23 Pathways for Digital Technologies to Change the Agrifood System

Kateryna Schroeder; Julian Lampietti; and Ghada Elabed

This chapter was adapted from What’s Cooking: Digital Transformation of the Agrifood System

“Schroeder, Kateryna; Lampietti, Julian; Elabed, Ghada. 2021. What’s Cooking : Digital Transformation of the Agrifood System. Agriculture and Food Series;. Washington, DC: World Bank. © World Bank. https://openknowledge.worldbank.org/handle/10986/35216 License: CC BY 3.0 IGO.”

Key Messages and Introduction

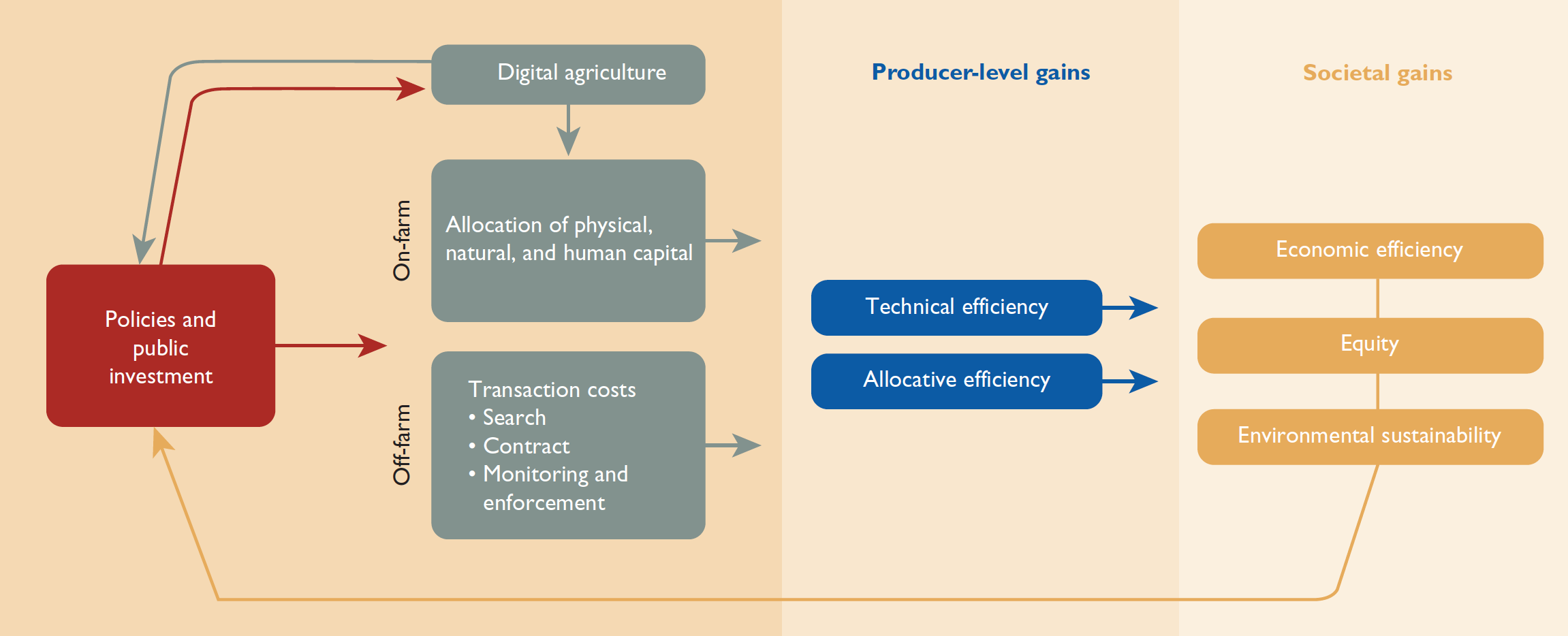

Figure 1 – Pathways for Digital Agriculture to Improve Efficiency, Equity, and Environmental Sustainability

Off the farm, digital technologies can sharply reduce the information-related transaction costs of farmer interactions with input and output markets, leading to improved allocative efficiency. Transaction costs—costs associated with the exchange of goods and services between buyer and seller—play a central role in the resource allocation decisions of agricultural producers and, consequently, in resource allocation at the societal level. Specifically, when the cost of a market transaction creates a disutility greater than the utility gain to producers, it results in a market failure (de Janvry, Fafchamps, and Sadoulet 1991). Effectively, trans-action costs raise the price to buyers and lower the price received by sellers, creating a price band within which some agents find it unprofitable to either sell or buy. In agriculture, the price band explains why many subsistence farmers lack access to profitable market opportunities and prefer to produce for home consumption (Cuevas 2014).

Transaction costs also explain the emergence of intermediary firms that strive to economize on such costs, resulting in frictions in the economy. A more complex modern agrifood system that requires the supply of products of consistent quantity, quality, and safety creates additional layers of transaction costs, which are often prohibitive for smallholder farmers. The digital agricul-ture revolution has sharply reduced transaction costs through the increased availability of information, greater transaction trust, and the ability to con-nect economic agents along the agrifood system. Digital computing power and advances in software have reduced information gaps between farmers and con-sumers and have decreased the need for traditional intermediaries to secure the transactions. While the biggest impact is on information-related transaction costs, other types of transaction costs, such as delivery costs, are also affected.

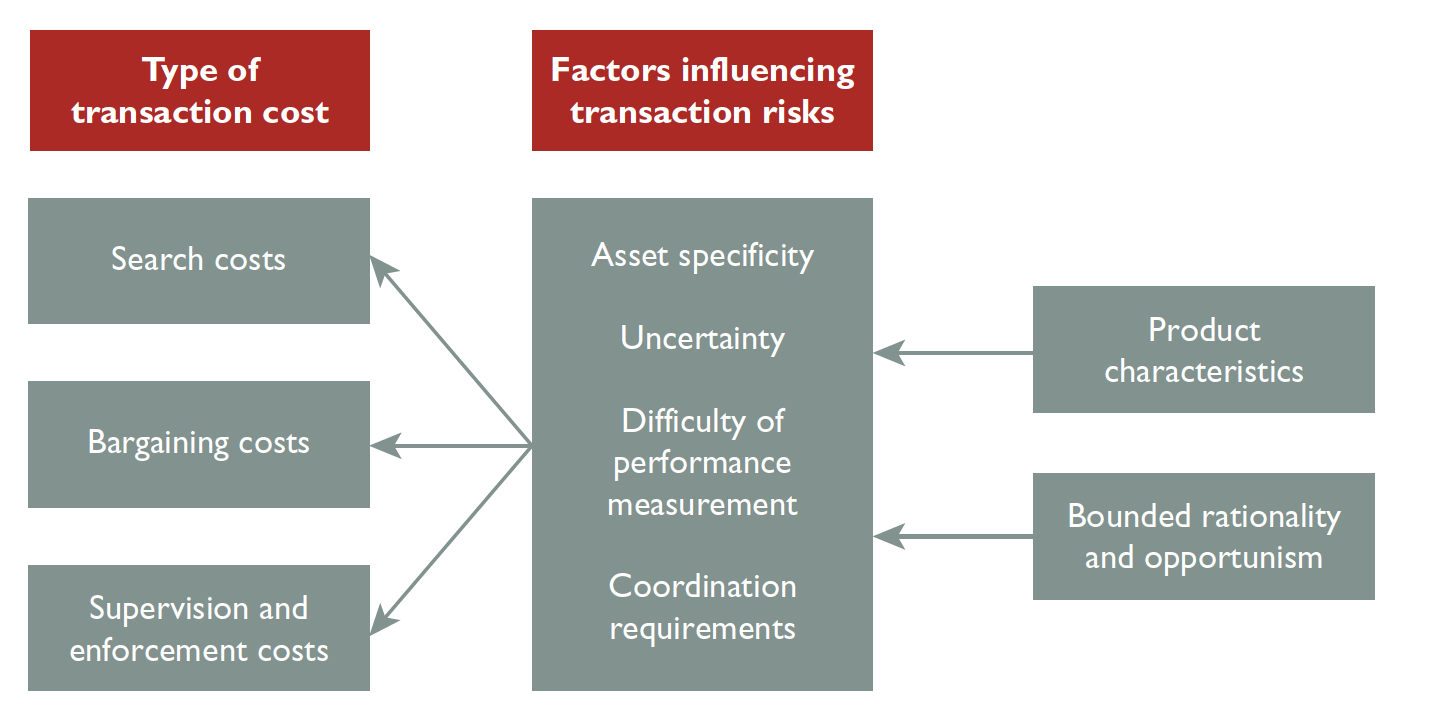

Broadly, three types of information-related transaction costs can be dis-tinguished: search costs, bargaining and decision costs, and supervision and enforcement costs (figure 3) (Eaton, Meijerink, and Bijman 2008). Search costs are the costs of looking for information on trading partners and on the prices and quality of products. Bargaining costs are the resources put into nego-tiating the terms of an agreement. Supervision and enforcement costs include the time and other costs of monitoring and enforcing the contract.

While the three types of transaction costs exist in all markets, four inherent features of agriculture result in higher transaction risks and, consequently, in higher transaction costs than in other markets (Eaton, Meijerink, and Bijman 2008). First, the uncertainty associated with production variability due to weather conditions, pests, and diseases is a particularly high risk in agricul-ture. It increases the transaction costs associated with concluding contracts

Figure 3 – Transaction Costs and Risks in Agricultural Value Chains

Source: Adapted with permission from Eaton, Meijerink, and Bijman 2008.

because of the potential need to renegotiate in the face of unforeseen events (Williamson 1979).

Second, asset specificity is the extent to which investments made by one or both parties to a transaction are specific to that transaction and thus have less value for transactions with other parties (Williamson 1988). For producers, investments in specific assets expose them to the risk of severe bargaining and contractual enforcement problems if a transaction falls through. In farm-ing, these risks are exacerbated by the prevalence of thin markets (meaning few alternative transactions are possible) and the perishability of agricultural commodities (meaning that a product’s value is inherently time dependent), both of which arise from farming’s context in remote, sparsely populated rural areas (Dorward and Kydd 2003). As a result, asset specificity in rural areas is often highly asymmetric: a powerful intermediary may be the only buyer of farmers’ produce, extracting most of the value in the transaction. In such cases, farmers have low incentives to invest in higher quality products, particularly for perishable goods.

Third, the need for coordination (connectedness of transactions) is par-ticularly high in agriculture. Transactions rarely take place in isolation but often depend on other transactions in the value chain or sector. For example, producers need to procure inputs (cash, seed, and fertilizer) before they can produce or market a product. All these transaction coordination efforts involve transaction costs.

Fourth, agricultural production makes performance measurement difficult, thereby raising the transaction costs associated with performance monitoring. For example, some characteristics of agricultural products may not be easily determined, such as how the product was produced (for example, the use of pesticides in organic produce).

Digital agriculture enables substantial reductions in transaction risks and costs through its influence on the factors that increase them. These reductions are possible because of the ability of digital technologies to generate and transmit massive amounts of data at nearly zero marginal cost and because digital platforms bring together many economic agents at the same time, again at nearly zero marginal cost. In other words, the proliferation of data and digital platforms thickens agrifood markets by increasing the number of potential buyers and sellers that can interact. At the same time, the increased flow of information on every process and customer along the agrifood value chain, underpinned by digital verification that makes it easier to certify the trustworthiness of an economic agent, strengthens trust in transactions.

By lowering transaction costs, digital agriculture affects economic activity in the sector in several ways (Deichmann, Goyal, and Mishra 2016; OECD 2019a; World Bank 2016). Falling transaction costs boost productivity and profitability in the sector. For example, falling transaction costs might lower input costs, increasing per-hectare profits. As transaction costs fall, farms and firms take up economic activities once precluded by high transaction costs. For example, the thickening of agrifood markets through greater trans-parency and lessened asset specificity creates opportunities for value cre-ation. Production processes can be more readily monitored and evaluated and information more easily transmitted to consumers, who may be will-ing to pay a price premium for their preferences. As a result, farmers can differentiate their products in a way that opens new markets, domestic and international. And as transaction costs fall close to zero, the structure of value chains can change and new business models emerge that can spark innova-tion, creating a virtuous cycle leading to further reductions in transaction costs. For example, as information-related transaction costs fall, traders may have a greater incentive to adopt efficient contracting structures than to verti-cally (or horizontally) integrate.

Pathways for Improved Equity

Three types of divides—economic, spatial, and social—exist in rural areas and may affect agrifood production. Economic divides stem from the unequal allocation of productive resources and differences in cost structures between smallholder farmers and those with larger farms. Spatial divides result from disadvantages in accessing markets, infrastructure, and public services in the sparsely populated areas in which farming takes place compared with access in urban or peri-urban communities. Social divides may prevent disadvantaged groups in rural areas, such as women and youth, from equitable access to resources or markets because of adverse societal and cultural norms or levels of educational attainment.

Digital agriculture has the potential to alleviate all three types of divides and boost equity. Economic divides can be narrowed through changes to econo-mies of scale; improved access to markets, including financial; and increases in productivity achieved through digital agriculture, all of which can enable smallholder farmers to participate in the value chains and lower poverty in rural areas. Spatial divides can be narrowed though digital technologies that lessen the disadvantages of remoteness by lowering hurdles to information, markets, and services. Finally, social divides can be narrowed through digital technologies that create opportunities to integrate disadvantaged groups into society; the spread of social media and changes in social interaction can also lessen social divides (IIASA 2019).

Digital agriculture can, however, create a new form of inequality: a digital divide. Digital divides can be defined as differences in the capacity to access and use information and communication technologies between individuals, men and women, households, geographic areas, socioeconomic groups, ethnic groups, and so forth. The capacity to access information and communication technolo-gies encompasses both physical access and access to the resources and skills to participate effectively as a “digital citizen.” The digital divide relates to a range of inequalities between social groups, genders, age groups, and rural and urban areas, both within and across countries (IIASA 2019). In the agrifood system, such inequalities concern (1) access to and use of digital technologies (including relevant skill sets and the quality and affordability of technologies and services); (2) the concentration of knowledge, power, and revenue in the hands of those who develop and own digital solutions and data; and (3) impacts on the economy through productivity gains and job losses. As a result, while digitalization promises to alleviate divides in the rural areas, it can exacerbate them if not well managed.

Inequality in Access to and Use of Digital Technologies

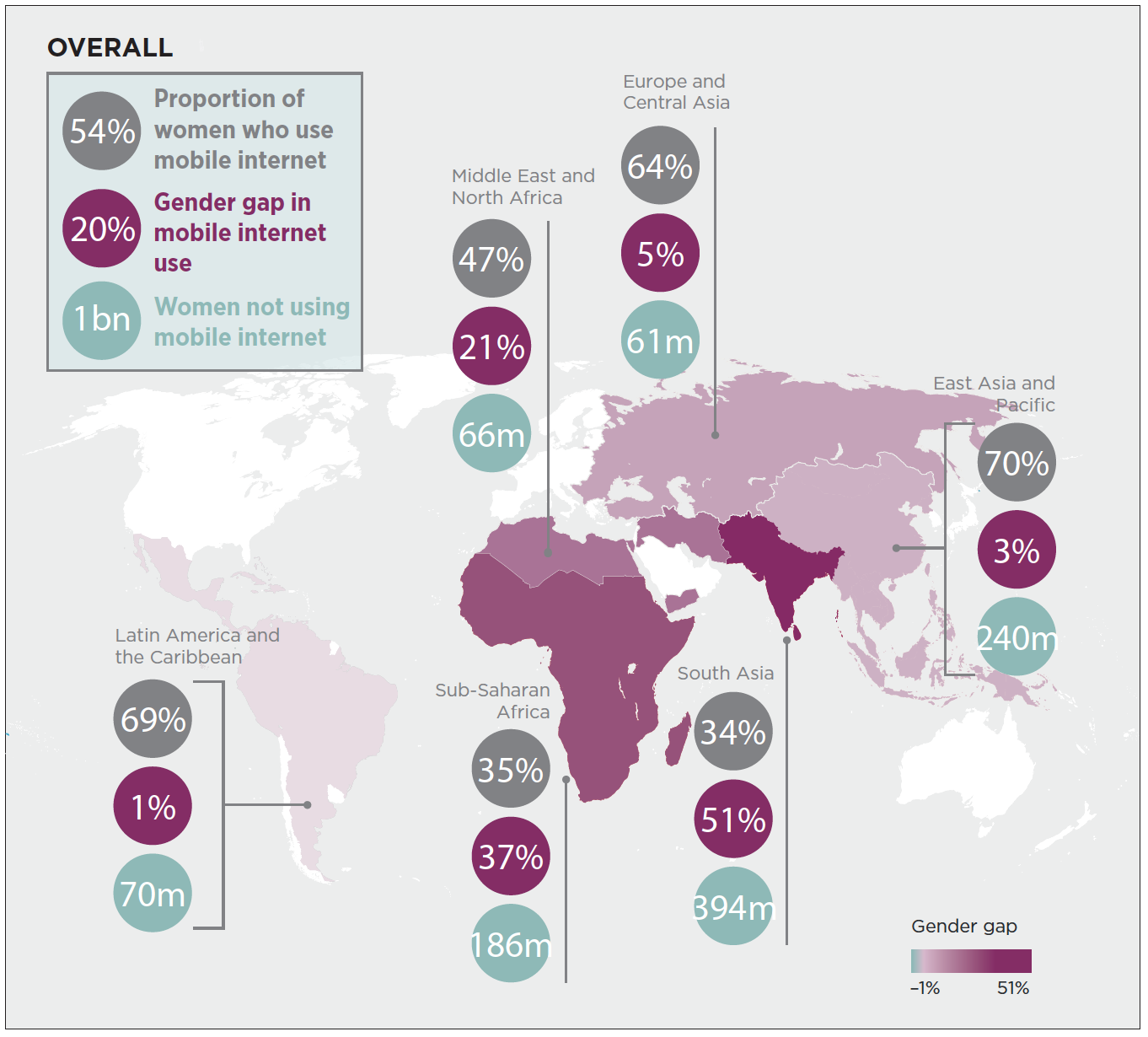

Digital divides often stem from the same economic, spatial, and social divides that already prevail in rural areas. For example, an analysis of the placement of cell phone towers in Sub-Saharan Africa found that small, isolated communi-ties are less likely to be near a cell phone tower (Buys, Thomas, and Wheeler 2009). Another study found that wealth-related variables, such as income and human capital, largely explain cross-country differences in internet access (Chinn and Fairlie 2007). Wealth also determines the types of devices and services that firms and households can afford. Women and girls face barriers to digital inclusion that reflect gender inequalities in society, in access to education, careers, and opportunities (Figure 4) (IIASA 2019). Skill and education levels also play a role. Larger-scale and better educated farmers are more likely to engage in digital agriculture than smallholder and less educated farmers (World Bank 2019).

The Concentration of Knowledge, Power, and Revenue in the Hands of Those Who Develop and Own Digital Solutions and Data

The cost of infrastructure (telecommunications, security protocols, ledgers, clouds, and so forth) and the advantage of accumulated data tend to favor big actors and first-movers in the development of new digital technologies, while creating barriers for later entrants (World Bank 2016, 2019). As a result, a few

Figure 4 – Gender Gaps in Mobile Internet Use Are Wide in Low- and Middle-Income Countries, 2019

Source: GSMA 2020

powerful companies dominate markets. For example, wealth and power in the digital space are increasingly concentrated in the hands of a small number of so-called global super platforms, including Microsoft, Apple, Amazon, Google, Facebook, Tencent, and Alibaba (UNCTAD 2019). There is also a high geo-graphic concentration in the platform economy, with the United States account-ing for 72 percent of the total market capitalization of platforms, followed by Asia, mainly China. Both high market valuations and the speed at which global digital companies have attained high capitalization attests to the value that comes from an ability to quickly collect data and transform it into digital intelligence (UNCTAD 2019). The value of data is also increasingly realized by corporate leaders in traditional sectors, such as agriculture (box 1), resulting in a changing market structure.

Impacts of Digital Agriculture on Input Industries

The development of digital agriculture influences the input-industry structure in three ways. The first and perhaps most important impact on the industry has been increased investments by new groups of investors and companies from out-side what is traditionally considered the agricultural input industry. The first group comprises the big information and communication companies, such as IBM, Google, and Alibaba. Another group comprises start-up companies from univer-sities in computer modeling and big data. Another group of start-ups is made of spinoffs from information technology companies such as ClimateCorp, which spun off from Google, or from machinery companies such as the Chinese drone com-pany XAG, which moved into agriculture in 2013. In the United States, much of the funding for these start-ups comes from venture capital groups that made money investing in computers and software and are now looking at food and agriculture as a new market for their investments. In addition to seeking financial returns, at least some of these investors see themselves as saving the planet through reducing the environmental impact of agriculture by reducing conventional inputs through precision farming.

The second important impact of digital agriculture has been vertical integration of major input firms in the provision of farm management services. There may also be a shift from input-based business models (providing herbicides) toward service-based business models (providing weed-free fields). Seed, biotech, and agricul-tural chemical companies and machinery companies are buying companies that provide short- and long-term weather predictions, crop and livestock management software, and other components to make digital platforms to provide farm man-agement recommendations to farmers. Part of their motivation is to make money by marketing farm management services through their current dealer networks, but they also want to protect or expand their market shares. Machinery compa-nies buy sensor producers and software companies. Animal health companies are also buying companies that provide sensors and tags for animals (Merck’s purchase of Antelliq).

A third change of industry structure involves the relationship between manu-facturers and dealers. One important factor is the possibility for machine manufac-turers to monitor farmers’ current use of their machines by directly accessing data collected by sensors mounted on tractors and machinery and transmitted back to the company. This information allows the manufacturers to do a better job pre-dicting current and future demand for the tractors and machinery and to use this data for refining their products. This information may also reduce the importance of their dealers in providing data for them, which may increase their bargaining power. However, not all farmers use digital solutions. So dealers still remain an important source of information for machine manufacturers. In Germany, it has been observed that machinery manufacturers increasingly request their dealers to use customer management software and share the data provided by this software with them. How the collection and sharing of this information will influence rela-tions among manufacturers, dealers, and farmers remains to be seen. It may foster the already ongoing trend toward more concentrated and more specialized dealer networks.

There is less evidence of the role digital agriculture has had on hori-zontal integration of input firms. Some evidence shows that European Union companies delivering precision agriculture technologies are expanding in size and shrinking in number (European Parliamentary Research Service 2017). However, the key question that remains unanswered and requires further research is the impact of the ongoing changes in the input industry on farmers’ access to inputs and the distribution of the value the input companies get from access to farm data.

Concentrations of knowledge and power can lead to information asym-metries in digital markets, increasing transaction costs for participants and affecting the functioning of the markets and ability to innovate. The market dominance of digital platforms is driven by three factors (UNCTAD 2019). The first is a network effect of a large platform—the more users a platform has, the more valuable it becomes to everyone. The second is the ability of digital platforms to aggregate, process, and control data—the more data plat-form collects the more it can cut its costs, satisfy the consumers, and improve its products relative to competitors. And the third is the dynamics of path dependency—once a platform begins to gain traction, the costs to users of switching to an alternative platform start to increase (Farrell and Klemperer 2007). As a result, large platforms control vast amounts of information about producers and consumers, which can create significant information asym-metries between the platforms and the stakeholders using the platforms. Information asymmetries stemming from the uneven accumulation of data among large and small companies can also reduce the ability of smaller com-panies to innovate (Nolet 2018). But Engels (2016) makes the case that digital platforms may support competition—product ranges (such as sales of sub-stitute services) provide for competitive conditions, and platform market conditions are regularly disrupted by innovation, so they are perhaps less susceptible to the accumulation of market power than more conventional exchange mechanisms. This has not been proved for the food value chain and justifies further research.

Impacts on the Economy Through Productivity Gains and Job Losses

The digital transformation of the agrifood sector creates winners and losers, and the role of the public sector is to ensure that the losers are properly compensated by the winners. The adoption of digital technologies tends to be skill- and knowledge-biased (OECD 2011). As a result, digital technologies tend to increase the demand for skilled labor while decreasing demand for unskilled labor, with implication for wage and income inequality (box 2).

Impacts of Digital Transformation on Agricultural Jobs

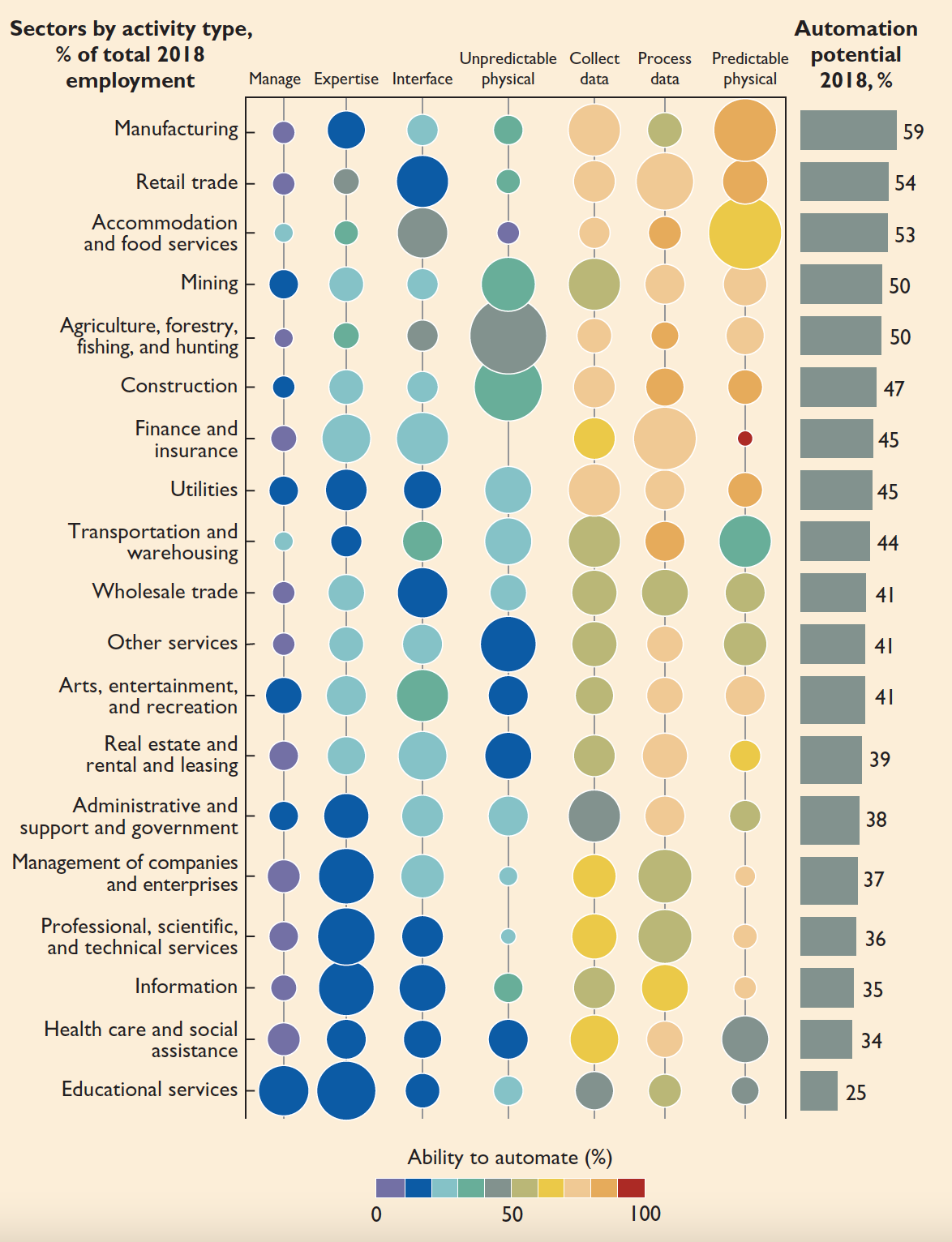

The digital agriculture revolution will likely have far-reaching consequences for the structure of agricultural labor around the world. The precise magnitude and direction of these consequences, however, is not yet clear. Emerging evidence from other industries shows that adopting digital technologies in agriculture may increase demand for higher-paying jobs requiring secondary education and decrease demand for jobs that perform routinized tasks (Autor 2015; Goecker et al. 2015; McKinsey Global Institute 2017). Specifically, the proliferation of digital technologies and automation of various processes displaces employment from jobs with routinized tasks, such as planting and harvesting, to jobs in which humans have a comparative advantage over machines, such as managing data analy-sis (Acemoglu and Restrepo 2020). A study from the McKinsey Global Institute projects that agriculture has a high potential for automation compared with other sectors (figure 6). Developed countries such as the United States and Canada, where digital agriculture has become more common than in other countries, pro-vide evidence for the hypothesis. In the United States and Canada, labor demand is increasing for higher-level activities such as farm management and the operation of digital technologies.As a result, digitalization of agriculture may reinforce social, economic, and spatial inequities in job opportunities and skills development, just as many digital technology divides already reflect existing social divides (Rotz et al. 2019). The effect of the digital transformation of agriculture on employment over time may be strong in countries with a large share of the labor force in agriculture and low productivity, mainly in Sub-Saharan Africa and South Asia. Yet these countries have lower capacity to adopt digital technologies, and any large change in agricul-tural employment is likely to be gradual (McKinsey Global Institute 2017).

While the displacement of workers is probable, digital agriculture also creates new pathways for employment. Digitalization is revolutionizing how farm-ers make decisions and how agricultural firms develop products and services. For example, apps such as Climate FieldView enable farmers to collect, store, and visualize critical data to maximize profits and yields (Climate Corporation 2020). The widespread availability of information thanks to digitalization also allows farmers to better understand consumer desires (Freddi 2008). This allows specialized farmers to satisfy evolving consumer tastes for niche products, such as organic foodstuffs and meat alternatives, and services, such as community-supported agriculture cooperatives. The burgeoning ag-tech scene has attracted considerable investor attention and represents a new frontier in farm employ-ment for innovative thinkers. Furthermore, new business models in agriculture are emerging postfarmgate that not only efficiently match supply and demand but also create new marketplaces for services and finance (Paris Innovation Review 2016). Online platforms represent such new employment avenues by reducing barriers to entry into markets and reducing search costs (Evans and Schmalensee 2007), yet the future effect on employment of online platforms across industries is difficult to model (Eichhorst et al. 2016) due to their negligible current role in the labor force (Katz and Krueger 2019). These platforms inevitably pressure the status quo (see Uber and the US taxi industry in Hall and Krueger 2016) and may decrease

Figure 6 – Automation Potential across Different Sectors of the Economy

Source: Adapted, with 2018 data, from McKinsey Global Institute 2017.

Note: Size of bubble indicates percentage of time spent in US occupations.

employment for just these reasons. To date, the evidence shows that introducing digital platforms does not have a monotonically negative correlation with employ-ment in industries where it has been adopted, as feared. But no significant positive correlation with employment has yet been empirically supported, either, so sweep-ing conclusions are inevitably misleading (Berger, Chen, and Frey 2018).The net effect of agricultural labor market transformation is yet to be seen. As change takes place, the key questions become to what extent do job losses occur, to whom, and whether or not the new jobs are shared across social and spatial levels, within economies, and between countries. To mitigate the negative effects brought about by the digital transformation, governments must address digital divides through investments in human capital and job-training programs. To prevent inequitable access to new jobs and educational opportunities, policy should target marginalized groups. Furthermore, policy makers will need to rethink social safety nets and income support for displaced workers, the “losers” in the transformation of the agrifood system (Acemoglu and Restrepo 2020; McKinsey Global Institute 2017). Sound digital agriculture policy can lead to productivity gains, economic growth, and reduced inequality across social and economic levels and places.

To incentivize the positive change toward digital technologies, governments should adopt clear, cross-cutting policies that reduce the cost of adopting new technologies, build trust in the digital transformation of agriculture, and create a positive enabling environment for the private sector to lead the charge in this revolution.

Pathways for Improved Environmental Sustainability

Digital agriculture can have direct, enabling, and behavioral effects on the environmental sustainability of the agrifood system. While it is impossible to fully quantify the impacts of digital agriculture on the environmental sus-tainability of the agrifood system, several pathways of change can be defined conceptually:

-

Direct effects stem from changes to production and distribution processes that have a direct impact on the use of natural resources or on greenhouse gas emissions. Such effects result from improvements in resource efficiency brought about by digital technologies and enabled through greater produc-tion control (such as precision agriculture), dematerialization of products and services on and off the farm, improved coordination of the agrifood system, and greater customization of production due to improved flows of information between producers and consumers.

- Enabling effects are attributable to the enhanced scope for environmen-tal monitoring of agricultural production systems. As digital technolo-gies enable the rapid and inexpensive dissemination of large amounts of environmental monitoring data (Kogan, Powell, and Fedorov 2010; Tsou, Guo, and Stow 2003), they allow for inventorying natural resources at national and global levels, monitoring their use, and ensuring compliance with environmental regulations. In turn, this enables addressing negative environmental externalities.

- Behavioral effects result from the transformation of the behavior and atti-tudes of food consumers and producers that affect the environmental sustainability of the agrifood system. As digital technologies expand the knowledge of the importance of sustainable production practices and allow for enhanced traceability, consumers can more easily act on their prefer-ences to consume food produced in an environmentally responsible way, in turn driving demand for more environmentally sustainable produc-tion. At the same time, digital technologies can disseminate information to the producers about the importance of sustainable production practices along with advice on how to implement them. Digital technologies can also strengthen the role of certifications and agreements that aim for environ-mentally friendly production practices and waste management (Berkhout and Hertin 2004).

The environmental impacts of digital agriculture are expected to be mostly positive, but there are also risks. Digital technologies are essential to measur-ing, modeling, and communicating the environmental impacts of the agrifood system. The impacts on environmental sustainability are expected to be largely positive. Digital technologies improve resource efficiency through greater pro-cess control, while addressing environmental problems at the global level and driving behavioral change among consumers and producers. Still, there are several known risks of digital technologies. For example, digital technologies consume energy (Berkhout and Hertin 2004), generate e-waste, or lead to a so-called rebound effect when efficiency gains, directly or indirectly, stimulate new demand that can offset environmental gains (OECD 2001). Precision agri-culture can lead to biodiversity loss (European Parliamentary Research Service 2017). Developing efficient and effective policy responses to improve the envi-ronmental sustainability of the agrifood system requires understanding both the pathways through which digital agriculture affects the environment and the potential risks associated with new technologies.

Public Policy Entry Points for Accelerating Digital Transformation of the Agrifood System

While the creation and use of digital agricultural technologies are fundamen-tally private sector activities, driven by the private gains of profit-maximizing producers and utility-maximizing consumers, the public sector may need to remedy market failures that distort incentives. Private economic agents may not have the right incentives to make rational decisions because of market or policy failures, lack of public good provision, or inadequate information about their options and the impacts of their decisions. Some of the characteristics of digital goods, such as nonrivalry, nonexcludability, infinite durability, and experience-good nature, may make it challenging for the private sector to sup-ply and use digital technologies in the agrifood system (box 3). In such cases, the entry point for public policy is to influence the incentives and decisions of private agents with the goal of maximizing efficiency gains at the societal level and maximizing the equity and environmental sustainability impacts of the adoption of digital agriculture that may not be fully internalized by pri-vate economic agents. In creating incentives to prompt behavior among private economic agents that maximizes societal benefits, the public sector must take care also to mitigate the potential (sometimes unknown) risks arising from digital agriculture.

The Maximizing Finance for Development (MFD) framework can help identify public actions needed to facilitate broader development and adop-tion of digital technologies and harness their impact on food system outcomes (World Bank 2019). MFD looks for ways to crowd in private resources to help

Properties of Digital Informatiion and Digital Goods Have Implicatiioins for Their Supply in Rural Areas

Digital goods are infinitely durable, with economic implications for their cre-ators. They are infinitely durable because they work on multiple devices—whether embodied or disembodied—and can be easily transferred from one medium to another (Rayna 2008). While the durability of a device is limited, digital goods can be stored indefinitely if they are transferred to a new device or medium. For exam-ple, a video on proper maize planting techniques can be transferred from the device of one farmer to the devices of many others across time and space. For compa-nies trying to get some return on their digital goods, this poses a challenge. Unless producing firms artificially reduce the durability of digital goods (for example, by renting, which limits the product’s durability to the duration of the rental period), the expected effect of the infinite durability of digital goods in a competitive setting is a progressive decline in demand and falling prices, limiting profit opportunities.Digital information and many digital goods typically are nonrivalrous and sometimes nonexcludable and so can be considered public goods. Because digital datasets and digital goods are, at the margin, nearly free to replicate, they are non-rivalrous from an economic perspective: one person can use a digital dataset or digital good without affecting the quality or quantity available for others to use. While digital information is nonrivalrous, it can also be a component of a physical good—for example, a copyright-protected algorithm programmed into a sensor, which itself is a component of a sowing machine. In this case, the final good is not fully a knowledge good and not strictly digital. So the sowing machine and its knowledge-product components can be marketed as a standard private good. But once nonrivalrous information takes the form of a nonrivalrous, reproducible, and easily transferred digital good, the nature of the good changes dramatically. Digital goods can also be largely nonexcludable, provided no policy or technical restriction is in place. In such a case, it is hard for anyone to exclude others from consuming them. This implies that reproduction costs are nearly zero. For producers of digital goods, the inability to exclude nonbuyers from using the goods means a loss of potential revenue for their products, undermining their incentive to create. That is why digital goods produced for embodied devices often have technical restrictions created by the manufacturer to prevent nonexcludability. From a public sector per-spective, nonexcludability creates a strong incentive to place digital data and some digital goods in the public domain.

In addition to being nonrivalrous, nonexcludable, and durable goods, digital goods are experience goods. A good is considered an experience good when full information about its main attributes is unknown without direct experience of the good or when the search for information about the main attributes is more costly or difficult than experiencing the product directly (Klein 1998). The qualities of experience goods, such as compact discs, have implications for consumers and producers. Because it is difficult to make a judgment about a digital good before experiencing it, consumers tend to reward the reputation of established suppliers of digital goods, making it harder for smaller players to enter the markets. Digital good producers need to employ consumer segmentation strategies (such as selling limited versions with fewer features) or offer samples to interested consumers to limit the amount of information consumers must process to decide whether to purchase the good. The experience-good nature of digital agriculture goods has implications for the adoption of digital technologies. In agriculture, a digital good is often judged by the economic outcomes on the farm; for example, if a farmer buys a subscription to an e-advisory service and if following the advice does not result in higher yields or prices at harvest, the farmer will be unlikely to renew the subscription.

The characteristics of digital goods have implications for their supply in rural areas. Because digital goods and services are nonrivalrous, replicable, and easily transferred, the marginal cost of delivering them to network-connected devices is nearly zero, even though the fixed cost of developing the product can be high, par-ticularly for digital goods produced for embodied devices. So, even small gains to a provider of digital goods or services from each nonrivalrous exchange can pro-vide a pathway for the product developer to recover fixed investments and realize profits. Providers of digital goods may employ various pricing approaches, such as bundling and subscription services, consumer segmentation strategies, and barter-ing for data. Providers can also put technical restrictions or licenses in place that limit the replicability of digital goods and information. Regardless of the strate-gies employed, the ability of a provider to recover the fixed costs depends on the expected technology adoption by farmers and, hence, the “thicknesses” of the mar-ket. So developers of highly sophisticated embodied digital devices and related digital goods must often focus on developing solutions for markets dominated by medium- and large-scale farmers, who are likely to adopt more expensive technolo-gies (see chapter 3). Even so, embodied digital solutions suitable for smaller farms, such as sensors or tracking devices, have also been emerging, although just as for more sophisticated tools, incentives for developers to invest in production of such solutions depends on their expected profits. Because farming often takes place in sparsely populated rural areas, markets for digital goods often may be “thin” unless they are adopted across vast geographic areas. So digital solutions for agriculture may not be immediately attractive to digital technology developers, justifying a public sector response, as discussed in the last section of this chapter.

achieve development goals, while optimizing the use of scarce public resources. Since digital technologies are primarily generated by the private sector, and since the farmers and agribusinesses adopting these technologies are also pri-vate actors, MFD can help identify entry points for public sector actions to facilitate the broader adoption of digital technologies and harness their impact on food system outcomes (see appendix E) (World Bank 2019).

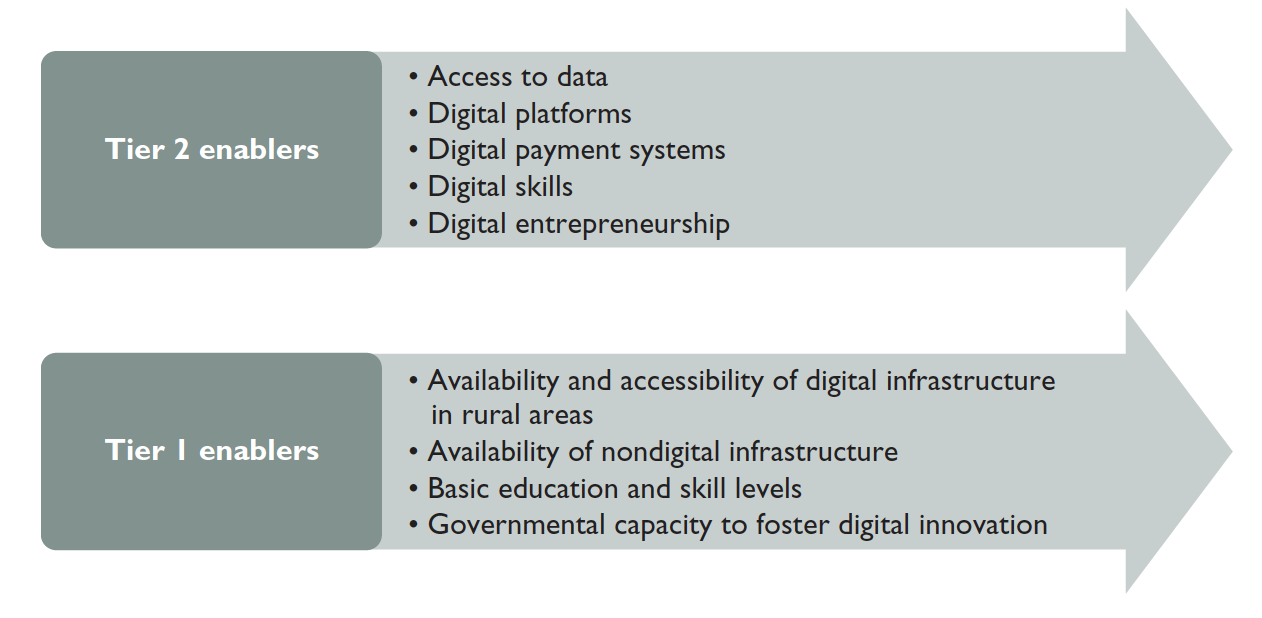

A starting point for the government is to create an enabling environment for the development of the tier 1 enablers for successful digital transformation, led by the private sector (figure 7). First, to maximize the efficiency, equity, and environmental sustainability gains from digital agriculture, good quality, acces-sible networks in rural areas are essential. The type of network infrastructure influences the type of digital applications that can be used. For example, second generation networks are more suited for voice and text messaging, while third, fourth, and fifth generation networks enable use of a much broader set of digi-tal devices and applications. The second foundation requires complementary investments in rural electricity, roads, and logistics to power digital devices and bridge digital markets. Finally, if the government is to facilitate digital trans-formation of the agrifood system, it has to develop governmental capacity to foster digital innovation and ensure the equitable distribution of the benefits by building data infrastructure and developing human capital. The government needs to be equipped with the physical, digital, and institutional structures that enable and govern the collection, transfer, storage, and analysis of data to pro-duce knowledge and advice for the agrifood system. And it needs to strengthen its own human capital through training or retraining for applying digital tech-nologies and analyzing underlying data, so that it establishes the right goals and instruments to support digital transformation.

To maximize the economic efficiency gains of digital agriculture, as a next step, public and private sectors need to jointly form an innovation ecosys-tem for digital agriculture to spur the supply of digital agriculture solutions. Building on the tier 1 enablers, the innovation ecosystem needs to include some

Figure 7 – Enablers of Digital Innovation Ecosystems in the Agrifood System

Source: World Bank

additional elements (tier 2 enablers), such as the availability of open datasets, digital platforms, the digital entrepreneurship environment, digital payment systems, and digital skills to incentivize the development of digital innova-tion ecosystems. On the government side, supportive public policy interven-tions should generally provide public goods and create an enabling policy and regulatory environment for the private sector to thrive. Theory and practical experience across many countries indicate that basing spending decisions on this general principle will ensure that public expenditures yield greater bang for the buck and crowd in—rather than crowd out—private sector investments. There may be cases where subsidies for private goods are justified to correct market failures, but these should be exceptions.

To facilitate the adoption of digital agriculture, governments have many tools to increase the uptake of digital solutions in the agrifood system by private economic agents. In addition to skills development, governments can promote the development of relevant, customized digital tools in a suitable format and languages; reduce the cost of adopting digital technologies and facilitate access to finance to enable adoption; and build trust in digital applications, particu-larly given the fact that digital goods are experience goods. Government inter-ventions should target the whole value chain, not just specific constraints in isolated segments of the value chain. The impact of government interventions will depend on how they affect the prices faced by all actors. Digital tech-nologies that reduce some frictions while leaving others could distort market outcomes, helping some actors and hurting others. For example, if farmers increase production through e-extension services but cannot access markets, they are unlikely to value digital solutions. Digital goods tend to be experience goods, so negative experiences may sharply reduce demand.

To ensure the equitable distribution of digital dividends, governments need to target digital divides as well as economic, spatial, and social divides. While public policy measures targeting economic, spatial, and social divides are not directly within the scope of this report, it is relevant to note that digital tech-nologies offer solutions for tackling these divides. Governments can improve access to and use of digital technologies by marginalized groups; monitor and address concentrations of knowledge, power, and revenue in the digital world; and adopt compensatory measures for potential losers from the digital trans-formation of the agrifood system.

Governments can increase the environmental sustainability of the agrifood system through digital technologies. The proliferation of digital technologies in agriculture offers enormous potential to enhance the environmental sustain-ability of the agrifood system. This can be achieved through more efficient use of production resources at the farm level, changes to distribution processes, improved capacity for environmental monitoring, and changes in the behavior of food consumers and producers and in their attitudes toward the environ-mental impacts of the agrifood system. The role of the public sector is to nudge producers and consumers in the direction of more environmentally sustainable choices. Possible actions include strengthening digital environmental monitor-ing, incentivizing the use of digital technologies for environmental sustainabil-ity, and applying e-education and information dissemination to influence the behavior of producers and consumers.

To identify the most appropriate and effective policies and entry points to spur digital innovation in the agrifood system, governments need clear pol-icy objectives. The goals of increasing efficiency, equity, and environmental sustainability in the agrifood system are largely interdependent. For example, more efficient use of inputs on the farm tends to result in positive environ-mental outcomes, improved profitability, and greater inclusion even for small producers. Even so, in formulating policies for digital development of the agri-cultural sector, governments need to prioritize interventions in areas where the gaps are largest, while also anticipating and addressing risks and second-order effects of the interventions along pathways in the efficiency, equity, and environmental sustainability framework. The approach needs to be as holistic as possible. For example, the ability of digital technologies to reduce transac-tion costs in the agrifood system has the potential to increase market efficiency and competition. At the same time, if digital technologies reduce some frictions but not others, that can distort market outcomes, widening the digital divide. Finally, digital development in the agrifood system should not be considered a goal but rather a means to achieve the societal gains of efficiency, equity, and environmental sustainability. The focus of policy agenda for accelerating digi-tal agriculture transformation in a country would depend on the level of agri-cultural and digital development in a country. The report’s digital agriculture profiling tool introduces an assessment framework to evaluate the state of a country’s agricultural and digital development and identify public policy entry points to maximize the efficiency, equity, and environmental sustainability of digital transformations in agriculture (appendix A).

References

/WorkingPaper246.pdf.