8.6 Calculating the Cost of a Job

Determining the Costs of an Individual Job Using Job Order Costing

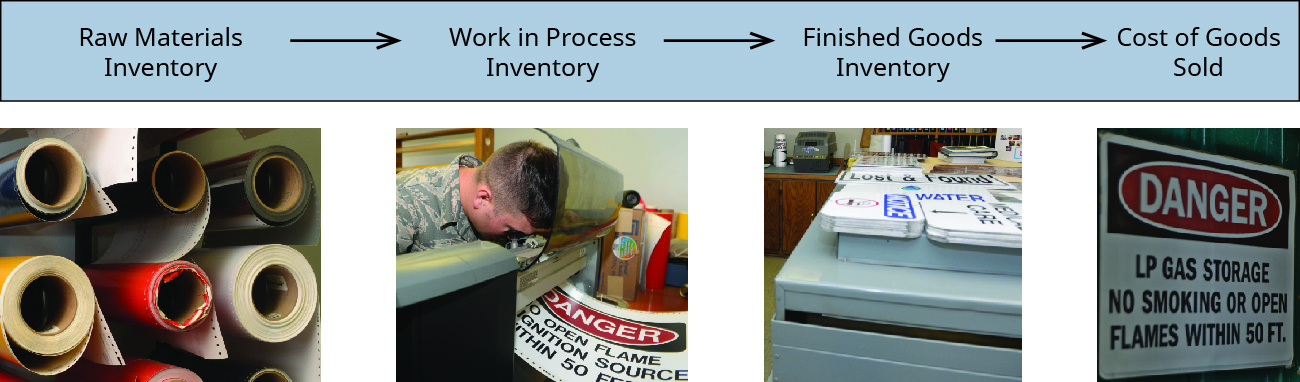

When a job is completed, the costs of the job—the direct materials, direct labor, and manufacturing overhead—are totaled on the job cost sheet, and the total amount is transferred to finished goods at the same time the product is transferred, either physically or legally, such as in the case of a home built by a contractor. Finally, when the product is sold, the sale is recorded at the sale price, while the cost is transferred from finished goods inventory to the cost of goods sold expense account. Figure 8.42 shows the flow of costs from raw materials inventory to cost of goods sold.

At all points in the process, the work in process should include the cost of direct materials and direct labor. When the job is completed and overhead assigned, the overhead allocation increases the cost of the work in process inventory. The cost of each individual job is maintained on a job cost sheet, and the total of all the work in process job cost sheets equals the work in process inventory and the statement of cost of goods manufactured, as you have learned.

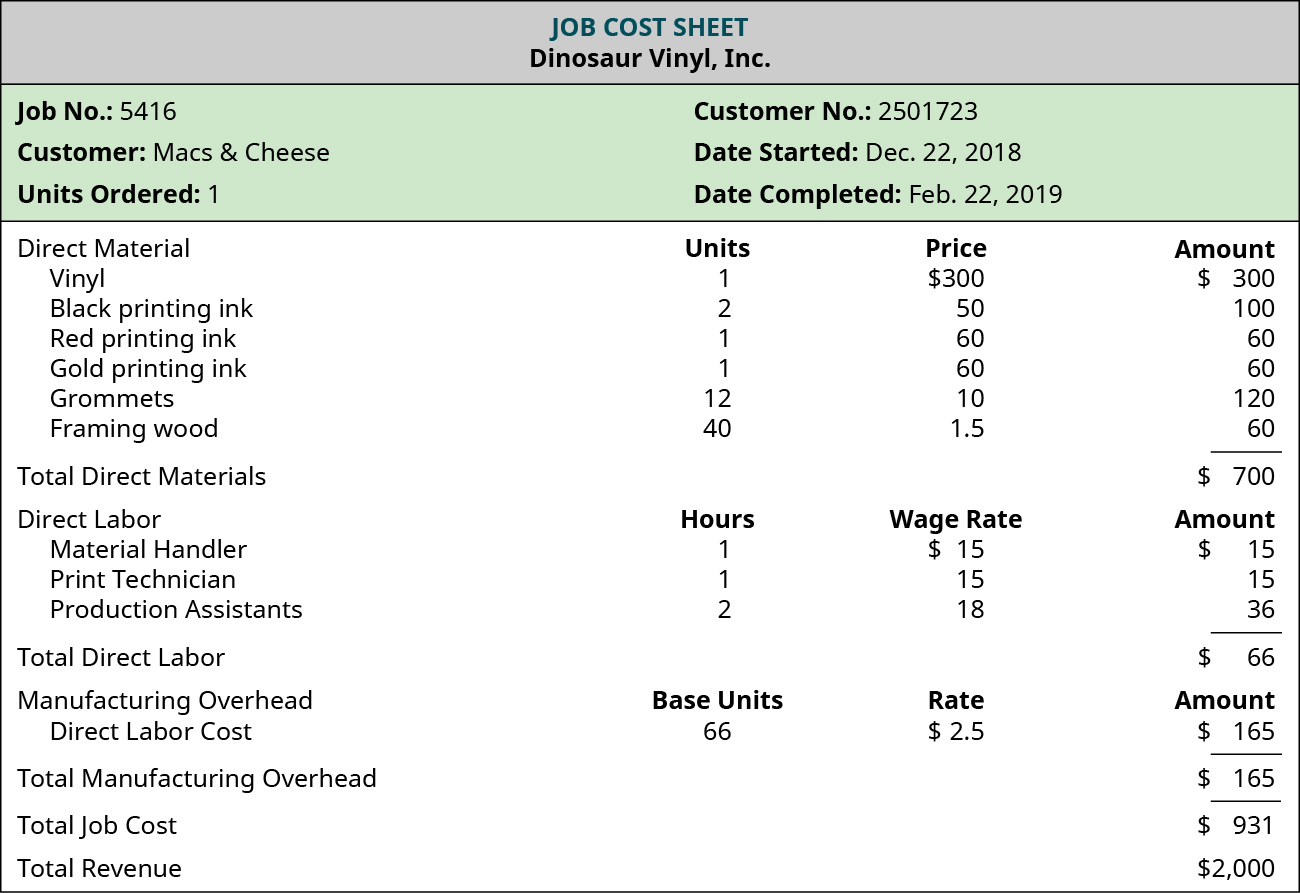

A job cost sheet is a subsidiary ledger that identifies the individual costs for each job. Figure 8.43 shows the job cost sheet for Job MAC001.

Sample Cost Information for Dinosaur Vinyl

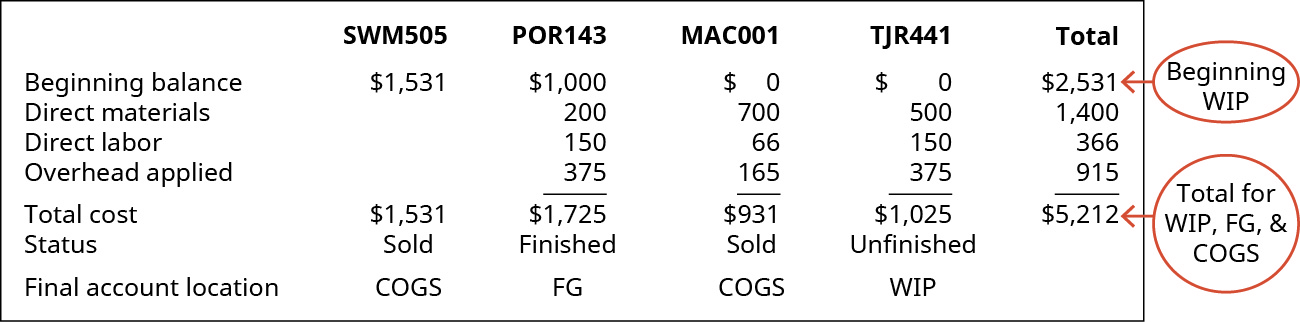

Dinosaur Vinyl worked on three jobs during the month: POR143, MAC001, and TRJ441, and a fourth Job SWM505 had been finished and moved to the finished goods inventory account during the previous month.

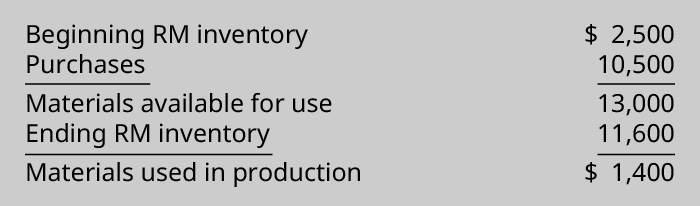

At the beginning of the month, the company had a beginning raw materials inventory balance of $2,500, and during the month, it purchased an additional $10,500, giving it a total of $13,000 in raw materials available for use in production.

The following example will examine four different production jobs. Each of the four will be at beginning stages at either the beginning of the current month or the end of the current month.

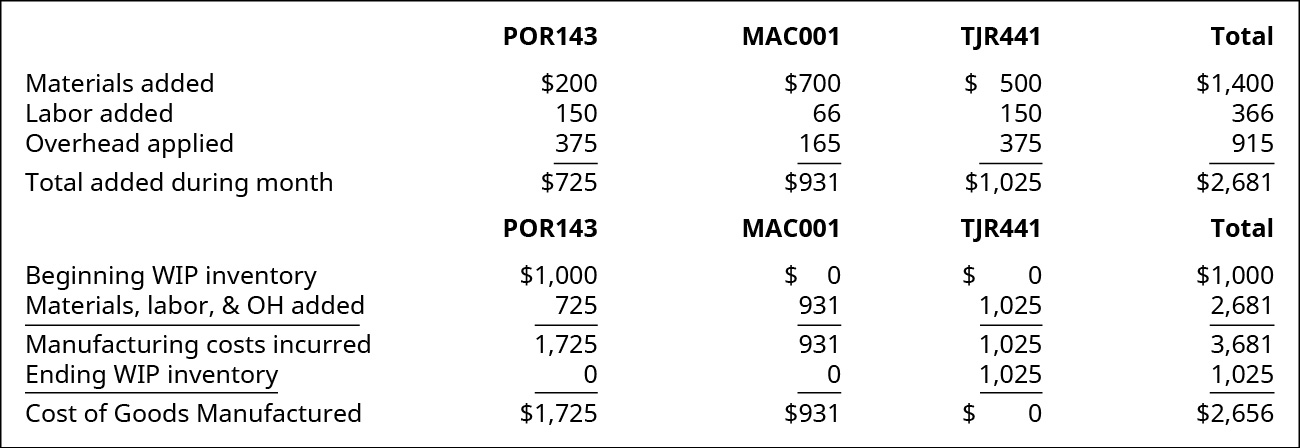

- Job POR 143: This job was the only work in process inventory at the beginning of the current month, and it had $1,000 in direct material costs, and $0 of direct labor costs already allocated to the work in process inventory. During the current month, additional direct materials of $200 and direct labor of $150 were added to POR143. An overhead cost of $375 was applied to POR143 at the predetermined overhead rate of $2.50 per direct labor dollar. It was finished during the month and transferred to the finished goods inventory. The sale was not finalized during the month, so it continues to be part of the finished goods inventory.

- Job MAC 001: This job was started and completed during the month. Since the job began in and was completed in the same month, there was no beginning balance in the work in process inventory. During the month it incurred $700 in direct materials costs, $66 in direct labor, and $165 of overhead applied to the job before it was transferred to the finished goods inventory upon completion. The sale was finalized during the month at a sale price of $2,000, so the costs were transferred from finished goods inventory to cost of goods sold.

- Job TRJ441: This job was started during the current month. Its costs consist of $500 in direct material cost, $150 in direct labor expenses, and $375 in applied overhead. The job remains in the work in process inventory awaiting assembly.

- Job SWM505: At the beginning of the month, this job was completed and already in the finished goods inventory at a cost of $1,531. Since it was completed, it did not incur any additional costs in the current month. It was sold during the month for $3,500, and the costs were transferred from the finished goods inventory to cost of goods sold.

The cost of raw materials used is calculated as shown:

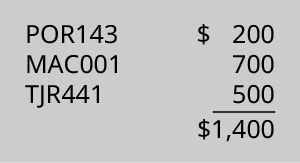

The individual job cost sheets show the $1,400 worth of materials used in production:

The cost of goods manufactured is accounted for as shown:

Notice the costs for Job TJR441 are included in the work in process inventory, whereas the costs for POR143 and MAC001 were transferred to the cost of goods manufactured. The costs of the jobs transferred are shown in the cost of goods sold and the finished goods inventory:

Mechanics of Job Order Costing for Dinosaur Vinyl

The amounts in raw materials, work in process, and finished goods inventories compose the total cost for each account, whereas the job cost sheets contain the costs for each individual job. A summary of the jobs for Dinosaur Vinyl is given in Figure 8.48.

Long Descriptions

A chart showing the calculation of Cost of Goods Manufactured for jobs POR143, MAC001, TJR441 and the Total. Respectively: Materials added are $200, $700, $500, and $1400; Labor added is 150, 66, 150, and 366; Overhead applied is 375, 165, 375, and 915; for Total added during the month of $725, $931, $1,025, and $2,681. Calculation is Beginning WIP Inventory of $1,000, $0, $0, and $1,000; Material, Labor, and Overhead added is 725, 931, 1,025, and 2,681; Equaling Manufacturing costs incurred of 1,725, 931, 1,025, and 3,681. Subtract Ending WIP Inventory of 0, 0, 1,025, and 1,025; Equaling Cost of Goods Manufactured of $1,725, $931, $0, and $2,656. Return

Chart showing Cost of Goods Sold for SWM505 POR143, MAC001, TJR441, and the Total. Respectively the dollar figures are: Beginning Finished Goods Inventory 1,531, 0, 0, 0, 1,531; plus Cost of Goods Manufactured 0, 1,725, 931, 0, 2,656; equaling Goods Available for Sale 1,531, 1,725, 931, 0, 4,187. Then subtract Ending Finished Goods Inventory of 0, 1,725, 0, 0, and 1,725 to get Cost of Goods Sold of 1,531, 0, 931, 0, and 2,462. Return

Chart showing a summary of the Jobs: SWM505, POR143, MAC001, TJR441, and Total. Beginning Balance $1,531, 1,000, 0, 0, 2,531 (which is the Beginning WIP for the company) plus Direct Materials 0, 200, 700, 500, and 1,400 plus Direct Labor 0, 150, 66, 150, 366 plus Overhead applied 0, 375, 165, 375, and 915 equals total cost of 1,531, 1,725, 931, 1,025, and 5,212 (which is Total for WIP, FG, and CGS) Status is Sold, Finished, Sold, and Unfinished, Final account location is Cost of Goods Sold, Finished Goods Inventory, cost of Goods Sold, and WIP Inventory. Return