7.5 Multi-product Breakeven Analysis

Up to this point in our CVP analysis, we have assumed that a company only sells one product, but we know that, realistically, this is not the case. Most companies operate in a multi-product environment, in which they sell different products, manufacture different products, or offer different types of services. Companies price each one of their products or services differently, and the costs associated with each of those products or services vary as well. In addition, companies have limited resources, such as time and labor, and must decide which products to sell or produce and in what quantities, or which services to offer in order to be the most profitable. These profitability considerations are often what contributes substance to a sales mix decision

In order to perform a break-even analysis for a company that sells multiple products or provides multiple services, it is important to understand the concept of a sales mix. A sales mix represents the relative proportions of the products that a company sells—in other words, the percentage of the company’s total revenue that comes from product A, product B, product C, and so forth. Sales mix is important to business owners and managers because they seek to have a mix that maximizes profit, since not all products have the same profit margin. Companies can maximize their profits if they are able to achieve a sales mix that is heavy with high-margin products, goods, or services. If a company focuses on a sales mix heavy with low-margin items, overall company profitability will often suffer.

Performing a break-even analysis for these multi-product businesses is more complex because each product has a different selling price, a different variable cost, and, ultimately, a different contribution margin. We must also proceed under the assumption that the sales mix remains constant; if it does change, the CVP analysis must be revised to reflect the change in sales mix. For the sake of clarity, we will also assume that all costs are companywide costs, and each product contributes toward covering these companywide costs.

Calculating Break-Even Analysis in a Multi-Product Environment

When a company sells more than one product or provides more than one service, break-even analysis is more complex because not all of the products sell for the same price or have the same costs associated with them: Each product has its own margin. Consequently, the break-even point in a multi-product environment depends on the mix of products sold. Further, when the mix of products changes, so does the break-even point. If demand shifts and customers purchase more low-margin products, then the break-even point rises. Conversely, if customers purchase more high-margin products, the break-even point falls. In fact, even if total sales dollars remain unchanged, the break-even point can change based on the sales mix. Let’s look at an example of how break-even analysis works in a multi-product environment.

In multi-product CVP analysis, the company’s sales mix is viewed as a composite unit, a selection of discrete products associated together in proportion to the sales mix. The composite unit is not sold to customers but is a concept used to calculate a combined contribution margin, which is then used to estimate the break-even point. Think of a composite unit as a virtual basket of fruit that contains the proportion of individual fruits equal to the company’s sales mix. If we purchased these items individually to make the fruit basket, each one would have a separate price and a different contribution margin. This is how a composite unit works in CVP analysis. We calculate the contribution margins of all of the component parts of the composite unit and then use the total to calculate the break-even point. It is important to note that fixed costs are allocated among the various components (products) that make up this composite unit. Should a product be eliminated from the composite unit or sales mix, the fixed costs must be re-allocated among the remaining products.

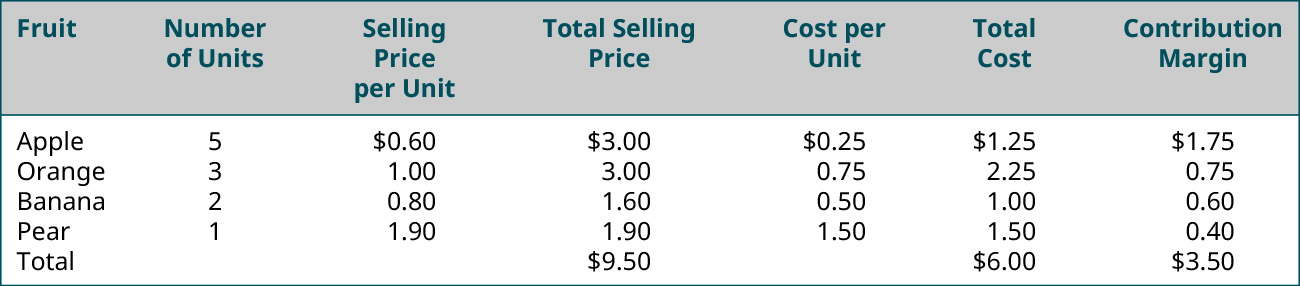

If we use the fruit basket as an example, we can look at the individual fruits that make up the basket: apples, oranges, bananas, and pears. We see that each individual fruit has a selling price and a cost. Each fruit has its own contribution margin. But how would we determine the contribution margin for a composite of fruit, or in other words, for our basket of fruit?

For our particular baskets, we will use 5 apples, 3 oranges, 2 bananas, and 1 pear. This means that our product mix is 5:3:2:1, as shown in Figure 7.49.

Notice that the composite contribution margin is based on the number of units of each item that is included in the composite item. If we change the composition of the basket, then the composite contribution margin would change even though contribution margin of the individual items would not change. For example, if we only include 4 apples, the contribution margin of a single apple is still $0.35, but the contribution margin of the apples in the basket is $1.40, not $1.75 as it is when 5 apples are included in the basket. Let’s look at an additional example and see how we find the break-even point for a composite good.

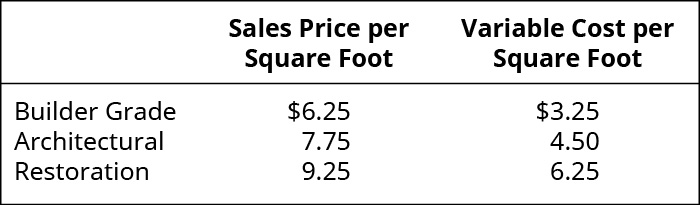

We will consider West Brothers for an example of a multi-product break-even analysis. West Brothers manufactures and sells 3 types of house siding: restoration vinyl, architectural vinyl, and builder grade vinyl, each with its own sales price, variable cost, and contribution margin, as shown:

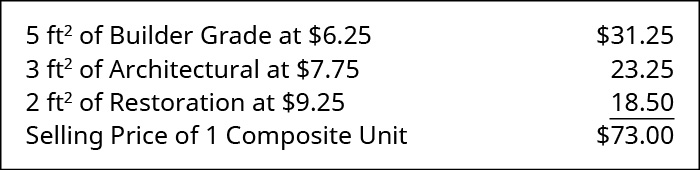

The sales mix for West Brothers is 5 ft2 of builder grade to 3 ft2 of architectural grade to 2 ft2 of restoration grade vinyl (a ratio of 5:3:2). This sales mix represents one composite unit, and the selling price of one composite unit is:

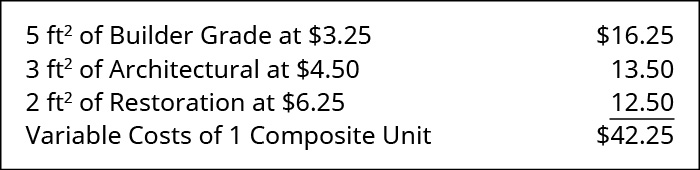

West Brothers’ fixed costs are $145,000 per year, and the variable costs for one composite unit are:

We will calculate the contribution margin of a composite unit for West Brothers using the same formula as before:

Applying the formula, we determine that $73 – $42.25 = 30.75. We then use the contribution margin per composite unit to determine West Brothers’ break-even point:

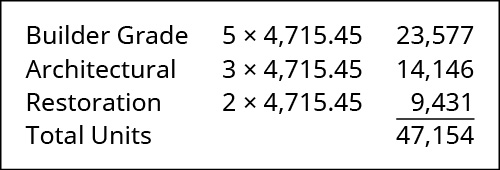

West Brothers will break even when it sells 4,715.45 (or 4,716 since it can’t sell a partial unit) composite units. To determine how many of each product West Brothers needs to sell, we apply their sales mix ratio (5:3:2) to the break-even quantity as follows:

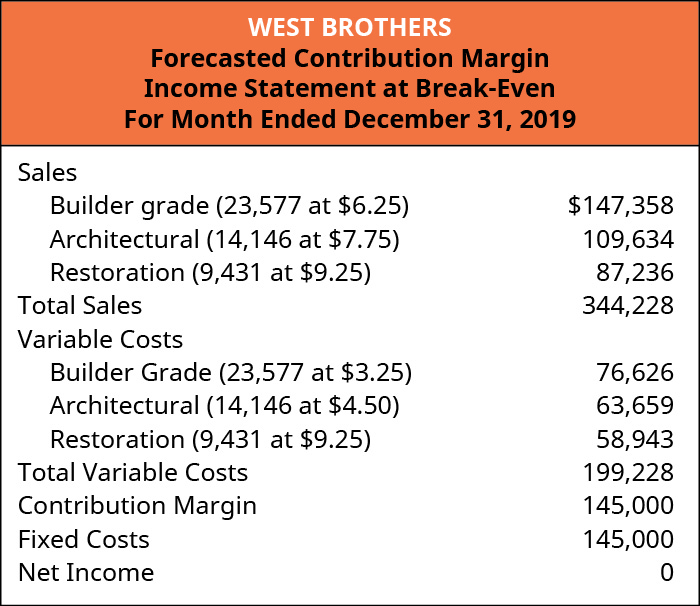

Using a forecasted or estimated contribution margin income statement, we can verify that the quantities listed will place West Brothers at break-even.

West Brothers can use this CVP analysis for a wide range of business decisions and for planning purposes. Remember, however, that if the sales mix changes from its current ratio, then the break-even point will change. For planning purposes, West Brothers can change the sales mix, sales price, or variable cost of one or more of the products in the composite unit and perform a “what-if” analysis.

YOUR TURN

Margins in the Sales Mix

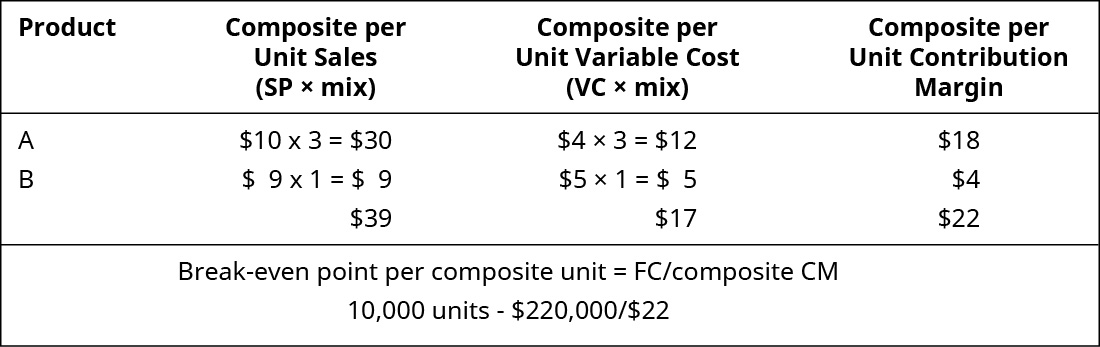

The sales mix of a company selling two products, A and B, is 3:1. The per-unit variable costs is $4 for Product A and $5 for Product B. Product A sells for $10 and product B sells for $9. Fixed costs for the company are $220,000.

- What is the contribution margin per composite unit?

- What is the break-even point in composite units?

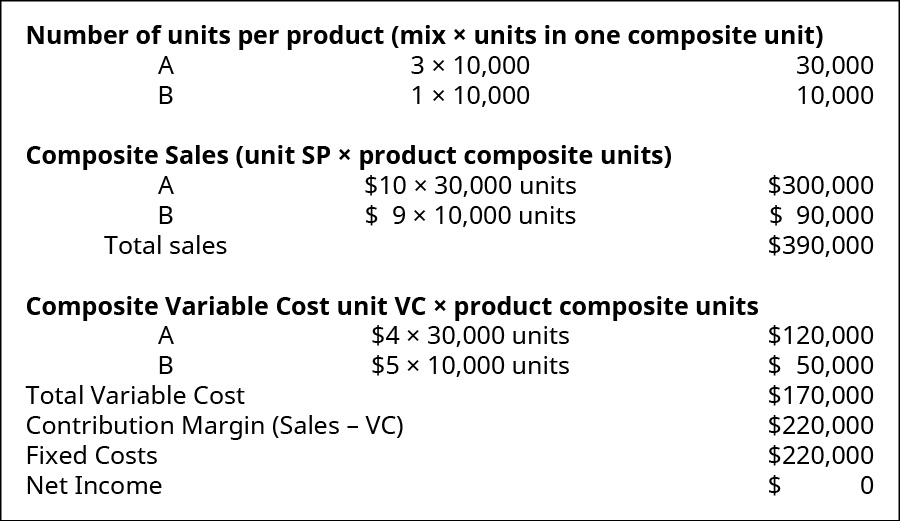

- How many units of product A and product B will the company sell at the break-even point?

Solution

A.

B.

Break-even per composite unit = 15,385.

C.

Long Description

Fruit, Number of Units, Selling Price per Unit, Total Selling Price, Cost per Unit, Total Cost, Contribution Margin (respectively): Apple 5, $0.60, 3.00, 0.25, 1.25, 1.75; Orange 3, $1.00, 3.00, 0.75, 2.25, 0.75; Banana 2, $0.80, 1.60, 0.50, 1.00, 0.60; Pear 1, $1.90, 1.90, 1.50, 1.50, 0.40; Total –, –, $9.50, –, $6.00, $3.50. Return

West Brothers Forecasted Contribution Margin Income Statement at Break-Even Sales: Builder grade (23,577 at $6.25) $147,358, Architectural (14,146 at 7.75) 109,634, Restoration (9,431 at $9.25) 87,236; Total Sales 344,228; Variable Costs: Builder grade (23,577 at $3.25) 76,626, Architectural (14,146 at 4.50) 63,659, Restoration (9,431 at $6.25) 58,943; Total Variable Costs 199,228, Contribution Margin 145,000 less Fixed Costs 145,000 equals Net Income of 0. Return

Product: A, B; Composite per unit sales (SP times mix): $10 times 3 equals $30, 49 times 1 equals $9. Total equals $39. Composite per unit variable cost (VC times mix): $4 times 3 equals $12, $5 times 1 equals $5. Total equals $17. Composite per unit contribution margin: $18, $4. Total equals $22. Break-even point per composite unit equals FC divided by composite CM 10,000 units minus $220,000 divided by $22. Return

Number of units per product (mix times units in one composite unit): A, 3 times 10,000, 30,000; B, 1 times 10,000, 10,000. Composite sales (unit SP times product composite units): Product A $10 times 30,000 units, $30,000; Product B $9 times 10,000 units, $90,000; Total sales $390,000. Composite variable costs (unit VC times product composite units): Product A $4 times 30,000 units, $120,000; Product B $5 times 10,000 units, $50,000; Total variable cost $170,000. Contribution Margin (sales minus VC) $220,000. Fixed costs $220,000. Net Income $0. Return