8.1 Job Order v. Process Costing

Job Order Costing versus Process Costing

Job order costing is an accounting system that traces the individual costs directly to a final job or service, instead of to the production department. It is used when goods are made to order or when individual costs are easy to trace to individual jobs, assuming that the additional information provides value. In these circumstances, the individual costs are easy to trace to the individual jobs.

For example, assume that a homeowner wants to have a custom deck added to her home. Also assume that in order to fit her lot’s topography and her anticipated uses for the addition, she needs a uniquely designed deck. Her contractor will design the deck, price the necessary components (in this case, the direct materials, direct labor, and overhead), and construct it.

The final cost will be unique to this project. If another homeowner wanted the contractor to construct a deck, the contractor would go through the same design and pricing process, and you would expect that the design and costs would not be the same as those of the deck in the first example, since the decks would differ from one another.

The job order costing method also works well for companies such as movie production companies, print service providers, advertising agencies, building contractors, accounting firms, consulting entities, and repair service providers. For example, Star Wars: The Last Jedi is believed to have cost $200 million to produce, whereas Logan only cost $97 million. The production processes for both films differed significantly, so that the accumulated costs for each job also differed significantly. Both were made in 2017.1

In contrast, process costing is used when the manufacturing process is continuous, so it is difficult to establish how much of each material is used and exactly how much time is invested in each unit of finished product. Therefore, in process costing, costs are accounted for by the production process or production department instead of by the product or by the job. This method works well for manufacturers of products such as Titleist golf balls, Kellogg’s cereal, Turkey Hill ice cream, CITGO gasoline, Dow Chemicals, or Sherwin Williams’ paints. However, process costing is not limited to basic manufacturing activities: It can also be used in the manufacturing of more complex items, such as small engines. A process costing system assigns costs to each department as the costs are incurred, and the costs to produce one unit are calculated based on the information from the production department. Unit costs are determined after total production costs are determined.

One factor that can complicate the choice between job order costing and process costing is the growth of automation in the production process, which typically is accompanied by a reduction in direct labor. The cost of the increase in equipment (typically reflected as a depreciation expense) is allocated to overhead, while the decreased need for labor usually reduces the direct labor cost. Because of these issues, some companies choose a hybrid system, using process costing to account for mass producing a part and using job order costing to account for assembling some of those individual parts into a custom product. Table 8.1 summarizes the use of these two systems.

| Job Order Cost System | Process Cost System | |

|---|---|---|

| Product type | Custom order | Mass production |

| Examples | Signs, buildings, tax returns | Folding tables, toys, buffet restaurants |

| Cost accumulation | Job lot | Accumulated per process |

| Work in process inventory | Individual job cost sheets | Separate work in process inventory department |

| Record keeping | Individual job cost sheets | Production cost report |

To illustrate how a company can determine whether to use job order costing or process costing, consider the cost accounting options for a local restaurant. Macs & Cheese makes specialty macaroni and cheese, and the company wants to erect a special sign on an already constructed billboard outside a stadium. It wants to use this space to target stadium customers; thus, the company wants a sign built specifically for that site. Dinosaur Vinyl is secured as the sign manufacturer and would use job order costing to account for the associated manufacturing costs because of the unique nature of the sign, including the art work involved. However, if Macs & Cheese was designing a costing system for the specialty food product they market, they typically would use a process costing approach because their product is made and marketed in homogeneous, similar batches.

Organization of Flow of Goods through Production

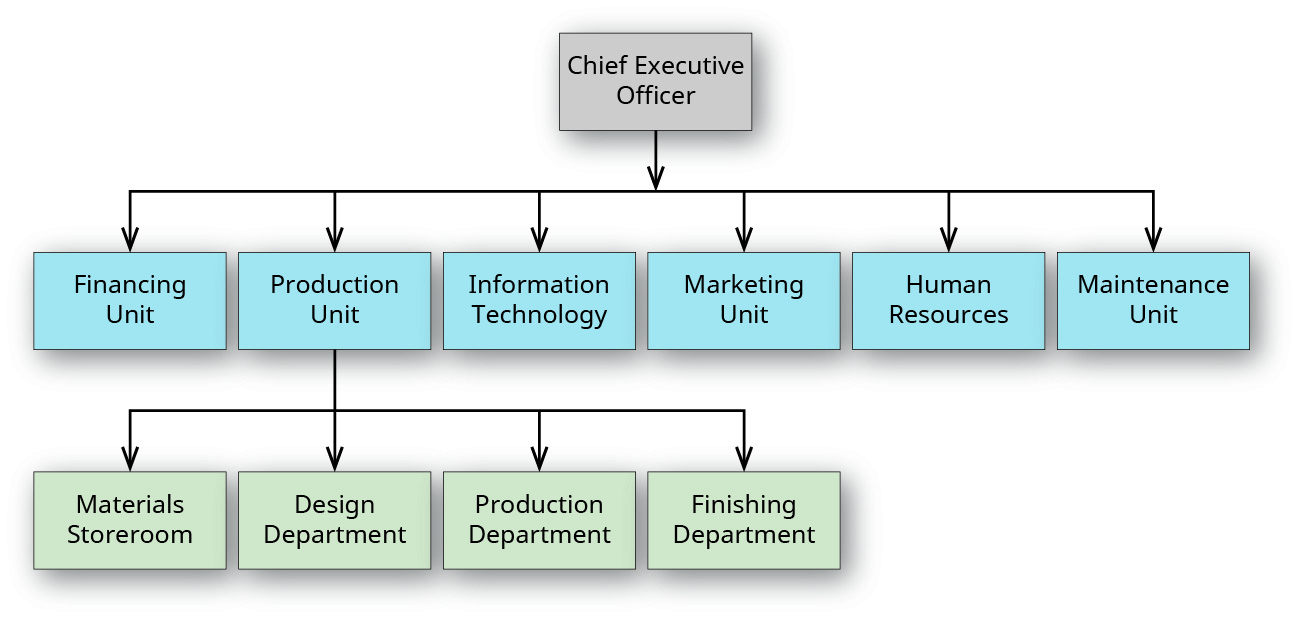

Regardless of the costing method used (job order costing, process costing, or another method), manufacturing companies are generally similar in their organizational structure and have a similar flow of goods through production. The diagram in Figure 8.1 shows a partial organizational chart for sign manufacturer Dinosaur Vinyl. The CEO has several direct reporting units—Financing, Production, Information Technology, Marketing, Human Resources, and Maintenance—each with a director responsible for several departments.

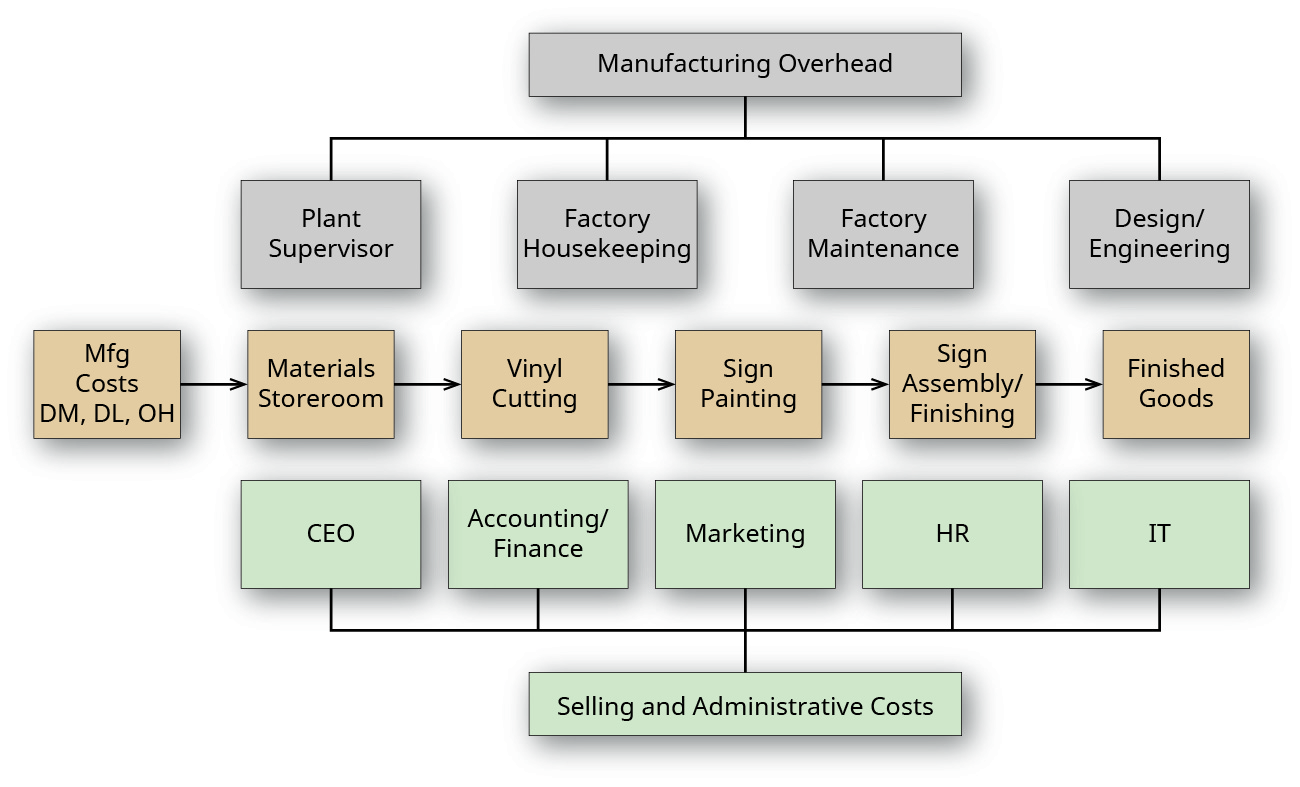

The diagram also shows the departments that report to the production unit director and gives an indication as to the flow of goods through production. The flow of goods through production is more evident in Figure 8.2, which depicts Dinosaur Vinyl as a simple factory with three stages of production.

Raw materials are stored in the materials storeroom and delivered to the appropriate production department—cutting, painting, or assembly/finishing. The design department uses direct labor to create the design specifications, and, when completed, it sends them to the production department. The production department uses the material and design specifications and adds additional labor to create the sign. The sign is transferred to the finishing department for final materials and labor, before the sign is installed or delivered to the customer.

Manufacturing Costs

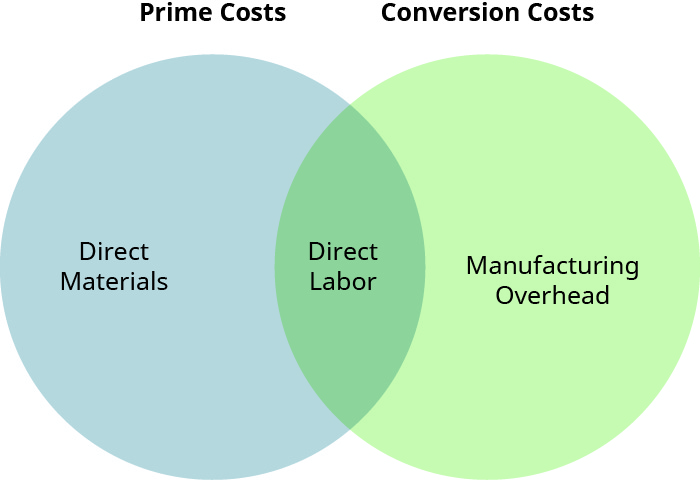

In a manufacturing environment, the manufacturing costs are also called product costs and include all expenses used to manufacture the product: direct materials, direct labor, and manufacturing overhead. The total of these costs becomes the cost of ending inventory and later becomes the cost of goods sold when the product is sold. Both job order costing and process costing use categorized cost information to make decisions and evaluate the effectiveness of the cost tracking process. Because of the difference in how each of the two costing systems track costs, different terminology is used. Thus, it is important to separate product costs from period costs, and it is sometimes important to separate product costs into prime costs and conversion costs. Prime costs are costs that include the primary (or direct) product costs: direct materials and direct labor. Conversion costs are costs that include the expenses necessary to convert direct materials into a finished product: direct labor and manufacturing overhead. Their relationship is shown in Figure 8.3.

Job order costing systems assign costs directly to the product by assigning direct materials and direct labor to the work in process (WIP) inventory. As you learned previously, direct materials are the components that can be directly traced to the products produced, whereas direct labor is the labor cost that can be directly traced to the products produced.

Material and labor costs that cannot be traced directly to the product produced are included in the overhead costs that are allocated in the production costing process. Overhead is applied to each product based on an activity base, which will be explained later in this chapter.

The assignment of direct materials and direct labor to each production unit illustrates the job order costing system’s focus on prime costs, in contrast to the process costing system, which assigns costs to the department and focuses on direct materials and conversion costs, which are composed of a combination of direct labor and overhead.

Selling and Administrative Costs

Selling and administrative costs (S&A) are period costs, and these costs are expensed as incurred, instead of being included in the product’s costs, as they move through the relevant inventory accounts. A period cost is a cost tied to a specific time period, such as a month, quarter, or year, instead of being associated with a particular job order. For example, if a company paid an insurance company $12,000 for one year’s liability insurance coverage, the first month’s expense would be $1,000. This expense would not be related to a particular job order, but instead would be classified as a period cost, and in this case recorded monthly as an administrative expense. Selling costs are the expenses related to the promotion and sale of the company’s products, whereas administrative costs are the expenses related to the operations of the company. The S&A costs are considered period costs because they include costs of departments not directly associated with manufacturing but necessary to operate the business. Some examples include research and development costs, marketing costs, sales commissions, administration building rent, the CEO’s salary expense, and accounting, payroll, and IT department expenses.

YOUR TURN

Maria’s Market

A grocery store’s analysis of a recent customer survey finds an increasing number of customers interested in being able to custom-order meals to go. Maria sees this as an opportunity to enter a niche market for busy families or individuals who want home-cooked meals with a variety of options and combinations, but who have little time. Maria already has an expansive deli, bakery, and prepared foods section in the store and sees this opportunity as a viable option to increase sales and its customer base. With meals to go, customers can choose from an array of options and can indicate the quantity of each item and the time of pickup. The customer simply pulls up in a designated spot at Maria’s and the food is brought to their car, packaged, and ready to take home to enjoy.

What type of costing system will work best for the Maria’s Market? What sales price information, cost information, and other options are important to this decision?

Solution

A job order cost system will work well for this store. In addition to specific price and cost, these are other important considerations.

- The optimal sales price should be set to encourage customers to purchase the meals.

- The materials, labor, and overhead cost should be considered for each meal option.

- Direct material costs may include the cost of the protein, grain, and vegetable option, as well as the cost of the packing containers.

- The direct labor cost is for employees who are directly involved in preparing the meals.

- Manufacturing overhead includes the cost of gloves used when preparing the meals, the cost of employees who support but are not directly involved in preparing the meals, and the cost to operate the oven.

- The cost of the various meal options should all be less than the sales price.

- The meal options should change to take advantage of seasonal items.

- There may be a need to vary the sales price, depending on the combinations selected.

Recording Costs in Job Order Costing versus Process Costing

Both job order costing and process costing track the costs of materials, labor, and overhead as components of virtually all products. The process of production does not change because of the costing method: The costing method is chosen based on the process of production and is intended to provide the most accurate representation of the costs incurred in the production process.

Maintaining accounting records for each system has its advantages. A job order costing system uses a job cost sheet to keep track of individual jobs and the direct materials, direct labor, and overhead associated with each job. The focus of a job order costing system is tracking costs per job, since each job is unique and therefore has different costs relative to other jobs. Maintaining this information is typically more expensive than process costing, and it is often used for the production of smaller, more individualized jobs because the benefit of knowing the cost of each product outweighs the additional cost of maintaining a job order costing system.

In contrast, a process costing system does not need to maintain the cost for individual jobs because the jobs use a continual system of production, and the items are typically not significantly unique but instead are basically equivalent. The accounting emphasis is in keeping records for the individual departments, which is useful for large batches or runs. Process costing is the optimal system to use when the production process is continuous and when it is difficult to trace a particular input cost to an individual product. Process costing systems assign costs to each department as the costs are incurred. The costs to produce one unit are calculated, based on the information from the production department. Therefore, the focus of process costing systems is on measuring and assigning the conversion costs to the proper department in order to best determine the cost of individual units.

Under either costing method, accounting theory explains why it is important to understand when costs become expenses. A primary reason for separating production costs from other company expenses is the expense recognition principle, which requires costs to be expensed when they match the revenue being earned and to separate the costs of production from other costs for the proper timing of recognition of expenses. Think about measuring the profit from the sale of an item, say a TV, in a nonmanufacturing environment. It is logical to subtract the costs associated with buying the TV in order to determine the profit, before applying other costs from that sale. Suppose the TV was purchased as inventory by the store in January and sold to a customer in March. This requires that the cost of the TV not be recorded as an expense (cost of goods sold) until March, when the sale from the TV is recorded, thus matching the revenue with the expense. Until that time, the TV and its cost are considered inventory. This same idea applies to the manufacturing process.

Per the expense recognition principle, product costs—the direct materials, direct labor, and manufacturing overhead incurred to produce the job—are expensed on the income statement for the period of the sale as cost of goods sold when the completed job is sold. If the products are not sold, their costs remain in ending inventory.

Prior to the sale of the product, separating production costs and assigning them to the product results in these costs remaining with the inventory. Until they are sold, the costs incurred are reflected in an assortment of inventory accounts, such as raw materials inventory, work in process inventory, and finished goods inventory.

In contrast, period costs are not directly related to the production process and are expensed during the period in which they are incurred. This approach matches administrative and other expenses shown on the income statement in the same period in which the company earns income.

Long Descriptions

An organizational chart with three tiers. The first tier is labeled “Chief Executive Officer”. The second tier branches from the first, and is labeled from left to right “Financing Unit”, “Production Unit”, “Information Technology”, “Marketing Unit”, “Human Resources”, and “Maintenance Unit”. The third tier branches from “Production Unit” and is labeled “Materials Storeroom”, “Design Department”, “Production Department”, and “Finishing Department”. Return

A factory floor layout from above, showing three rows of departments. The top row is labeled “Manufacturing Overhead” and includes “Plant Supervisor”, “Factory Housekeeping”, “Factory Maintenance”, and “Design/engineering”. The middle row is labeled “Manufacturing Costs, DM, DL, OH) and includes “Materials Storeroom”, “Vinyl Cutting”, Sign Painting”, “Sign Assembly/Finishing”, and “Finished Goods.” The bottom row is labeled “Selling and Administrative Costs” and includes “CEO”, “Accounting/Finance”, “Marketing”, “HR”, and “IT”. Return

Footnotes

- 1 “Production Costs and Global Box Office Revenue of Star Wars Movies from 1977 to 2018 (in million U.S. dollars).” The Statistics Portal. https://www.statista.com/statistics/311356/star-wars-production-costs-box-office-revenue/.