2.2 Perpetual v. Periodic Inventory Systems

[latex][/latex]

There are two ways in which a company may account for their inventory. They can use a perpetual or periodic inventory system. Let’s look at the characteristics of these two systems.

Characteristics of the Perpetual and Periodic Inventory Systems

A perpetual inventory system automatically updates and records the inventory account every time a sale, or purchase of inventory, occurs. You can consider this “recording as you go.” The recognition of each sale or purchase happens immediately upon sale or purchase.

A periodic inventory system updates and records the inventory account at certain, scheduled times at the end of an operating cycle. The update and recognition could occur at the end of the month, quarter, and year. There is a gap between the sale or purchase of inventory and when the inventory activity is recognized.

Generally Accepted Accounting Principles (GAAP) do not state a required inventory system, but the periodic inventory system uses a Purchases account to meet the requirements for recognition under GAAP. IFRS requirements are very similar. The main difference is that assets are valued at net realizable value and can be increased or decreased as values change. Under GAAP, once values are reduced they cannot be increased again.

Inventory Systems Comparison

There are some key differences between perpetual and periodic inventory systems. When a company uses the perpetual inventory system and makes a purchase, they will automatically update the Merchandise Inventory account. Under a periodic inventory system, Purchases will be updated, while Merchandise Inventory will remain unchanged until the company counts and verifies its inventory balance. This count and verification typically occur at the end of the annual accounting period, which is often on December 31 of the year. The Merchandise Inventory account balance is reported on the balance sheet while the Purchases account is reported on the Income Statement when using the periodic inventory method. The Cost of Goods Sold is reported on the Income Statement under the perpetual inventory method.

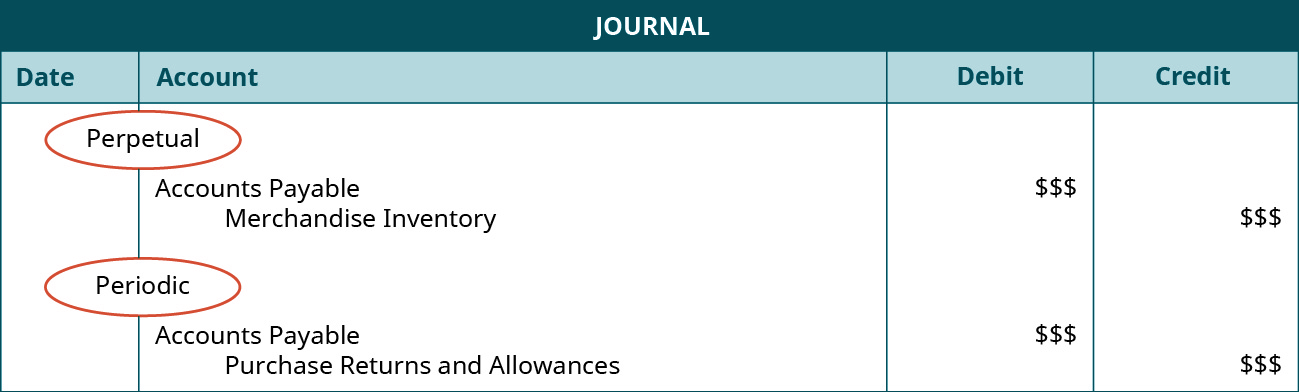

A purchase return or allowance under perpetual inventory systems updates Merchandise Inventory for any decreased cost. Under periodic inventory systems, a temporary account, Purchase Returns and Allowances, is updated. Purchase Returns and Allowances is a contra account and is used to reduce Purchases.

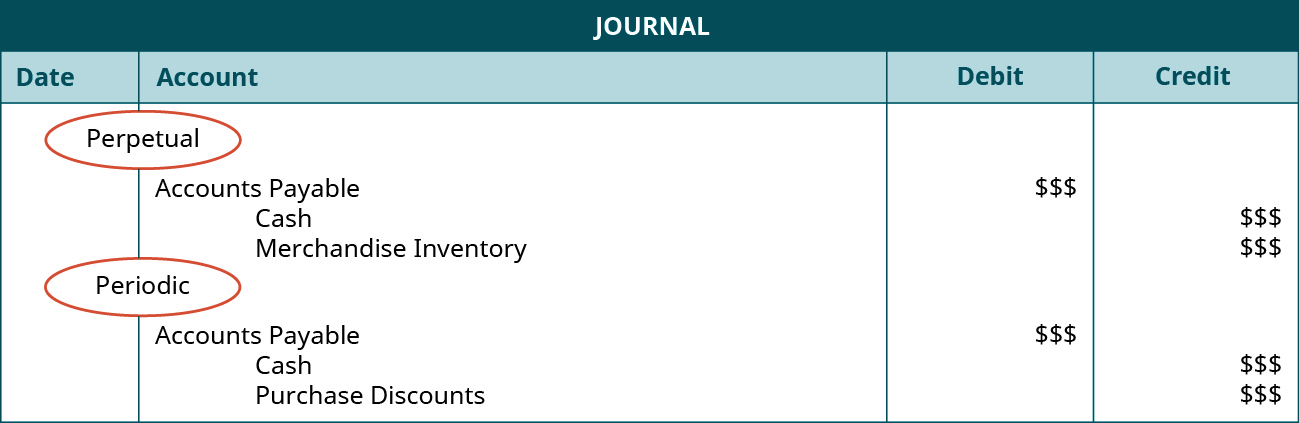

When a purchase discount is applied under a perpetual inventory system, Merchandise Inventory decreases for the discount amount. Under a periodic inventory system, Purchase Discounts (a temporary, contra account), increases for the discount amount and Merchandise Inventory remains unchanged.

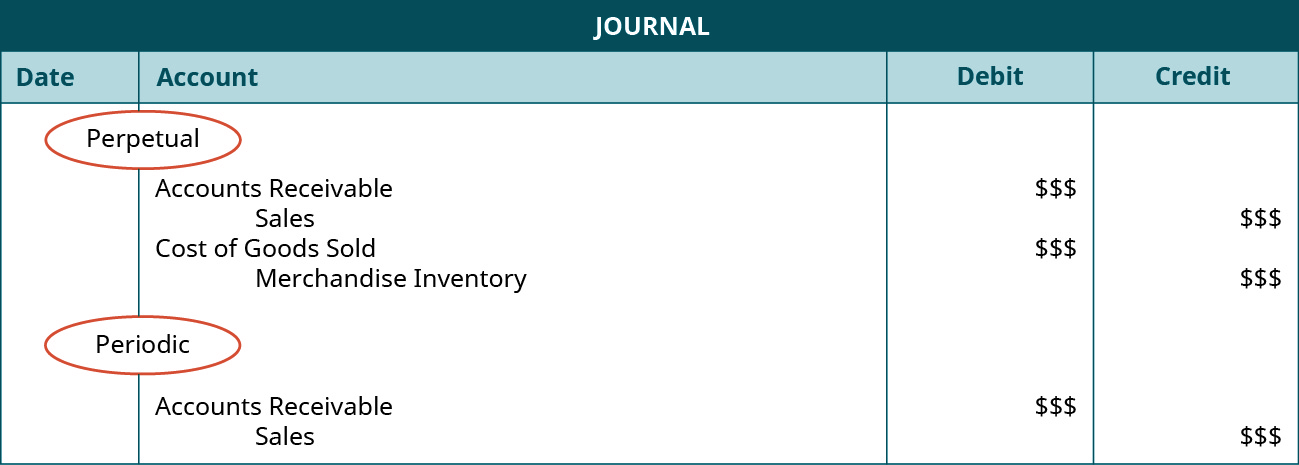

When a sale occurs under perpetual inventory systems, two entries are required: one to recognize the sale, and the other to recognize the cost of sale. For the cost of sale, Merchandise Inventory and Cost of Goods Sold are updated. Under periodic inventory systems, this cost of sale entry does not exist. The recognition of merchandise cost only occurs at the end of the period when adjustments are made and temporary accounts are closed.

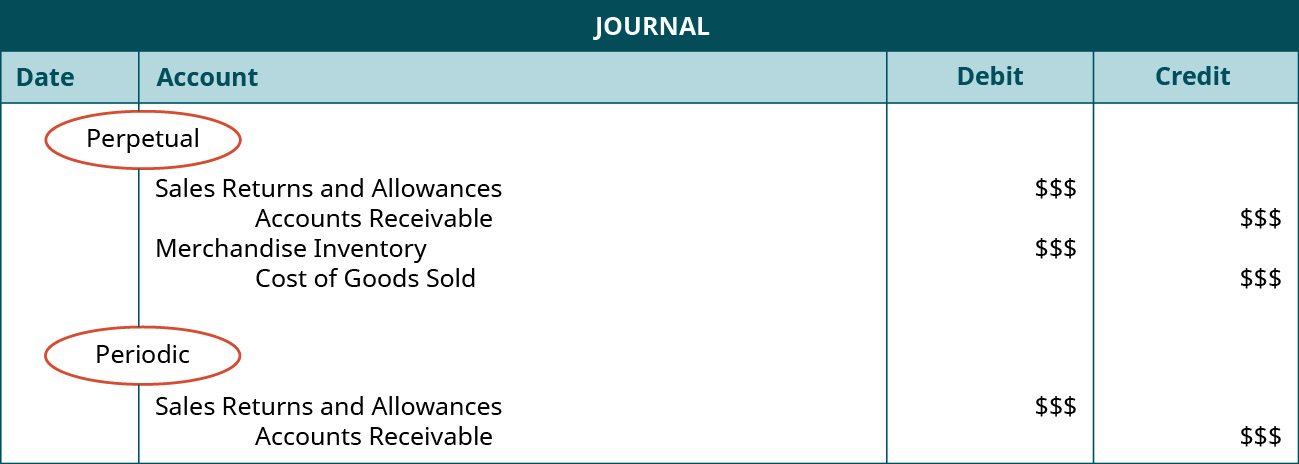

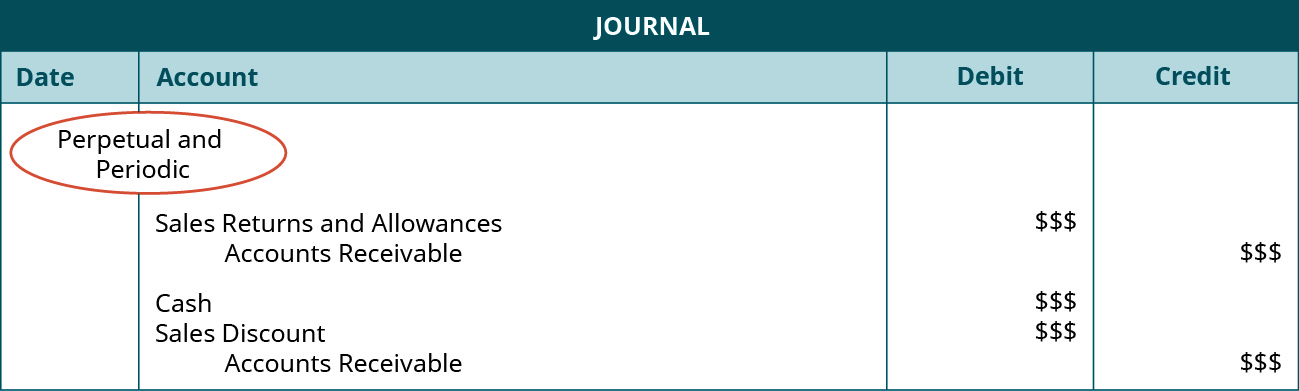

When a sales return occurs, perpetual inventory systems require recognition of the inventory’s condition. This means a decrease to COGS and an increase to Merchandise Inventory. Under periodic inventory systems, only the sales return is recognized, but not the inventory condition entry.

A sales allowance and sales discount follow the same recording formats for either perpetual or periodic inventory systems.

Adjusting and Closing Entries for a Perpetual Inventory System

You have already explored adjusting entries and the closing process in prior discussions, but merchandising activities require additional adjusting and closing entries to inventory, sales discounts, returns, and allowances. Here, we’ll briefly discuss these additional closing entries and adjustments as they relate to the perpetual inventory system.

At the end of the period, a perpetual inventory system will have the Merchandise Inventory account up-to-date; the only thing left to do is to compare a physical count of inventory to what is on the books. A physical inventory count requires companies to do a manual “stock-check” of inventory to make sure what they have recorded on the books matches what they physically have in stock. Differences could occur due to mismanagement, shrinkage, damage, or outdated merchandise. Shrinkage is a term used when inventory or other assets disappear without an identifiable reason, such as theft. For a perpetual inventory system, the adjusting entry to show this difference follows. This example assumes that the merchandise inventory is overstated in the accounting records and needs to be adjusted downward to reflect the actual value on hand.

If a physical count determines that merchandise inventory is understated in the accounting records, Merchandise Inventory would need to be increased with a debit entry and the COGS would be reduced with a credit entry. The adjusting entry is:

To sum up the potential adjustment process, after the merchandise inventory has been verified with a physical count, its book value is adjusted upward or downward to reflect the actual inventory on hand, with an accompanying adjustment to the COGS.

Not only must an adjustment to Merchandise Inventory occur at the end of a period, but closure of temporary merchandising accounts to prepare them for the next period is required. Temporary accounts requiring closure are Sales, Sales Discounts, Sales Returns and Allowances, and Cost of Goods Sold. Sales will close with the temporary credit balance accounts to Income Summary.

Sales Discounts, Sales Returns and Allowances, and Cost of Goods Sold will close with the temporary debit balance accounts to Income Summary.

Note that for a periodic inventory system, the end of the period adjustments require an update to COGS. To determine the value of Cost of Goods Sold, the business will have to look at the beginning inventory balance, purchases, purchase returns and allowances, discounts, and the ending inventory balance.

The formula to compute COGS is:

where:

Once the COGS balance has been established, an adjustment is made to Merchandise Inventory and COGS, and COGS is closed to prepare for the next period.

Table 2.1 summarizes the differences between the perpetual and periodic inventory systems.

| Transaction | Perpetual Inventory System | Periodic Inventory System |

|---|---|---|

| Purchase of Inventory | Record cost to Inventory account | Record cost to Purchases account |

| Purchase Return or Allowance | Record to update Inventory | Record to Purchase Returns and Allowances |

| Purchase Discount | Record to update Inventory | Record to Purchase Discounts |

| Sale of Merchandise | Record two entries: one for sale and one for cost of sale | Record one entry for the sale |

| Sales Return | Record two entries: one for sales return, one for cost of inventory returned | Record one entry: sales return, cost not recognized |

| Sales Allowance | Same under both systems | Same under both systems |

| Sales Discount | Same under both systems | Same under both systems |

There are advantages and disadvantages to both the perpetual and periodic inventory systems.

CONCEPTS IN PRACTICE

Point-of-Sale Systems

Advancements in point-of-sale (POS) systems have simplified the once tedious task of inventory management. POS systems connect with inventory management programs to make real-time data available to help streamline business operations. The cost of inventory management decreases with this connection tool, allowing all businesses to stay current with technology without “breaking the bank.”

One such POS system is Square. Square accepts many payment types and updates accounting records every time a sale occurs through a cloud-based application. Square, Inc. has expanded their product offerings to include Square for Retail POS. This enhanced product allows businesses to connect sales and inventory costs immediately. A business can easily create purchase orders, develop reports for cost of goods sold, manage inventory stock, and update discounts, returns, and allowances. With this application, customers have payment flexibility, and businesses can make present decisions to positively affect growth.

Advantages and Disadvantages of the Perpetual Inventory System

The perpetual inventory system gives real-time updates and keeps a constant flow of inventory information available for decision-makers. With advancements in point-of-sale technologies, inventory is updated automatically and transferred into the company’s accounting system. This allows managers to make decisions as it relates to inventory purchases, stocking, and sales. The information can be more robust, with exact purchase costs, sales prices, and dates known. Although a periodic physical count of inventory is still required, a perpetual inventory system may reduce the number of times physical counts are needed.

The biggest disadvantages of using the perpetual inventory systems arise from the resource constraints for cost and time. It is costly to keep an automatic inventory system up-to-date. This may prohibit smaller or less established companies from investing in the required technologies. The time commitment to train and retrain staff to update inventory is considerable. In addition, since there are fewer physical counts of inventory, the figures recorded in the system may be drastically different from inventory levels in the actual warehouse. A company may not have correct inventory stock and could make financial decisions based on incorrect data.

Advantages and Disadvantages of the Periodic Inventory System

The periodic inventory system is often less expensive and time consuming than perpetual inventory systems. This is because there is no constant maintenance of inventory records or training and retraining of employees to upkeep the system. The complexity of the system makes it difficult to identify the cost justification associated with the inventory function.

While both the periodic and perpetual inventory systems require a physical count of inventory, periodic inventorying requires more physical counts to be conducted. This updates the inventory account more frequently to record exact costs. Knowing the exact costs earlier in an accounting cycle can help a company stay on budget and control costs.

However, the need for frequent physical counts of inventory can suspend business operations each time this is done. There are more chances for shrinkage, damaged, or obsolete merchandise because inventory is not constantly monitored. Since there is no constant monitoring, it may be more difficult to make in-the-moment business decisions about inventory needs.

While each inventory system has its own advantages and disadvantages, the more popular system is the perpetual inventory system. The ability to have real-time data to make decisions, the constant update to inventory, and the integration to point-of-sale systems, outweigh the cost and time investments needed to maintain the system.