1.13 The Worksheet

Here’s a short video describing how accountants use a worksheet to facilitate the creation of the adjusted trial balance, financial statements and closing entries.

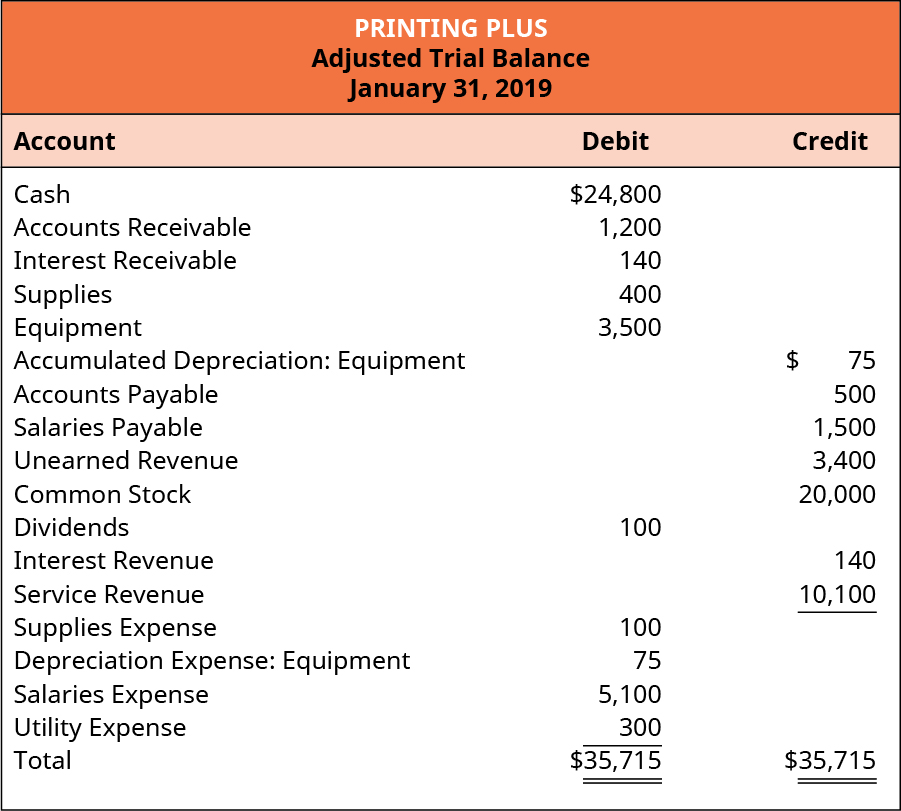

Once all of the adjusting entries have been posted to the general ledger, we are ready to start working on preparing the adjusted trial balance. Preparing an adjusted trial balance is the sixth step in the accounting cycle. An adjusted trial balance is a list of all accounts in the general ledger, including adjusting entries, which have nonzero balances. This trial balance is an important step in the accounting process because it helps identify any computational errors throughout the first five steps in the cycle.

As with the unadjusted trial balance, transferring information from T-accounts to the adjusted trial balance requires consideration of the final balance in each account. If the final balance in the ledger account (T-account) is a debit balance, you will record the total in the left column of the trial balance. If the final balance in the ledger account (T-account) is a credit balance, you will record the total in the right column.

Once all ledger accounts and their balances are recorded, the debit and credit columns on the adjusted trial balance are totaled to see if the figures in each column match. The final total in the debit column must be the same dollar amount that is determined in the final credit column.

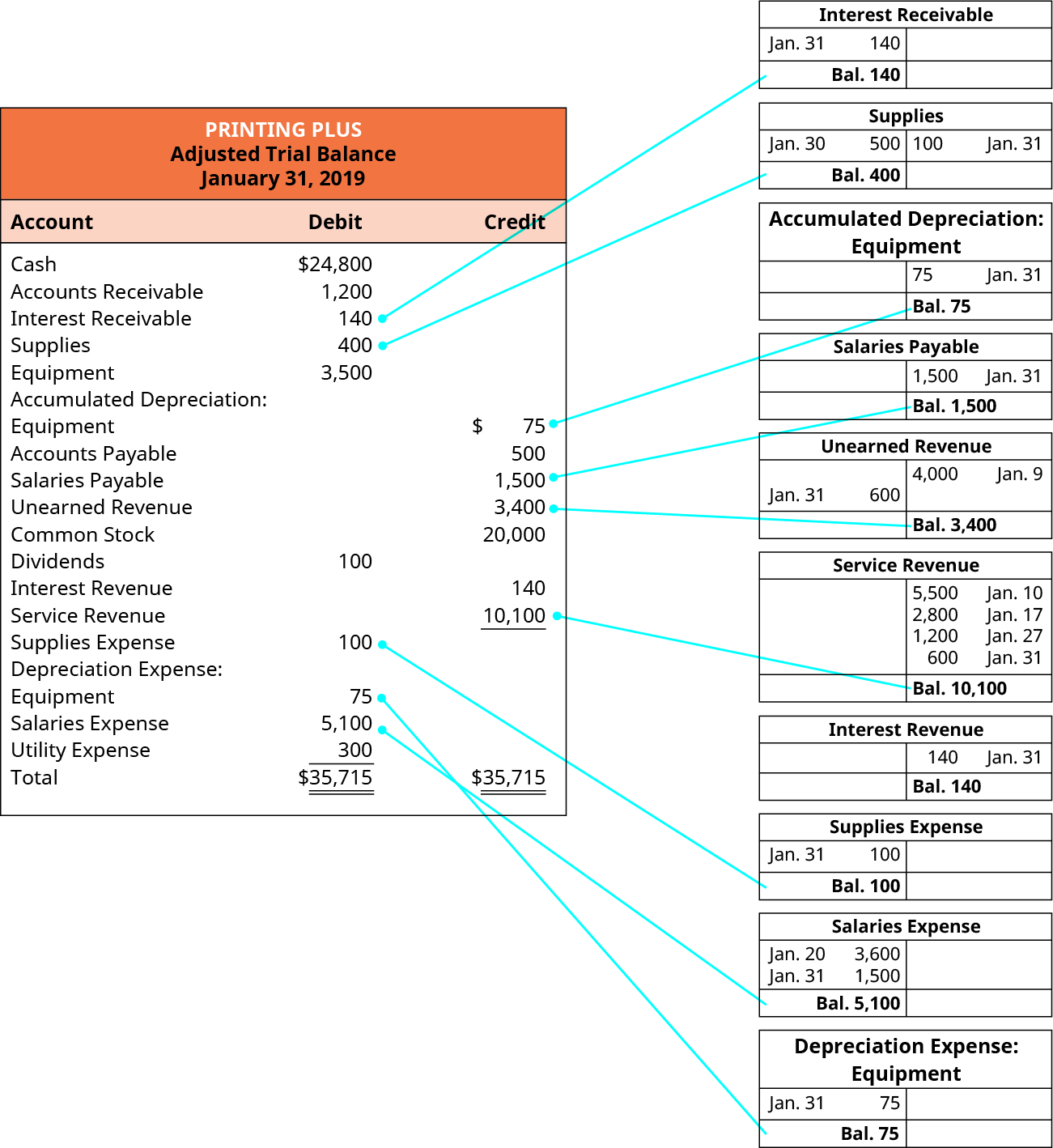

Let’s now take a look at the adjusted T-accounts and adjusted trial balance for Printing Plus to see how the information is transferred from these T-accounts to the adjusted trial balance. We only focus on those general ledger accounts that had balance adjustments.

For example, Interest Receivable is an adjusted account that has a final balance of $140 on the debit side. This balance is transferred to the Interest Receivable account in the debit column on the adjusted trial balance. Supplies ($400), Supplies Expense ($100), Salaries Expense ($5,100), and Depreciation Expense–Equipment ($75) also have debit final balances in their adjusted T-accounts, so this information will be transferred to the debit column on the adjusted trial balance. Accumulated Depreciation–Equipment ($75), Salaries Payable ($1,500), Unearned Revenue ($3,400), Service Revenue ($10,100), and Interest Revenue ($140) all have credit final balances in their T-accounts. These credit balances would transfer to the credit column on the adjusted trial balance.

Once all balances are transferred to the adjusted trial balance, we sum each of the debit and credit columns. The debit and credit columns both total $35,715, which means they are equal and in balance.

After the adjusted trial balance is complete, we next prepare the company’s financial statements.

Long Descriptions

Printing Plus Adjusted Trial Balance, January 31, 2019. Debit accounts: Cash $24,800; Accounts Receivable 1,200; Interest Receivable 140; Supplies 400; Equipment 3,500; Dividends 100; Supplies Expense 100; Depreciation Expense Equipment 75; Salaries Expense 5,100; Utility Expense 300; Total Debits $35,715. Credit accounts: Accumulated Depreciation: Equipment 75; Accounts Payable 500; Salaries Payable 1,500; Unearned Revenue 3,400; Common Stock 20,000; Interest Revenue 140; Service Revenue 10,100; Total Credits $35,715. To the right of the adjusted trial balance are ten T-accounts, highlighting the January 31 adjusting entries, with lines connecting the balances of the T-accounts to the adjusted trial balance. The ten T-accounts, in order, are: Interest Receivable, debit balance 140. Supplies, debit balance 400. Accumulated Depreciation: Equipment, credit balance 75. Salaries Payable, credit balance 1,500. Unearned Revenue, credit balance 3,400. Service Revenue, credit balance 10,100. Interest Revenue, credit balance 140. Supplies Expense, debit balance 100. Salaries Expense, debit balance 5,100. Depreciation Expense Equipment, debit balance 75. Return

Printing Plus Adjusted Trial Balance, January 31, 2019. Debit accounts: Cash $24,800; Accounts Receivable 1,200; Interest Receivable 140; Supplies 400; Equipment 3,500; Dividends 100; Supplies Expense 100; Depreciation Expense: Equipment 75; Salaries Expense 5,100; Utility Expense 300; Total Debits $35,715. Credit accounts: Accumulated Depreciation: Equipment 75; Accounts Payable 500; Salaries Payable 1,500; Unearned Revenue 3,400; Common Stock 20,000; Interest Revenue 140; Service Revenue 10,100; Total Credits $35,715. Return