10.4 Flexible Budgets

A company makes a budget for the smallest time period possible so that management can find and adjust problems to minimize their impact on the business. Everything starts with the estimated sales, but what happens if the sales are more or less than expected? How does this affect the budget? What adjustments does a company have to make in order to compare the actual numbers to budgeted numbers when evaluating results? If production is higher than planned and has been increased to meet the increased sales, expenses will be over budget. But is this bad? To account for actual sales and expenses differing from budgeted sales and expenses, companies will often create flexible budgets to allow budgets to fluctuate with future demand.

Flexible Budgets

A flexible budget is one based on different volumes of sales. A flexible budget flexes the static budget for each anticipated level of production. This flexibility allows management to estimate what the budgeted numbers would look like at various levels of sales. Flexible budgets are prepared at each analysis period (usually monthly), rather than in advance, since the idea is to compare the operating income to the expenses deemed appropriate at the actual production level.

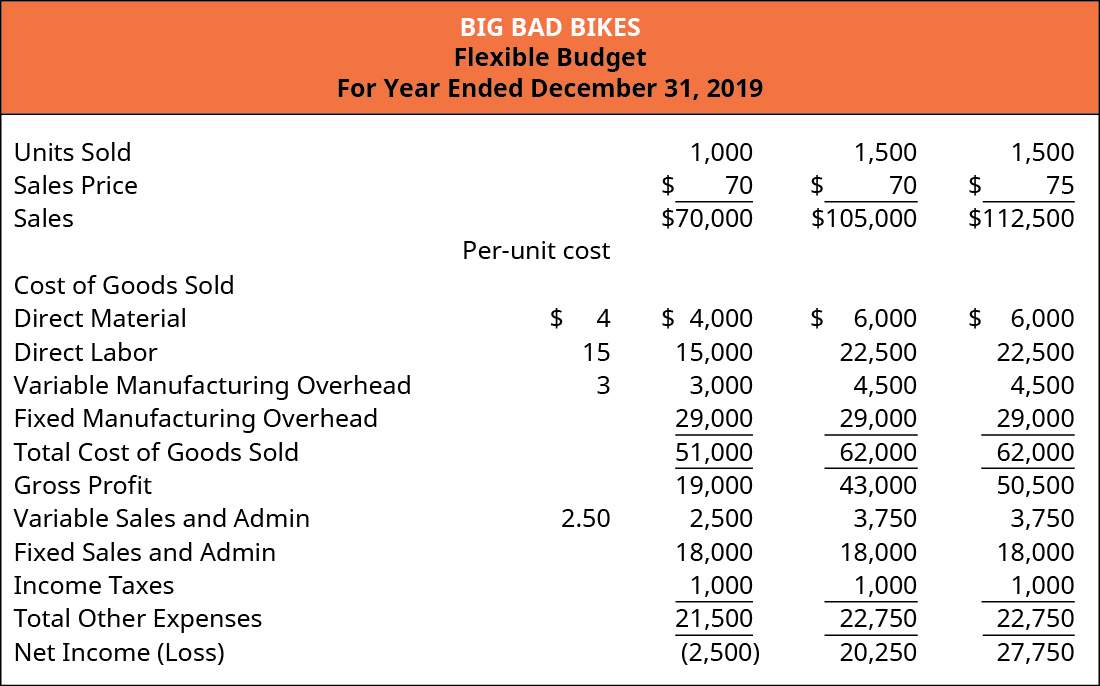

Big Bad Bikes is planning to use a flexible budget when they begin making trainers. The company knows its variable costs per unit and knows it is introducing its new product to the marketplace. Its estimations of sales and sales price will likely change as the product takes hold and customers purchase it. Big Bad Bikes developed a flexible budget that shows the change in income and expenses as the number of units changes. It also looked at the effect a change in price would have if the number of units remained the same. The expenses that do not change are the fixed expenses, as shown in Figure 10.25.

Static versus Flexible Budgets

A static budget is one that is prepared based on a single level of output for a given period. The master budget, and all the budgets included in the master budget, are examples of static budgets. Actual results are compared to the static budget numbers as one means to evaluate company performance. However, this comparison may be like comparing apples to oranges because variable costs should follow production, which should follow sales. Thus, if sales differ from what is budgeted, then comparing actual costs to budgeted costs may not provide a clear indicator of how well the company is meeting its targets. A flexible budget created each period allows for a comparison of apples to apples because it will calculate budgeted costs based on the actual sales activity.

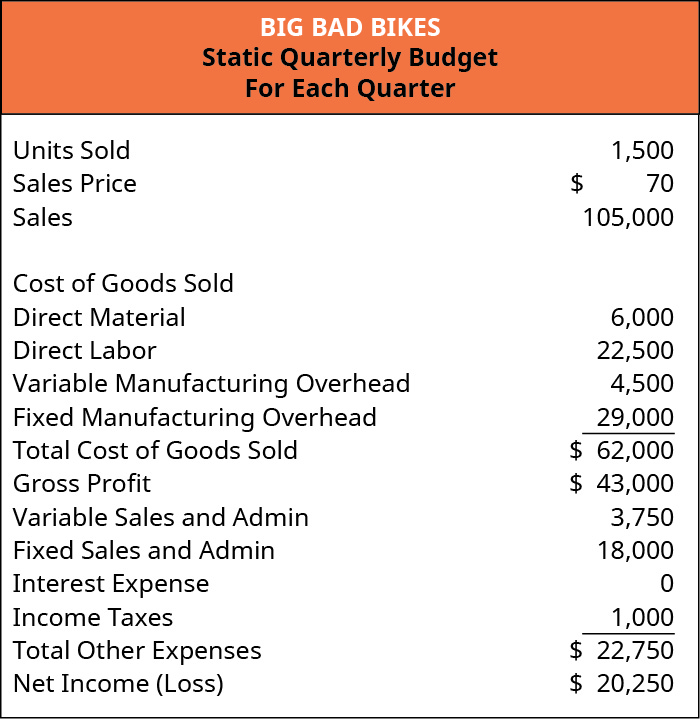

For example, Figure 10.26 shows a static quarterly budget for 1,500 trainers sold by Big Bad Bikes. The budget will change if there are more or fewer units sold.

Budget with Varying Levels of Production

Companies develop a budget based on their expectations for their most likely level of sales and expenses. Often, a company can expect that their production and sales volume will vary from budget period to budget period. They can use their various expected levels of production to create a flexible budget that includes these different levels of production. Then, they can modify the flexible budget when they have their actual production volume and compare it to the flexible budget for the same production volume. A flexible budget is more complicated, requires a solid understanding of a company’s fixed and variable expenses, and allows for greater control over changes that occur throughout the year. For example, suppose a proposed sale of items does not occur because the expected client opted to go with another supplier. In a static budget situation, this would result in large variances in many accounts due to the static budget being set based on sales that included the potential large client. A flexible budget on the other hand would allow management to adjust their expectations in the budget for both changes in costs and revenue that would occur from the loss of the potential client. The changes made in the flexible budget would then be compared to what actually occurs to result in more realistic and representative variance. This ability to change the budget also makes it easier to pinpoint who is responsible if a revenue or cost target is missed.

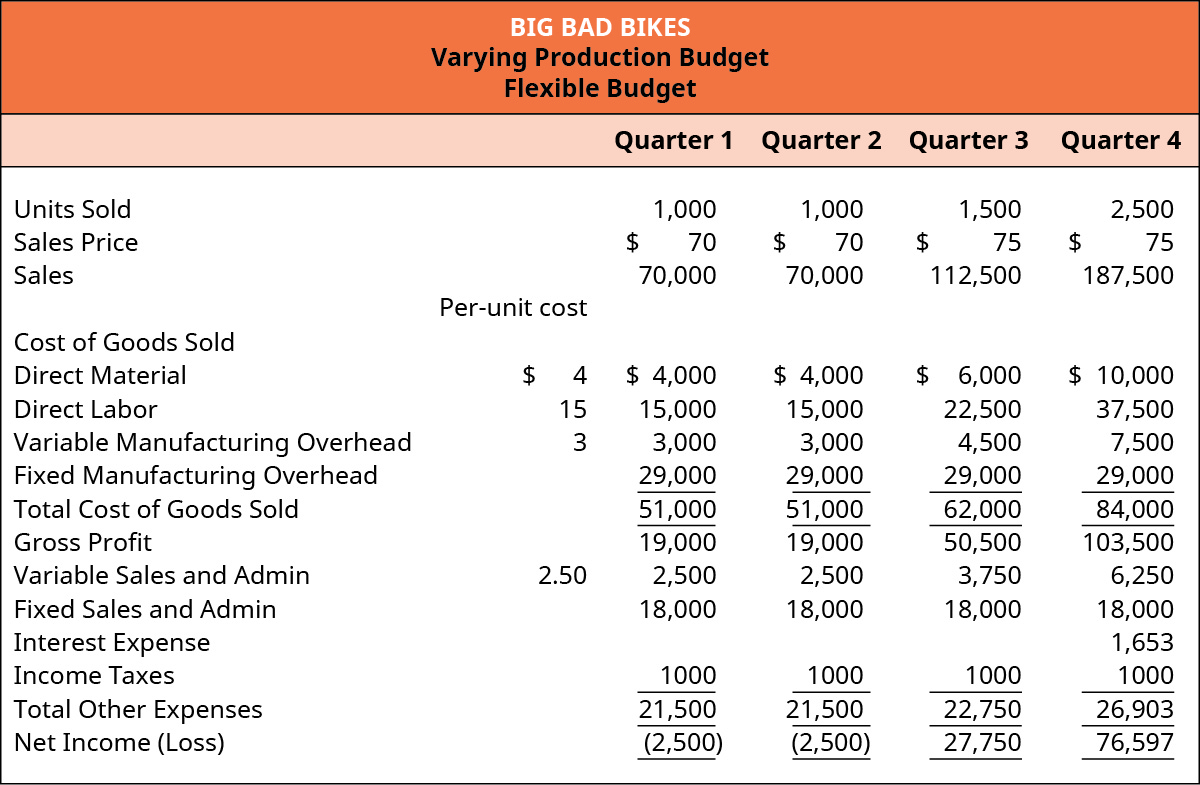

Big Bad Bikes used the flexible budget concept to develop a budget based on its expectation that production levels will vary by quarter. By the fourth quarter, sales are expected to be strong enough to pay back the financing from earlier in the year. The budget shown in Figure 10.27 illustrates the payment of interest and contains information helpful to management when determining which items should be produced if production capacity is limited.

CONCEPTS IN PRACTICE

Flexible Budgets and Sustainability

The ability to provide flexible budgets can be critical in new or changing businesses where the accuracy of estimating sales or usage my not be strong. For example, organizations are often reporting their sustainability efforts and may have some products that require more electricity than other products. The reporting of the energy per unit of output has sometimes been in error and can mislead management into making changes that may or may not help the company. For example, based on the energy per unit reported, management may decide to change the product mix, the amount that is outsourced, and/or the amount that is produced.1 If the energy output isn’t correct, the decisions may be wrong and create an adverse impact on the budget.

Long Descriptions

A flexible budget for Big Bad Bikes presents three budget scenarios for different quantities of units sold and different sale prices. Per-unit costs are identified: direct material $4, direct labor $15, variable manufacturing overhead $3, and variable sales and admin $3. In the first scenario, 1,000 units are sold at a sales price of $70 for total sales income of $70,000. Budget items for the first scenario are: direct material $4,000, direct labor $15,000, variable manufacturing overhead $3,000, fixed manufacturing overhead $29,000, total cost of goods sold $51,000, gross profit $19,000, variable sales and admin $2,500, fixed sales and admin $18,000, income taxes $1,000, total other expenses $21,500, resulting in a net loss of $2,500. In the second scenario, 1,500 units are sold at a sales price of $70 for total sales income of $105,000. Budget items for the second scenario are: direct material $6,000, direct labor $22,500, variable manufacturing overhead $4,500, fixed manufacturing overhead $29,000, total cost of goods sold $62,000, gross profit $43,000, variable sales and admin $3,750, fixed sales and admin $18,000, income taxes $1,000, total other expenses $22,750, resulting in a net income gain of $20,250. In the third scenario, 1,500 units are sold at a sales price of $75 for total sales income of $112,500. Budget items for the third scenario are: direct material $6,000, direct labor $22,500, variable manufacturing overhead $4,500, fixed manufacturing overhead $29,000, total cost of goods sold $62,000, gross profit $50,500, variable sales and admin $3,750, fixed sales and admin $18,000, income taxes $1,000, total other expenses $22,750, resulting in a net income gain of $27,750. Return

Big Bad Bikes, Static Quarterly Budget for Each Quarter: Units sold 1,500 times Sales price $70 equals Sales $105,000. Budget items are: Direct material $6,000, Direct labor $22,500, Variable manufacturing overhead $4,500, Fixed manufacturing overhead $29,000, Total cost of goods sold $62,000, gross profit $43,000, variable sales and admin $3,750, fixed sales and admin $18,000, no interest expense, income taxes $1,000, total other expenses $22,750, net income $20,250. Return

A varying production budget for Big Bad Bikes presents budget items for four quarters. Per-unit costs are identified: direct material $4, direct labor $15, variable manufacturing overhead $3, and variable sales and admin $3. In the first quarter, 1,000 units are sold at a sales price of $70 for total sales income of $70,000. Budget items for the first quarter are: direct material $4,000, direct labor $15,000, variable manufacturing overhead $3,000, fixed manufacturing overhead $29,000, total cost of goods sold $51,000, gross profit $19,000, variable sales and admin $2,500, fixed sales and admin $18,000, income taxes $1,000, total other expenses $21,500, resulting in a net loss of $2,500. The second quarter is identical to the first quarter. In the third quarter, 1,500 units are sold for a sales price of $75 for total sales income of $112,500. Budget items for the third quarter are: direct material $6,000, direct labor $22,500, variable manufacturing overhead $4,500, fixed manufacturing overhead $29,000, total cost of goods sold $62,000, gross profit $50,500, variable sales and admin $3,750, fixed sales and admin $18,000, income taxes $1,000, total other expenses $22,750, resulting in a net income gain of $27,750. In the fourth quarter, 2,500 units are sold for a sales price of $75 for total sales income of $187,500. Budget items for the fourth quarter are: direct material $10,000, direct labor $37,500, variable manufacturing overhead $7,500, fixed manufacturing overhead $29,000, total cost of goods sold $84,000, gross profit $103,500, variable sales and admin $6,250, fixed sales and admin $18,000, income taxes $1,653, total other expenses $26,903, resulting in a net income gain of $76,597. Return

Footnotes

- 1 Jon Bartley, et al. “Using Flexible Budgeting to Improve Sustainability Measures.: American Institute of CPAs. Jan. 23, 2017. https://www.aicpa.org/interestareas/businessindustryandgovernment/resources/sustainability/improvesustainabilitymeasures.html