2.1 Merchandisers v. Service Providers

Every week, you run errands for your household. These errands may include buying products and services from local retailers, such as gas, groceries, and clothing. As a consumer, you are focused solely on purchasing your items and getting home to your family. You are probably not thinking about how your purchases impact the businesses you frequent. Whether the business is a service or a merchandising company, it tracks sales from customers, purchases from manufacturers or other suppliers, and costs that affect their everyday operations. There are some key differences between these business types in the manner and detail required for transaction recognition.

Comparison of Merchandising Transactions versus Service Transactions

Some of the biggest differences between a service company and a merchandising company are what they sell, their typical financial transactions, their operating cycles, and how these translate to financial statements.

A service company provides intangible services to customers and does not have inventory. Some examples of service companies include lawyers, doctors, consultants, and accountants. Service companies often have simple financial transactions that involve taking customer deposits, billing clients after services have been provided, providing the service, and processing payments. These activities may occur frequently within a company’s accounting cycle and make up a portion of the service company’s operating cycle.

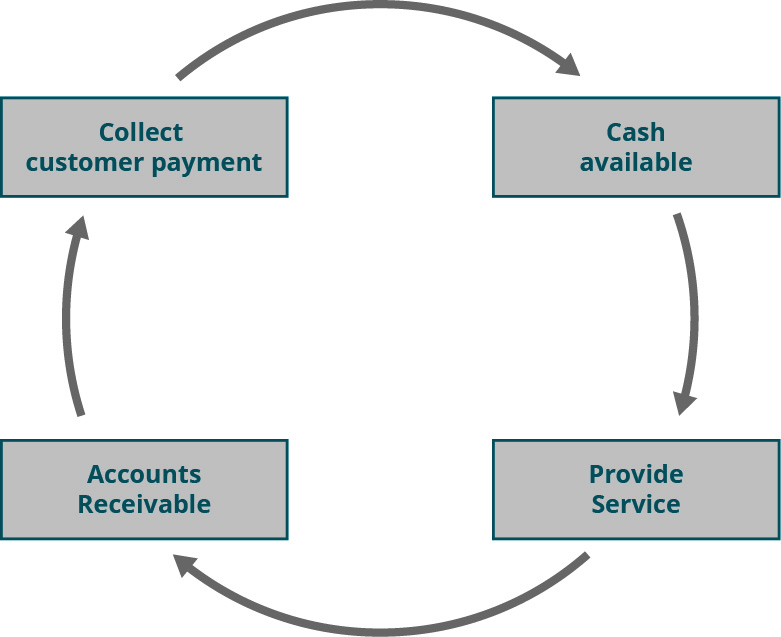

An operating cycle is the amount of time it takes a company to use its cash to provide a product or service and collect payment from the customer. Completing this cycle faster puts the company in a more stable financial position. A typical operating cycle for a service company begins with having cash available, providing service to a customer, and then receiving cash from the customer for the service.

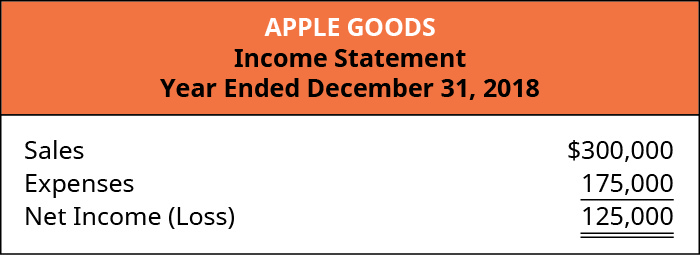

The income statement format is fairly simple as well. Revenues (sales) are reported first, followed by any period operating expenses. The outcome of sales less expenses, which is net income (loss), is calculated from these accounts.

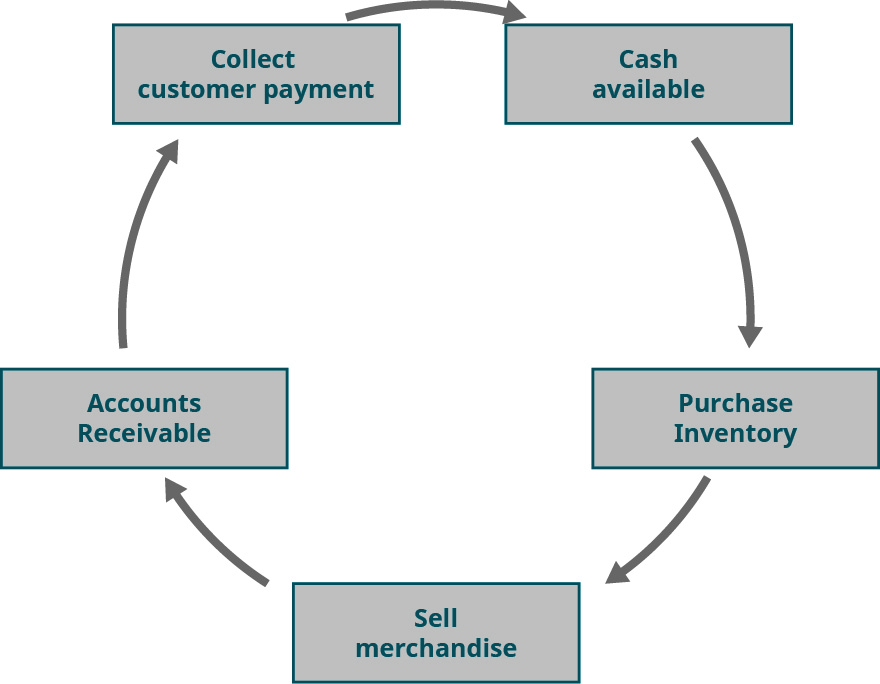

A merchandising company resells finished goods (inventory) produced by a manufacturer (supplier) to customers. Some examples of merchandising companies include Walmart, Macy’s, and Home Depot. Merchandising companies have financial transactions that include: purchasing merchandise, paying for merchandise, storing inventory, selling merchandise, and collecting customer payments. A typical operating cycle for a merchandising company starts with having cash available, purchasing inventory, selling the merchandise to customers, and finally collecting payment from customers.

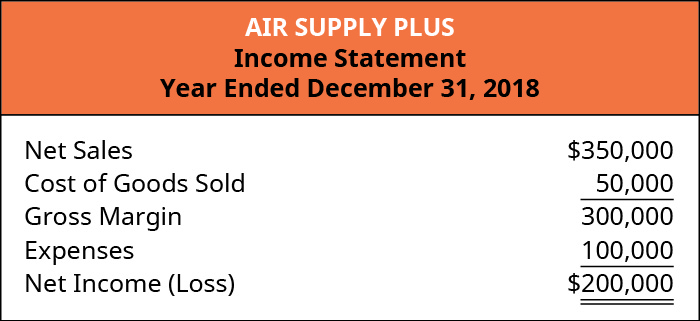

Note that unlike a service company, the merchandiser, also sometimes labeled as a retailer, must first resolve any sale reductions and merchandise costs, known as Cost of Goods Sold, before determining other expenses and net income (loss). A simple retailer income statement is shown in Figure 2.4 for comparison.

Characteristics of Merchandising Transactions

Merchandising transactions are separated into two categories: purchases and sales. In general, a purchase transaction occurs between a manufacturer and the merchandiser, also called a retailer. A sales transaction occurs between a customer and the merchandiser or retailer. We will now discuss the characteristics that create purchase and sales transactions for a retailer. A merchandiser will need to purchase merchandise for its business to continue operations and can use several purchase situations to accomplish this.

Purchases with Cash or on Credit

A retailer typically conducts business with a manufacturer or with a supplier who buys from a manufacturer. The retailer will purchase their finished goods for resale. When the purchase occurs, the retailer may pay for the merchandise with cash or on credit. If the retailer pays for the merchandise with cash, they would be trading one current asset, Cash, for another current asset, Merchandise Inventory or just Inventory, depending upon the company’s account titles. In this example, they would record a debit entry to Merchandise Inventory and a credit entry to Cash. If they decide to pay on credit, a liability would be created, and Accounts Payable would be credited rather than Cash. For example, a clothing store may pay a jeans manufacturer cash for 50 pairs of jeans, costing $25 each. The following entry would occur.

If this same company decides to purchase merchandise on credit, Accounts Payable is credited instead of Cash.

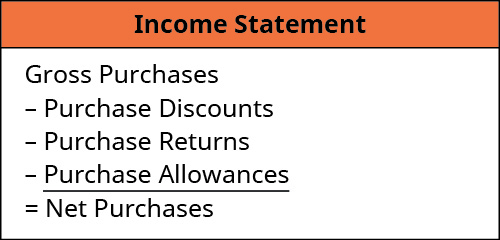

Merchandise Inventory is a current asset account that houses all purchase costs associated with the transaction. This includes the cost of the merchandise, shipping charges, insurance fees, taxes, and any other costs that gets the products ready for sale. Gross purchases are defined as the original amount of the purchase without considering reductions for purchase discounts, returns, or allowances. Once the purchase reductions are adjusted at the end of a period, net purchases are calculated. Net purchases (see Figure 2.7) equals gross purchases less purchase discounts, purchase returns, and purchase allowances.

Purchase Discounts

If a retailer, pays on credit, they will work out payment terms with the manufacturer. These payment terms establish the purchase cost, an invoice date, any discounts, shipping charges, and the final payment due date.

Purchase discounts provide an incentive for the retailer to pay early on their accounts by offering a reduced rate on the final purchase cost. Receiving payment in a timely manner allows the manufacturer to free up cash for other business opportunities and decreases the risk of nonpayment.

To describe the discount terms, the manufacturer can write descriptions such as 2/10, n/30 on the invoice. The “2” represents a discount rate of 2%, the “10” represents the discount period in days, and the “n/30” means “net of 30” days, representing the entire payment period without a discount application. So, “2/10, n/30” reads as, “The company will receive a 2% discount on their purchase if they pay in 10 days. Otherwise, they have 30 days from the date of the sale to pay in full, no discount received.” In some cases, if the retailer exceeds the full payment period (30 days in this example), the manufacturer may charge interest as a penalty for late payment. The number of days allowed for both the discount period and the full payment period begins counting from the invoice date.

If a merchandiser pays an invoice within the discount period, they receive a discount, which affects the cost of the inventory. Let’s say a retailer pays within the discount window. They would need to show a credit to the Merchandise Inventory account, recognizing the decreased final cost of the merchandise. This aligns with the cost principle, which requires a company to record an asset’s value at the cost of acquisition. In addition, since cash is used to pay the manufacturer, Cash is credited. The debit to Accounts Payable does not reflect the discount taken: it reflects fulfillment of the liability in full, and the credits to Merchandise Inventory and Cash reflect the discount taken, as demonstrated in the following example.

If the retailer does not pay within the discount window, they do not receive a discount but are still required to pay the full invoice price at the end of the term. In this case, Accounts Payable is debited and Cash is credited, but no reductions are made to Merchandise Inventory.

For example, suppose a kitchen appliances retailer purchases merchandise for their store from a manufacturer on September 1 in the amount of $1,600. Credit terms are 2/10, n/30 from the invoice date of September 1. The retailer makes payment on September 5 and receives the discount. The following entry occurs.

Let’s consider the same situation except the retailer did not make the discount window and paid in full on September 30. The entry would recognize the following instead.

There are two kinds of purchase discounts, cash discounts and trade discounts. Cash discount provides a discount on the final price after purchase if a retailer pays within a discount window. On the other hand, a trade discount is a reduction to the advertised manufacturer’s price that occurs during negotiations of a final purchase price before the inventory is purchased. The trade discount may become larger if the retailer purchases more in one transaction. While the cash discount is recognized in journal entries, a trade discount is not, since it is negotiated before purchase.

For example, assume that a retailer is considering an order for $4,000 in inventory on September 1. The manufacturer offers the retailer a 15% discount on the price if they place the order by September 5. Assume that the retailer places the $4,000 order on September 3. The purchase price would be $4,000 less the 15% discount of $600, or $3,400. Since the trade discount is based on when the order was placed and not on any potential payment discounts, the initial journal entry to record the purchase would reflect the discounted amount of $3,400. Even if the retailer receives a trade discount, they may still be eligible for an additional purchase discount if they pay within the discount window of the invoice.

Purchase Returns and Allowances

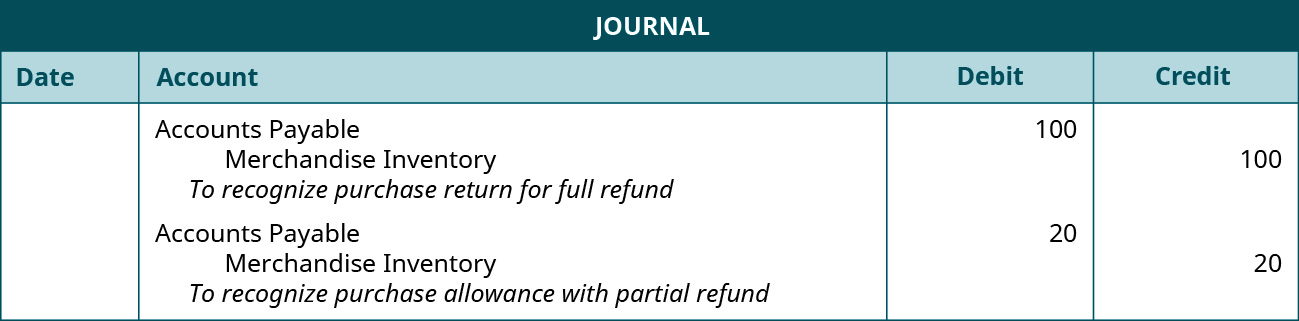

If a retailer is unhappy with their purchase—for example, if the order is incorrect or if the products are damaged—they may receive a partial or full refund from the manufacturer in a purchase returns and allowances transaction. A purchase return occurs when merchandise is returned and a full refund is issued. A purchase allowance occurs when merchandise is kept and a partial refund is issued. In either case, a manufacturer will issue a debit memo to acknowledge the change in contract terms and the reduction in the amount owed.

To recognize a return or allowance, the retailer will reduce Accounts Payable (or increase Cash) and reduce Merchandise Inventory. Accounts Payable decreases if the retailer has yet to pay on their account, and Cash increases if they had already paid and received a subsequent refund. Merchandise Inventory decreases to show the reduction of inventory cost from the retailer’s inventory stock. Note that if a retailer receives a refund before they make a payment, any discount taken must be from the new cost of the merchandise less the refund.

To illustrate, assume that Carter Candle Company received a shipment from a manufacturer that had 150 candles that cost $150. Assume that they have not yet paid for these candles and 100 of the candles are badly damaged and must be returned. The other 50 candles are marketable, but are not the right style. The candle company returned the 100 defective candles for a full refund and requested and received an allowance of $20 for the 50 improper candles they kept. The first entry shows the return and the second entry shows the allowance.

It is possible to show these entries as one, since they affect the same accounts and were requested at the same time. From a manager’s standpoint, though, it may be better to record these as separate transactions to better understand the specific reasons for the reduction to inventory (either return or allowance) and restocking needs.

Characteristics of Sales Transactions

Business owners may encounter several sales situations that can help meet customer needs and control inventory operations. For example, some customers will expect the opportunity to buy using short-term credit and often will assume that they will receive a discount for paying within a brief period. The mechanics of sales discounts are demonstrated later in this section.

Sales with Cash or on Credit

As previously mentioned, a sale is usually considered a transaction between a merchandiser or retailer and a customer. When a sale occurs, a customer has the option to pay with cash or credit. For our purposes, let’s consider “credit” as credit extended from the business directly to the customer.

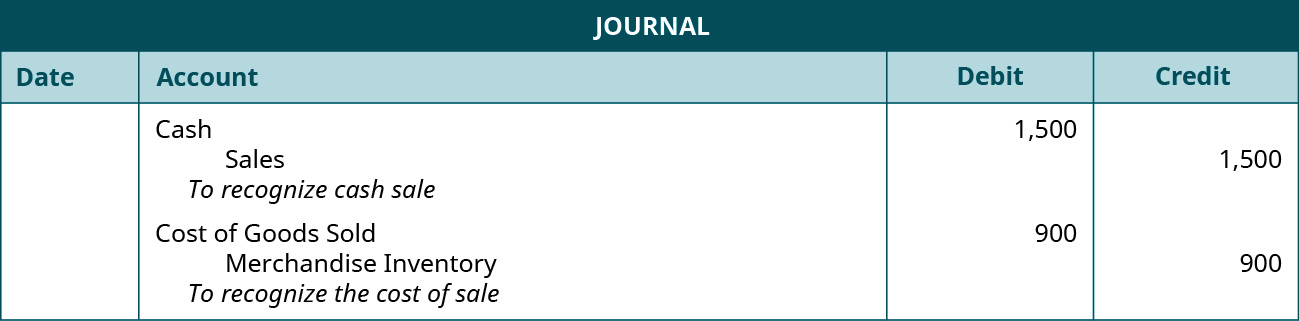

Whether or not a customer pays with cash or credit, a business must record two accounting entries. One entry recognizes the sale and the other recognizes the cost of the sale. The sales entry consists of a debit to either Cash or Accounts Receivable (if paying on credit), and a credit to the revenue account, Sales.

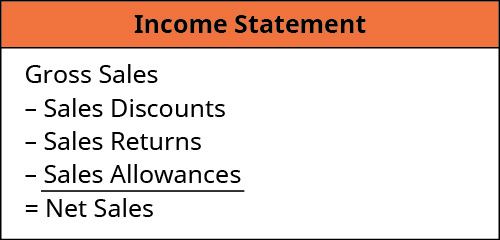

The amount recorded in the Sales account is the gross amount. Gross sales is the original amount of the sale without factoring in any possible reductions for discounts, returns, or allowances. Once those reductions are recorded at the end of a period, net sales are calculated. Net sales (see Figure 2.12) equals gross sales less sales discounts, sales returns, and sales allowances. Recording the sale as it occurs allows the company to align with the revenue recognition principle. The revenue recognition principle requires companies to record revenue when it is earned, and revenue is earned when a product or service has been provided.

The second accounting entry that is made during a sale describes the cost of sales. The cost of sales entry includes decreasing Merchandise Inventory and increasing Cost of Goods Sold (COGS). The decrease to Merchandise Inventory reflects the reduction in the inventory account value due to the sold merchandise. The increase to COGS represents the expense associated with the sale. The cost of goods sold (COGS) is an expense account that houses all costs associated with getting the product ready for sale. This could include purchase costs, shipping, taxes, insurance, stocking fees, and overhead related to preparing the product for sale. By recording the cost of sale when the sale occurs, the company aligns with the matching principle. The matching principle requires companies to match revenues generated with related expenses in the period in which they are incurred.

For example, when a shoe store sells 150 pairs of athletic cleats to a local baseball league for $1,500 (cost of $900), the league may pay with cash or credit. If the baseball league elects to pay with cash, the shoe store would debit Cash as part of the sales entry. If the baseball league decides to use a line of credit extended by the shoe store, the shoe store would debit Accounts Receivable as part of the sales entry instead of Cash. With the sales entry, the shoe store must also recognize the $900 cost of the shoes sold and the $900 reduction in Merchandise Inventory.

You may have noticed that sales tax has not been discussed as part of the sales entry. Sales taxes are liabilities that require a portion of every sales dollar be remitted to a government entity. This would reduce the amount of cash the company keeps after the sale. Sales tax is relevant to consumer sales and is discussed later in the course.

There are a few transactional situations that may occur after a sale is made that have an effect on reported sales at the end of a period.

Sales Discounts

Sales discounts are incentives given to customers to entice them to pay off their accounts early. Why would a retailer offer this? Wouldn’t they rather receive the entire amount owed? The discount serves several purposes that are similar to the rationale manufacturers consider when offering discounts to retailers. It can help solidify a long-term relationship with the customer, encourage the customer to purchase more, and decreases the time it takes for the company to see a liquid asset (cash). Cash can be used for other purposes immediately such as reinvesting in the business, paying down loans quicker, and distributing dividends to shareholders. This can help grow the business at a more rapid rate.

Similar to credit terms between a retailer and a manufacturer, a customer could see credit terms offered by the retailer in the form of 2/10, n/30. This particular example shows that if a customer pays their account within 10 days, they will receive a 2% discount. Otherwise, they have 30 days to pay in full but do not receive a discount. If the customer does not pay within the discount window, but pays within 30 days, the retailing company records a credit to Accounts Receivable, and a debit to Cash for the full amount stated on the invoice. If the customer is able to pay the account within the discount window, the company records a credit to Accounts Receivable, a debit to Cash, and a debit to Sales Discounts.

The sales discounts account is a contra revenue account that is deducted from gross sales at the end of a period in the calculation of net sales. Sales Discounts has a normal debit balance, which offsets Sales that has a normal credit balance.

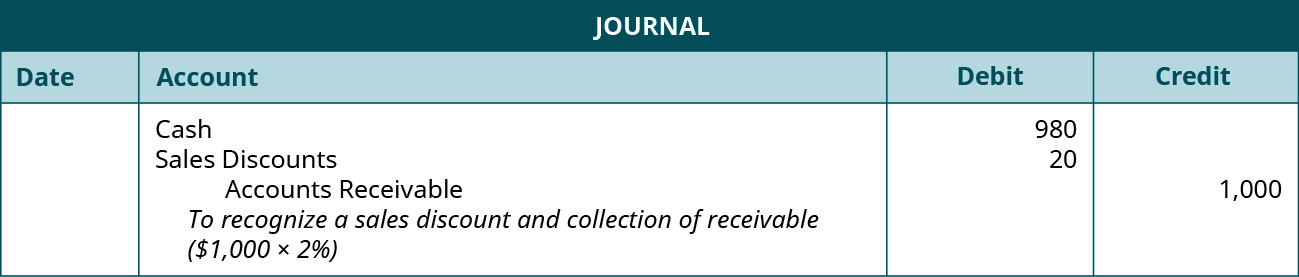

Let’s assume that a customer purchased 10 emergency kits from a retailer at $100 per kit on credit. The retailer offered the customer 2/10, n/30 terms, and the customer paid within the discount window. The retailer recorded the following entry for the initial sale.

Since the retailer doesn’t know at the point of sale whether or not the customer will qualify for the sales discount, the entire account receivable of $1,000 is recorded on the retailer’s journal.

Also assume that the retailer’s costs of goods sold in this example were $560 and we are using the perpetual inventory method. The journal entry to record the sale of the inventory follows the entry for the sale to the customer.

Since the customer paid the account in full within the discount qualification period of ten days, the following journal entry on the retailer’s books reflects the payment.

Now, assume that the customer paid the retailer within the 30-day period but did not qualify for the discount. The following entry reflects the payment without the discount.

Please note that the entire $1,000 account receivable created is eliminated under both payment options. When the discount is missed, the retail received the entire $1,000. However, when the discount was received by the customer, the retailer received $980, and the remaining $20 is recorded in the sales discount account.

Sales Returns and Allowances

If a customer purchases merchandise and is dissatisfied with their purchase, they may receive a refund or a partial refund, depending on the situation. When the customer returns merchandise and receives a full refund, it is considered a sales return. When the customer keeps the defective merchandise and is given a partial refund, it is considered a sales allowance. The biggest difference is that a customer returns merchandise in a sales return and keeps the merchandise in a sales allowance.

When a customer returns the merchandise, a retailer issues a credit memo to acknowledge the change in contract and reduction to Accounts Receivable, if applicable. The retailer records an entry acknowledging the return by reducing either Cash or Accounts Receivable and increasing Sales Returns and Allowances. Cash would decrease if the customer had already paid for the merchandise and cash was thus refunded to the customer. Accounts Receivable would decrease if the customer had not yet paid on their account. Like Sales Discounts, the sales returns and allowances account is a contra revenue account with a normal debit balance that reduces the gross sales figure at the end of the period.

Beyond recording the return, the retailer must also determine if the returned merchandise is in “sellable condition.” An item is in sellable condition if the merchandise is good enough to warrant a sale to another customer in the future. If so, the company would record a decrease to Cost of Goods Sold (COGS) and an increase to Merchandise Inventory to return the merchandise back to the inventory for resale. This is recorded at the merchandise’s costs of goods sold value. If the merchandise is in sellable condition but will not realize the original cost of the good, the company must estimate the loss at this time.

On the other hand, when the merchandise is returned and is not in sellable condition, the retailer must estimate the value of the merchandise in its current condition and record a loss. This would increase Merchandise Inventory for the assessed value of the merchandise in its current state, decrease COGS for the original expense amount associated with the sale, and increase Loss on Defective Merchandise for the unsellable merchandise lost value.

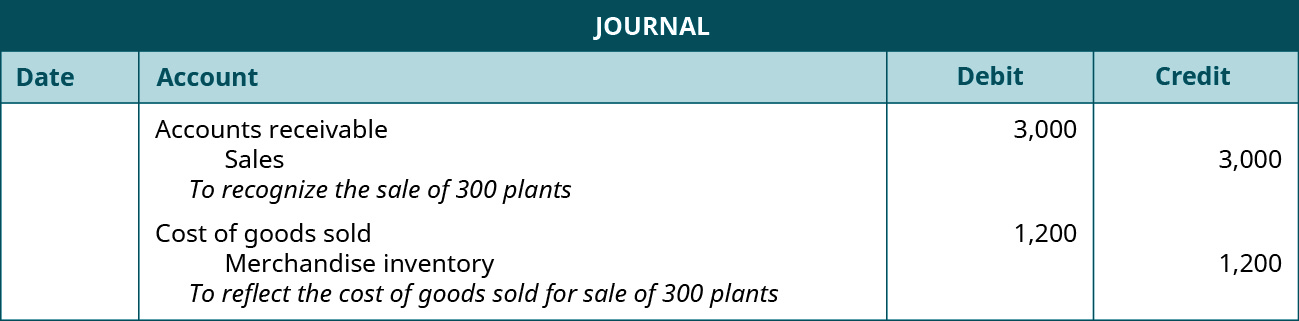

Let’s say a customer purchases 300 plants on credit from a nursery for $3,000 (with a cost of $1,200). The first entry reflects the initial sale by the nursery. The second entry reflects the cost of goods sold.

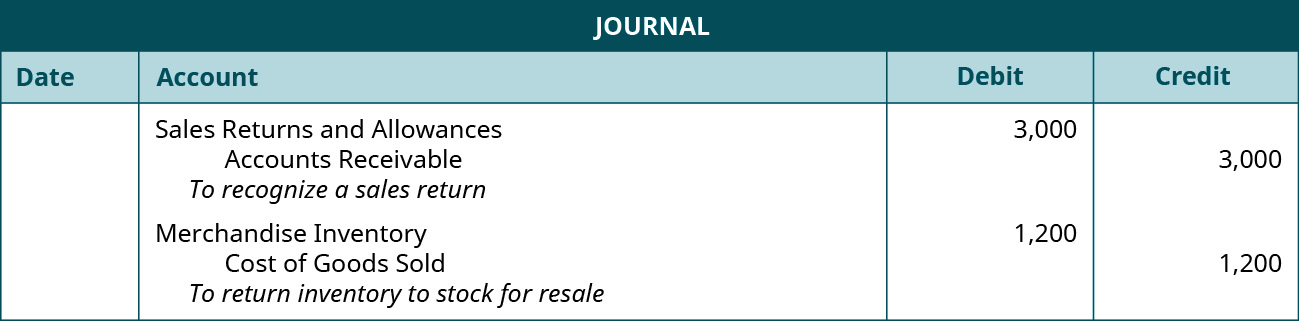

Upon receipt, the customer discovers the plants have been infested with bugs and they send all the plants back. Assuming that the customer had not yet paid the nursery any of the $3,000 accounts receivable and assuming that the nursery determines the condition of the returned plants to be sellable, the retailer would record the following entries.

For another example, let’s say the plant customer was only dissatisfied with 100 of the plants. After speaking with the nursery, the customer decides to keep 200 of the plants for a partial refund of $1,000. The nursery would record the following entry for sales allowance associated with 100 plants.

The nursery would also record a corresponding entry for the inventory and the cost of goods sold for the 100 returned plants.

For both the return and the allowance, if the customer had already paid their account in full, Cash would be affected rather than Accounts Receivable.

There are differing opinions as to whether sales returns and allowances should be in separate accounts. Separating the accounts would help a retailer distinguish between items that are returned and those that the customer kept. This can better identify quality control issues, track whether a customer was satisfied with their purchase, and report how many resources are spent on processing returns. Most companies choose to combine returns and allowances into one account, but from a manager’s perspective, it may be easier to have the accounts separated to make current determinations about inventory.

You may have noticed our discussion of credit sales did not include third-party credit card transactions. This is when a customer pays with a credit or debit card from a third-party, such as Visa, MasterCard, Discover, or American Express. These entries and discussion are covered in more advanced accounting courses.

Media Attributions

- Operating Cycle for a Service Firm © Rice University is licensed under a CC BY-NC-SA (Attribution NonCommercial ShareAlike) license