8.9 Process Costing Overview

Process costing is the optimal costing system when a standardized process is used to manufacture identical products and the direct material, direct labor, and manufacturing overhead cannot be easily or economically traced to a specific unit. Process costing is used most often when manufacturing a product in batches. Each department or production process or batch process tracks its direct material and direct labor costs as well as the number of units in production. The actual cost to produce each unit through a process costing system varies, but the average result is an adequate determination of the cost for each manufactured unit. Examples of items produced and accounted for using a form of the process costing method could be soft drinks, petroleum products, or even furniture such as chairs, assuming that the company makes batches of the same chair, instead of customizing final products for individual customers.

For example, small companies, such as David and William’s, and large companies, such as Nabisco, use similar cost-determination processes. In order to understand how much each product costs—for example, Oreo cookies—Nabisco uses process costing to track the direct materials, direct labor, and manufacturing overhead used in the manufacturing of its products. Oreo production has six distinct steps or departments: (1) make the cookie dough, (2) press the cookie dough into a molding machine, (3) bake the cookies, (4) make the filling and apply it to the cookies, (5) put the cookies together into a sandwich, and (6) and place the cookies into plastic trays and packages. Each department keeps track of its direct materials used and direct labor incurred, and manufacturing overhead applied to facilitate determining the cost of a batch of Oreo cookies.

As previously mentioned, process costing is used when similar items are produced in large quantities. As such, many individuals immediately associate process costing with assembly line production. Process costing works best when products cannot be distinguished from each other and, in addition to obvious production line products like ice cream or paint, also works for more complex manufacturing of similar products like small engines. Conversely, products in a job order cost system are manufactured in small quantities and include custom jobs such as custom manufacturing products. They can also be legal or accounting tasks, movie production, or major projects such as construction activities.

The difference between process costing and job order costing relates to how the costs are assigned to the products. In either costing system, the ability to obtain and analyze cost data is needed. This results in the costing system selected being the one that best matches the manufacturing process.

A job order cost system is often more expensive to maintain than a basic process costing system, since there is a cost associated with assigning the individual material and labor to the product. Thus, a job order cost system is used for custom jobs when it is easy to determine the cost of materials and labor used for each job. A process cost system is often less expensive to maintain and works best when items are identical and it is difficult to trace the exact cost of materials and labor to the final product. For example, assume that your company uses three production processes to make jigsaw puzzles. The first process glues the picture on the cardboard backing, the second process cuts the puzzle into pieces, and the final process loads the pieces into the boxes and seals them. Tracing the complete costs for the batch of similar puzzles would likely entail three steps, with three separate costing system components. In this environment, it would be difficult and not economically feasible to trace the exact materials and the exact labor to each individual puzzle; rather, it would be more efficient to trace the costs per batch of puzzles.

The costing system used typically depends on whether the company can most efficiently and economically trace the costs to the job (favoring job order costing system) or to the production department or batch (favoring a process costing system).

While the costing systems are different from each other, management uses the information provided to make similar managerial decisions, such as setting the sales price. For example, in a job order cost system, each job is unique, which allows management to establish individual prices for individual projects. Management also needs to establish a sales price for a product produced with a process costing system, but this system is not designed to stop the production process and individually cost each batch of a product, so management must set a price that will work for many batches of the product.

In addition to setting the sales price, managers need to know the cost of their products in order to determine the value of inventory, plan production, determine labor needs, and make long- and short-term plans. They also need to know the costs to determine when a new product should be added or an old product removed from production.

In this chapter, you will learn when and why process costing is used. You’ll also learn the concepts of conversion costs and equivalent units of production and how to use these for calculating the unit and total cost of items produced using a process costing system.

Basic Managerial Accounting Terms Used in Job Order Costing and Process Costing

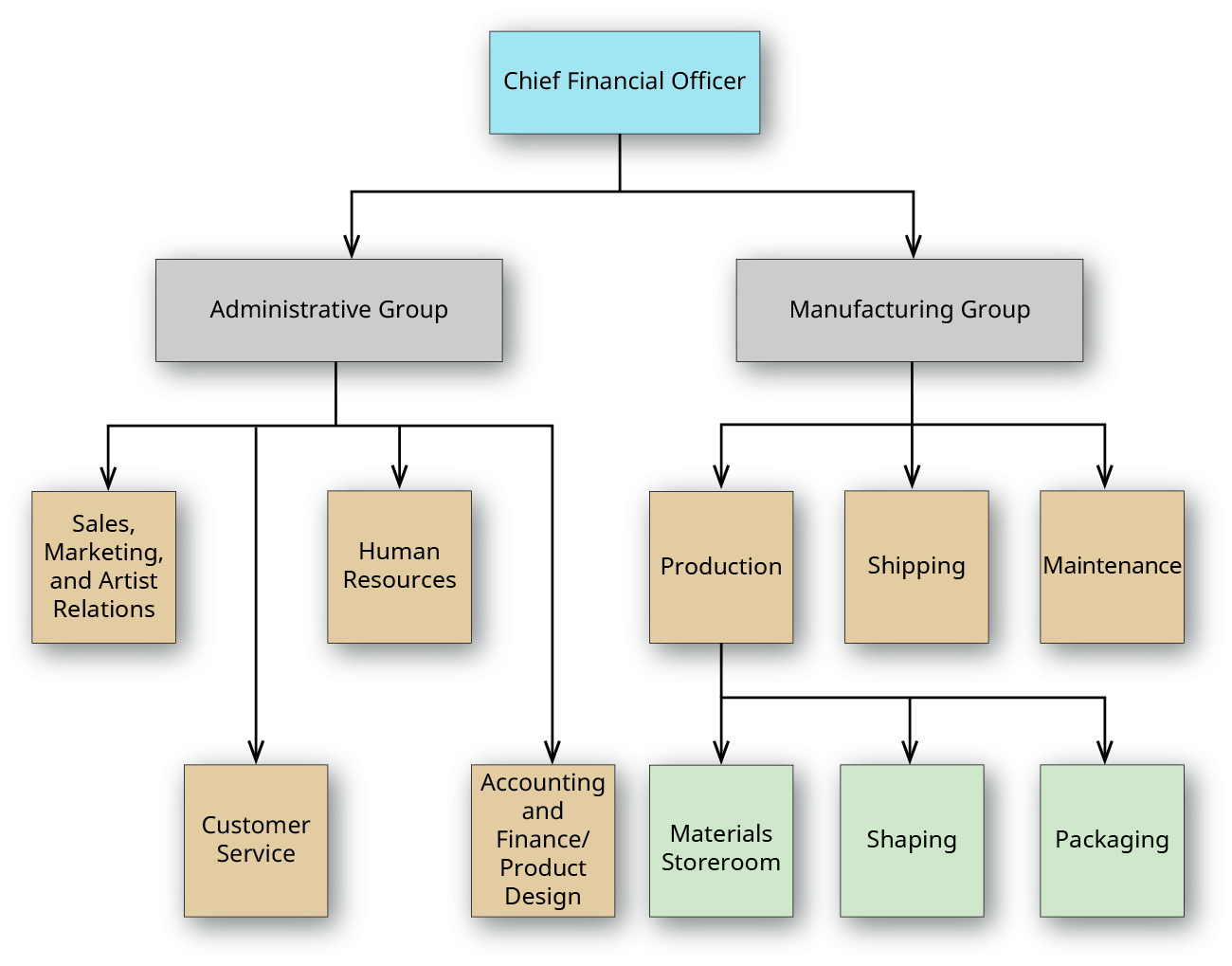

Regardless of the costing system used, manufacturing costs consist of direct material, direct labor, and manufacturing overhead. Figure 8.61 shows a partial organizational chart for Rock City Percussion, a drumstick manufacturer. In this example, two groups—administrative and manufacturing—report directly to the chief financial officer (CFO). Each group has a vice president responsible for several departments. The organizational chart also shows the departments that report to the production department, illustrating the production arrangement. The material storage unit stores the types of wood used (hickory, maple, and birch), the tips (nylon and felt), and packaging materials.

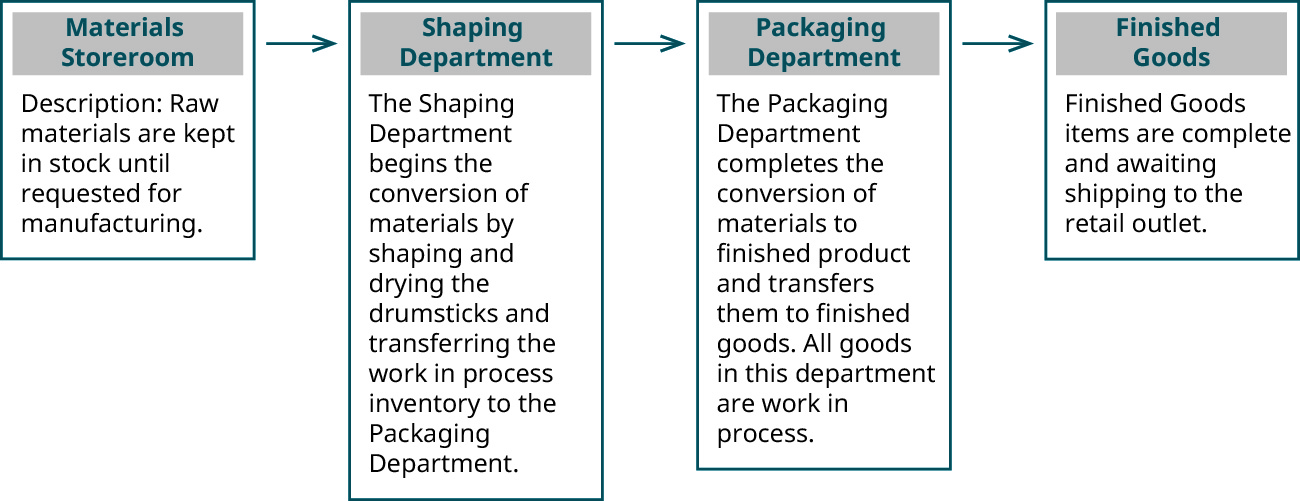

Understanding the company’s organization is an important first step in any costing system. Next is understanding the production process. The most basic drumstick is made of hickory and has a wooden tip. When the popular size 5A stick is manufactured, the hickory stored in the materials storeroom is delivered to the shaping department where the wood is cut into pieces, shaped into dowels, and shaped into the size 5A shape while under a stream of water. The sticks are dried, and then sent to the packaging department, where the sticks are embossed with the Rock City Percussion logo, inspected, paired, packaged, and shipped to retail outlets such as Guitar Center. The manufacturing process is described in Figure 8.62.

The different units within Rock City Percussion illustrate the two main cost categories of a manufacturing company: manufacturing costs and administrative costs.

Manufacturing Costs

Manufacturing costs or product costs include all expenses required to manufacture the product: direct materials, direct labor, and manufacturing overhead. Since process costing assigns the costs to each department, the inventory at the end of the period includes the finished goods inventory, and the work in process inventory for each manufacturing department. For example, using the departments shown in Figure 8.62, raw materials inventory is the cost paid for the materials that remain in the storeroom until requested.

While still in production, the work in process units are moved from one department to the next until they are completed, so the work in process inventory includes all of the units in the shaping and packaging departments. When the units are completed, they are transferred to finished goods inventory and become costs of goods sold when the product is sold.

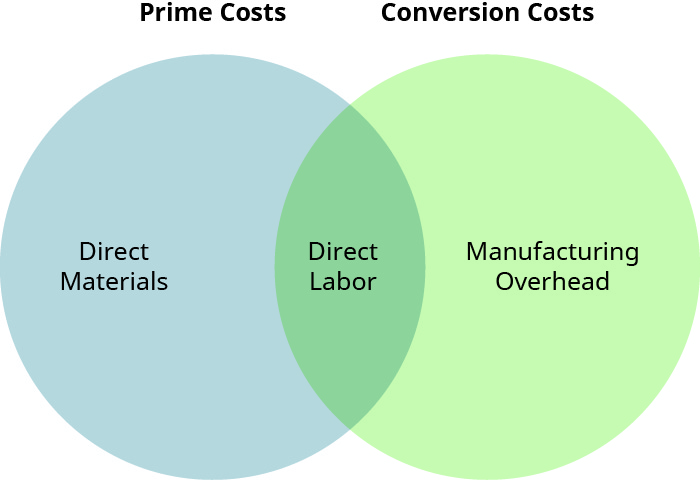

When assigning costs to departments, it is important to separate the product costs from the period costs, which are those that are typically related with a particular time period, instead of attached to the production of an asset. Management often needs additional information to make decisions and needs the product costs further categorized as prime costs or conversion costs (Figure 8.63). Prime costs are costs that include the primary (or direct) product costs: direct material and direct labor. Conversion costs are the costs necessary to convert direct materials into a finished product: direct labor and manufacturing overhead, which includes other costs that are not classified as direct materials or direct labor, such as plant insurance, utilities, or property taxes. Also, note that direct labor is considered to be a component of both prime costs and conversion costs.

Job order costing tracks prime costs to assign direct material and direct labor to individual products (jobs). Process costing also tracks prime costs to assign direct material and direct labor to each production department (batch). Manufacturing overhead is another cost of production, and it is applied to products (job order) or departments (process) based on an appropriate activity base.

Selling and Administrative Expenses

Selling and administrative (S&A) expenses are period costs, which means that they are recorded in the period in which they were incurred. Selling and administrative expenses typically are not directly assigned to the items produced or services provided and include costs of departments not directly associated with manufacturing but necessary to operate the business. The selling costs component of S&A expenses is related to the promotion and sale of the company’s products, while administrative expenses are related to the administration of the company. Some examples of S&A expenses include marketing costs; administration building rent; the chief executive officer’s salary expense; and the accounting, payroll, and data processing department expenses.

These general rules for S&A expenses, however, have their exceptions. For example, some items that are classified as overhead, such as plant insurance, are period costs but are classified as overhead and are attached to the items produced as product costs.

The expense recognition principle is the primary reason to separate the costs of production from the other expenses of the company. This principle requires costs to be recorded in the period in which they are incurred. The costs are expensed when matched to the revenue with which they are associated; this is commonly referred to as having the expenses follow the revenues.

Period costs are expensed during the period in which they are incurred; this allows a company to apply the administrative and other expenses shown on the income statement to the same period in which the company earns income. Under generally accepted accounting principles (GAAP), separating the production costs and assigning them to the department results in the costs of the product staying with the work in process inventory for each department. This follows the expense recognition principle because the cost of the product is expensed when revenue from the sale is recognized.

Equivalent Units

In a process cost system, costs are maintained by each department, and the method for determining the cost per individual unit is different than in a job order costing system. Rock City Percussion uses a process cost system because the drumsticks are produced in batches, and it is not economically feasible to trace the direct labor or direct material, like hickory, to a specific drumstick. Therefore, the costs are maintained by each department, rather than by job, as they are in job order costing.

How does an organization determine the cost of each unit in a process costing environment? The costs in each department are allocated to the number of units produced in a given period. This requires determination of the number of units produced, but this is not always an easy process. At the end of the accounting period, there typically are always units still in production, and these units are only partially complete. Think of it this way: At midnight on the last day of the month, all accounting numbers need to be determined in order to process the financial statements for that month, but the production process does not stop at the end of each accounting period. However, the number of units produced must be calculated at the end of the accounting period to determine the number of equivalent units, or the number of units that would have been produced if the units were produced sequentially and in their entirety in a particular time period. The number of equivalent units is different from the number of actual units and represents the number of full or whole units that could have been produced given the amount of effort applied. To illustrate, consider this analogy. You have five large pizzas that each contained eight slices. Your friends served themselves, and when they were finished eating, there were several partial pizzas left. In equivalent units, determine how many whole pizzas are left if the remaining slices are divided as shown in Figure 8.64

- Pie 1 had one slice

- Pie 2 had two slices

- Pie 3 had two slices

- Pie 4 had three slices

- Pie 5 had eight slices

Together, there are sixteen slices left. Since there are eight slices per pizza, the leftover pizza would be considered two full equivalent units of pizzas. The equivalent unit is determined separately for direct materials and for conversion costs as part of the computation of the per-unit cost for both material and conversion costs.

Major Characteristics of Process Costing

Process costing is the optimal system for a company to use when the production process results in many similar units. It is used when production is continuous or occurs in large batches and it is difficult to trace a particular input cost to a specific individual product.

For example, before David and William found ways to make five large cookies per batch, their family always made one large cookie per batch. In order to make five cookies at a time, they had to gather the ingredients and baking materials, including five bowls and five cookie sheets. The exact amount of ingredients for one large cookie was mixed in each separate bowl and then placed on the cookie sheet. When this method was used, it was easy to establish that exactly one egg, two cups of flour, three-quarter cup of chocolate chips, three-quarter cup of sugar, one-quarter teaspoon salt, and so forth, were in each cookie. This made it easy to determine the exact cost of each cookie. But if David and William used one bowl instead of five bowls, measured the ingredients into it and then divided the dough into five large cookies, they could not know for certain that each cookie has exactly two cups of flour. One cookie may have 1 and 7 eighths cups and another may have 1 and 15 sixteenths cups, and one cookie may have a few more chocolate chips than another. It is also impossible to trace the chocolate chips from each bag to each cookie because the chips were mixed together. These variations do not affect the taste and are not important in this type of accounting. Process costing is optimal when the products are relatively homogenous or indistinguishable from one another, such as bottles of vegetable oil or boxes of cereal.

Often, process costing makes sense if the individual costs or values of each unit are not significant. For example, it would not be cost effective for a restaurant to make each cup of iced tea separately or to track the direct material and direct labor used to make each eight-ounce glass of iced tea served to a customer. In this scenario, job order costing is a less efficient accounting method because it costs more to track the costs per eight ounces of iced tea than the cost of a batch of tea. Overall, when it is difficult or not economically feasible to track the costs of a product individually, process costing is typically the best cost system to use.

Process costing can also accommodate increasingly complex business scenarios. While making drumsticks may sound simple, an immense amount of technology is involved. Rock City Percussion makes 8,000 hickory sticks per day, four days each week. The sticks made of maple and birch are manufactured on the fifth day of the week. It is difficult to tell the first drumstick made on Monday from the 32,000th one made on Thursday, so a computer matches the sticks in pairs based on the tone produced.

Process costing measures and assigns the costs to the associated department. The basic 5A hickory stick consists only of hickory as direct material. The rest of the manufacturing process involves direct labor and manufacturing overhead, so the focus is on properly assigning those costs. Thus, process costing works well for simple production processes such as cereal, rubber, and steel, and for more complicated production processes such as the manufacturing of electronics and watches, if there is a degree of similarity in the production process.

In a process cost system, each department accumulates its costs to compute the value of work in process inventory, so there will be a work in process inventory for each manufacturing or production department as well as an inventory cost for finished goods inventory. Manufacturing departments are often organized by the various stages of the production process. For example, blending, baking, and packaging could each be categorized as manufacturing or production departments for the cookie producer, while cutting, assembly, and finishing could be manufacturing or production departments with accompanying costs for a furniture manufacturer. Each department, or process, will have its own work in process inventory account, but there will only be one finished goods inventory account.

There are two methods used to compute the values in the work in process and finished goods inventories. The first method is the weighted-average method, which includes all costs (costs incurred during the current period and costs incurred during the prior period and carried over to the current period). This method is often favored, because in the process cost production method there often is little product left at the end of the period and most has been transferred out. The second method is the first-in, first-out (FIFO) method, which calculates the unit costs based on the assumption that the first units sold come from the prior period’s work in process that was carried over into the current period and completed. After these units are sold, the newer completed units can then be sold. The theory is similar to the FIFO inventory valuation process that you learned about in Accounting for Inventory. (Since the FIFO process costing method is more complicated than the weighted-average method, the FIFO method is typically covered in more advanced accounting courses.)

With processing, it is difficult to establish how much of each material, and exactly how much time is in each unit of finished product. This will require the use of the equivalent unit computation, and management selects the method (weighted average or FIFO) that best fits their information system.

Process costing can also be used by service organizations that provide homogeneous services and often do not have inventory to value, such as a hotel reservation system. Although they have no inventory, the hotel might want to know its costs per reservation for a period. They could allocate the total costs incurred by the reservation system based on the number of inquiries they served. For example, assume that in a year they incurred costs of $200,000 and served 50,000 potential guests. They could determine an average cost by dividing costs by number of inquiries, or $200,000 ÷ 50,000 = $4.00 per potential guest.

In the case of a not-for-profit company, the same process could be used to determine the average costs incurred by a department that performs interviews. The department’s costs would be allocated based on the number of cases processed. For example, assume a not-for-profit pet adoption organization has an annual budget of $180,000 and typically matches 900 shelter animals with new owners each year. The average cost would be $200 per match.

Similarities between Process Costing and Job Order Costing

Both process costing and job order costing maintain the costs of direct material, direct labor, and manufacturing overhead. The process of production does not change because of the costing method. The costing method is chosen based on the production process.

In job order cost production, the costs can be directly traced to the job, and the job cost sheet contains the total expenses for that job. Process costing is optimal when the costs cannot be traced directly to the job. For example, it would be impossible for David and William to trace the exact amount of eggs in each chocolate chip cookie. It is also impossible to trace the exact amount of hickory in a drumstick. Even two sticks made sequentially may have different weights because the wood varies in density. These types of manufacturing are optimal for the process cost system.

The similarities between job order cost systems and process cost systems are the product costs of materials, labor, and overhead, which are used determine the cost per unit, and the inventory values. The differences between the two systems are shown in Table 8.3.

| Job Order Costing | Process Costing |

|---|---|

| Product costs are traced to the product and recorded on each job’s individual job cost sheet. | Product costs are traced to departments or processes. |

| Each department tracks its expenses and adds them to the job cost sheet. As jobs move from one department to another, the job cost sheet moves to the next department as well. | Each department tracks its expenses, the number of units started or transferred in, and the number of units transferred to the next department. |

| Unit costs are computed using the job cost sheet. | Unit costs are computed using the departmental costs and the equivalent units produced. |

| Finished goods inventory includes the products completed but not sold, and all incomplete jobs are work in process inventory. | Finished goods inventory is the number of units completed at the per unit cost. Work in process inventory is the cost per unit and the equivalent units remaining to be completed. |

CONCEPTS IN PRACTICE

Choosing Between Process Costing and Job Order Costing

Process costing and job order costing are both acceptable methods for tracking costs and production levels. Some companies use a single method, while some companies use both, which creates a hybrid costing system. The system a company uses depends on the nature of the product the company manufactures.

Companies that mass produce a product allocate the costs to each department and use process costing. For example, General Mills uses process costing for its cereal, pasta, baking products, and pet foods. Job order systems are custom orders because the cost of the direct material and direct labor are traced directly to the job being produced. For example, Boeing uses job order costing to manufacture planes.

When a company mass produces parts but allows customization on the final product, both systems are used; this is common in auto manufacturing. Each part of the vehicle is mass produced, and its cost is calculated with process costing. However, specific cars have custom options, so each individual car costs the sum of the specific parts used.

Long Descriptions

Box labeled Chief Financial Officer at the top points to two boxes just below labeled Administrative Group and Manufacturing Group. The Administrative Group box points to four boxes below that: Sales, Marketing, and Artist Relations; Customer Service; Human Resources; and Accounting and Finance/Product Design. The Manufacturing Group box points to three boxes below it: Production, Shipping, and Maintenance. The Production box points to three boxes below it: Materials Storeroom, Shaping, and Packaging. Return

Four boxes with arrows pointing from left to right. Leftmost box is Materials Storeroom. Description: Raw materials are kept in stock until requested for manufacturing. The next box is Shaping and Drying. The Shaping Department begins the conversion of materials by shaping the drumsticks and transferring the work in process inventory to the Packaging Department. The next box is the Packaging Department. The Packaging Department completes the conversion of materials to finished product and transfers them to finished goods. All goods in this department are work in process. The last box is Finished Goods. Finished Goods items are complete and awaiting shipping to the retail outlet. Return

A diagram showing five boxes with pizzas labeled 1 through 5. The first has seven grayed-out slices and one orange slice. The second and third have six grayed-out and two orange slices each. The fourth has five grayed-out and three orange, the fifth has eight orange slices. There are two more boxes filled with the orange slices, labeled Equivalent Units—one has the collection of the eight oranges slices collected from boxes 1 through 4, the other is the full box 5 repeated. Return