8.8 Job Order in the Service Industries

Fundamentals of the Job Order Costing Method for Service Entities

Instead of being dependent on materials, service industries depend on labor. Since their work is labor intensive, it makes sense to use labor as an activity base with billable hours often as the best allocation base. For example, in an audit, there often will be several accountants, with differing levels of experience and expertise involved in the assignment. The accounting firms have more billable hours at the staff level and fewer billable hours at the partner level. And since the firm bills the partner’s time at a significantly higher rate than the staff, it makes sense to apply overhead at the billable hours instead of the billable costs.

In service industries, there is no manufacturing overhead because they are not manufacturing a product, but instead are providing a service. Accordingly, overhead is called operating overhead.

Another terminology difference is the inventory accounts. The jobs are considered movies or assignments in process, and are transferred to a cost of service sold account instead of to a finished goods inventory.

CONCEPTS IN PRACTICE

Tracking Costs in Healthcare

Healthcare is one of the industries that keeps track of materials, such as medicine. In this industry, direct labor is shown to the patient as the cost of the provider, such as a physician, physician assistant, or nurse practitioner. Indirect labor includes all other personnel from front desk staff to the nurse who gathers vital signs or a technician who performs tests. Patients do not see the overhead cost on their bill, but it is built into the invoice as part of the practitioner or testing fees.

Service Entity Use of a Job Order Costing System

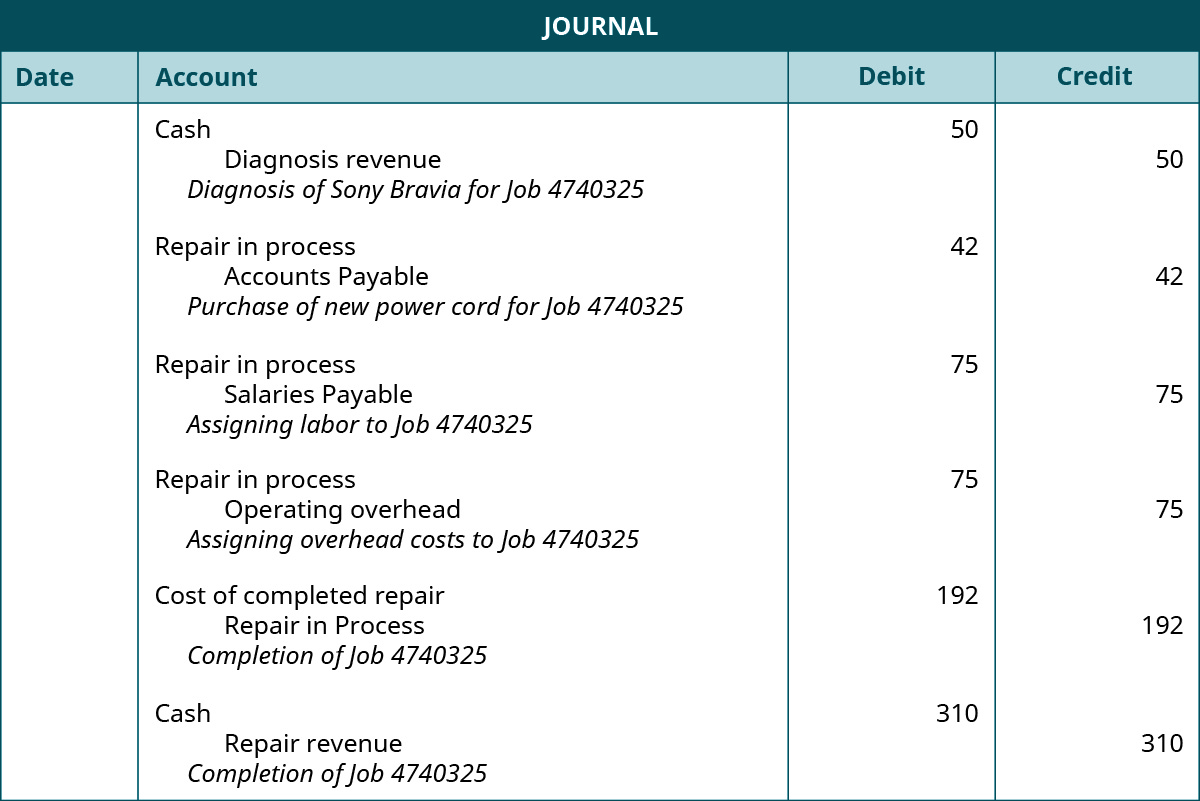

To understand how a service provider uses a job order cost system, let’s consider the case of IFixIT. IFixIT Systems is a Sony-authorized repair provider that fixes audiovisual equipment brought in by customers. IFixIT requires customers to pay $50 to diagnose the problem. IFixIt pays its employees $25 per hour and assigns overhead equal to its direct labor cost. The customers’ bills do not show overhead and are instead itemized as parts plus labor, where the cost for parts is the original cost plus a markup, and the labor rate is $80 per hour.

A customer brought in his TV and paid the $50 diagnostic fee. IFixIT determined a new power cord was needed. To fix it, IFixIT purchases the part from its suppliers at $42 and pays $75 in direct labor for 3 hours at $25 per hour. Overhead is applied equal to the direct labor cost of $75. The customer is charged $310, consisting of $70 for the part and 3 hours of labor at a rate of $80 per hour. IFixIT records the journal entries shown:

Long Description

A journal with four columns headed “Date”, “Account”, “Debit”, and “Credit.” There are six entries (not dated.) The first one shows in the “Account” column a debit to “Cash, a credit (indented) to Diagnosis revenue, and the entry description, which reads “Diagnosis of Sony Bravia for Job 4740325”. The amount of 50 is listed in the debit column across from the “Cash” debit and in the credit column across from the “Diagnosis Revenue” credit. The second entry shows in the “Account” column a debit to “Repair in process”, a credit (indented) to “Accounts Payable”, and the entry description, which reads “Purchase of new power cord for Job 4740325.” The amount of 42 is shown across from each of these in the respective debit and credit columns. The third entry shows in the “Account” column a debit to “Repair in process”, a credit (indented) to “Salaries Expense”, and the entry description, which reads “Assigning labor to Job 4740325.” The amount of 75 is shown across from each of these in the respective debit and credit columns. The fourth entry shows in the “Account” column a debit to “Repair in process”, a credit (indented) to “Operating Overhead”, and the entry description, which reads “Assigning overhead costs to Job 4740325.” The amount of 75 is shown across from each of these in the respective debit and credit columns. The fifth entry shows in the “Account” column a debit to “Cost of completed repair”, a credit (indented) to “Repair in process”, and the entry description, which reads “Completion of Job 4740325.” The amount of 192 is shown across from each of these in the respective debit and credit columns. The sixth entry shows in the “Account” column a debit to “Cash” , a credit (indented) to “Repair Service”, and the entry description, which reads “Completion of Job 4740325.” The amount of 310 is shown across from each of these in the respective debit and credit columns. Return