5.1 Current Liabilities

To assist in understanding current liabilities, assume that you own a landscaping company that provides landscaping maintenance services to clients. As is common for landscaping companies in your area, you require clients to pay an initial deposit of 25% for services before you begin working on their property. Asking a customer to pay for services before you have provided them creates a current liability transaction for your business. As you’ve learned, liabilities require a future disbursement of assets or services resulting from a prior business activity or transaction. For companies to make more informed decisions, liabilities need to be classified into two specific categories: current liabilities and noncurrent (or long-term) liabilities. The differentiating factor between current and long-term is when the liability is due.

Fundamentals of Current Liabilities

A current liability is a debt or obligation due within a company’s standard operating period, typically a year, although there are exceptions that are longer or shorter than a year. A company’s typical operating period (sometimes called an operating cycle) is a year, which is used to delineate current and noncurrent liabilities, and current liabilities are considered short term and are typically due within a year or less.

Noncurrent liabilities are long-term obligations with payment typically due in a subsequent operating period. Current liabilities are reported on the classified balance sheet, listed before noncurrent liabilities. Changes in current liabilities from the beginning of an accounting period to the end are reported on the statement of cash flows as part of the cash flows from operations section. An increase in current liabilities over a period increases cash flow, while a decrease in current liabilities decreases cash flow.

| Current Liabilities | Noncurrent Liabilities |

|---|---|

| Due within one year or less for a typical one-year operating period | Due in more than one year or longer than one operating period |

|

Short-term accounts such as:

|

Long-term portion of obligations such as:

|

Examples of Current Liabilities

Common current liabilities include accounts payable, unearned revenues, the current portion of a note payable, and taxes payable. Each of these liabilities is current because it results from a past business activity, with a disbursement or payment due within a period of less than a year.

Accounts Payable

Accounts payable accounts for financial obligations owed to suppliers after purchasing products or services on credit. This account may be an open credit line between the supplier and the company. An open credit line is a borrowing agreement for an amount of money, supplies, or inventory. The option to borrow from the lender can be exercised at any time within the agreed time period.

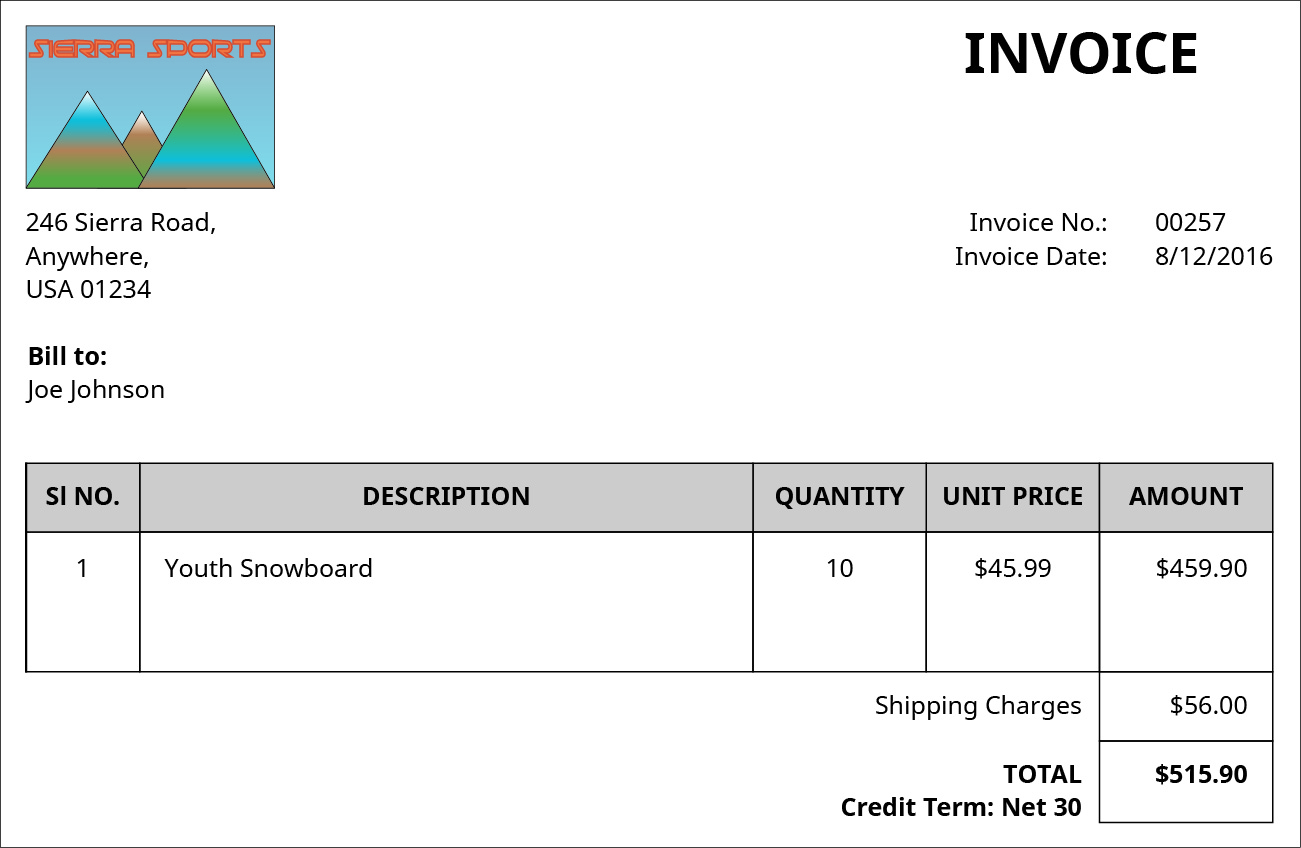

An account payable is usually a less formal arrangement than a promissory note for a current note payable. Long-term debt is covered in depth in An invoice from the supplier (such as the one shown in Figure 5.1) detailing the purchase, credit terms, invoice date, and shipping arrangements will suffice for this contractual relationship. In many cases, accounts payable agreements do not include interest payments, unlike notes payable. Long-Term Liabilities. For now, know that for some debt, including short-term or current, a formal contract might be created. This contract provides additional legal protection for the lender in the event of failure by the borrower to make timely payments. Also, the contract often provides an opportunity for the lender to actually sell the rights in the contract to another party.

For example, assume the owner of a clothing boutique purchases hangers from a manufacturer on credit. The organizations may establish an ongoing purchase agreement, which includes purchase details (such as hanger prices and quantities), credit terms (2/10, n/60), an invoice date, and shipping charges (free on board [FOB] shipping) for each order.

On August 1, Sierra Sports purchases $12,000 of soccer equipment from a manufacturer (supplier) on credit. Assume for the following examples that Sierra Sports uses the perpetual inventory method, which uses the Inventory account when the company buys, sells, or adjusts the inventory balance, such as in the following example where they qualified for a discount. In the current transaction, credit terms are 2/10, n/30, the invoice date is August 1, and shipping charges are FOB shipping point (which is included in the purchase cost).

Recall that credit terms of 2/10, n/30 signal the payment terms and discount, and FOB shipping point establishes the point of merchandise ownership, the responsibility during transit, and which entity pays shipping charges. Therefore, 2/10, n/30 means Sierra Sports has ten days to pay its balance due to receive a 2% discount, otherwise Sierra Sports has net thirty days, in this case August 31, to pay in full but not receive a discount. FOB shipping point signals that since Sierra Sports takes ownership of the merchandise when it leaves the manufacturer, it takes responsibility for the merchandise in transit and will pay the shipping charges.

Sierra Sports would make the following journal entry on August 1.

The merchandise is purchased from the supplier on credit. In this case, Accounts Payable would increase (a credit) for the full amount due. Inventory, the asset account, would increase (a debit) for the purchase price of the merchandise.

If Sierra Sports pays the full amount owed on August 10, it qualifies for the discount, and the following entry would occur.

Assume that the payment to the manufacturer occurs within the discount period of ten days (2/10, n/30) and is recognized in the entry. Accounts Payable decreases (debit) for the original amount due, Inventory decreases (credit) for the discount amount of $240 ($12,000 × 2%), and Cash decreases (credit) for the remaining balance due after discount.

Note that Inventory is decreased in this entry because the value of the merchandise (soccer equipment) is reduced. When applying the perpetual inventory method, this reduction is required by generally accepted accounting principles (GAAP) (under the cost principle) to reflect the actual cost of the merchandise.

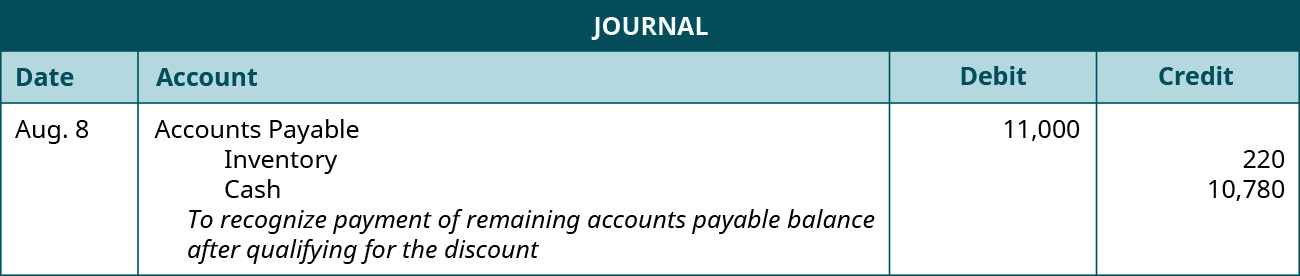

A second possibility is that Sierra will return part of the purchase before the ten-day discount window has expired. Assume in this example that $1,000 of the $12,000 purchase was returned to the seller on August 8 and the remaining account payable due was paid by Sierra to the seller on August 10, which means that Sierra qualified for the remaining eligible discount. The following two journal entries represent the return of inventory and the subsequent payment for the remaining account payable owed. The initial journal entry from August 1 will still apply, because we assume that Sierra intended to keep the full $12,000 of inventory when the purchase was made.

When the $1,000 in inventory was returned on August 8, the accounts payable account and the inventory accounts should be reduced by $1,000 as demonstrated in this journal entry.

After this transaction, Sierra still owed $11,000 and still had $11,000 in inventory from the purchase, assuming that Sierra had not sold any of it yet.

When Sierra paid the remaining balance on August 10, the company qualified for the discount. However, since Sierra only owed a remaining balance of $11,000 and not the original $12,000, the discount received was 2% of $11,000, or $220, as demonstrated in this journal entry. Since Sierra owed $11,000 and received a discount of $220, the supplier was paid $10,780. This second journal entry is the same as the one that would have recognized an original purchase of $11,000 that qualified for a discount.

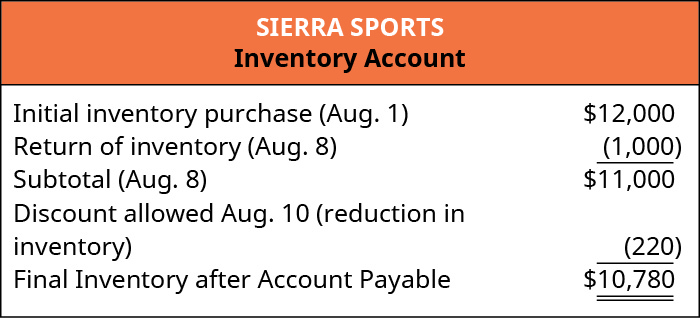

Remember that since we are assuming that Sierra was using the perpetual inventory method, purchases, payments, and adjustments in goods available for sale are reflected in the company’s Inventory account. In our example, one of the potential adjustments is that discounts received are recorded as reductions to the Inventory account.

To demonstrate this concept, after buying $12,000 in inventory, returning $1,000 in inventory, and then paying for the remaining balance and qualifying for the discount, Sierra’s Inventory balance increased by $10,780, as shown.

If Sierra had bought $11,000 of inventory on August 1 and paid cash and taken the discount, after taking the $220 discount, the increase of Inventory on their balance sheet would have been $10,780, as it finally ended up being in our more complicated set of transactions on three different days. The important factor is that the company qualified for a 2% discount on inventory that had a retail price before discounts of $11,000.

In a final possible scenario, assume that Sierra Sports remitted payment outside of the discount window on August 28, but inside of thirty days. In this case, they did not qualify for the discount, and assuming that they made no returns they paid the full, undiscounted balance of $12,000.

If this occurred, both Accounts Payable and Cash decreased by $12,000. Inventory is not affected in this instance because the full cost of the merchandise was paid; so, the increase in value for the inventory was $12,000, and not the $11,760 value determined in our beginning transactions where they qualified for the discount.

Unearned Revenue

Unearned revenue, also known as deferred revenue, is a customer’s advance payment for a product or service that has yet to be provided by the company. Some common unearned revenue situations include subscription services, gift cards, advance ticket sales, lawyer retainer fees, and deposits for services. As you learned when studying the accounting cycle, we are applying the principles of accrual accounting when revenues and expenses are recognized in different months or years. Under accrual accounting, a company does not record revenue as earned until it has provided a product or service, thus adhering to the revenue recognition principle. Until the customer is provided an obligated product or service, a liability exists, and the amount paid in advance is recognized in the Unearned Revenue account. As soon as the company provides all, or a portion, of the product or service, the value is then recognized as earned revenue.

For example, assume that a landscaping company provides services to clients. The company requires advance payment before rendering service. The customer’s advance payment for landscaping is recognized in the Unearned Service Revenue account, which is a liability. Once the company has finished the client’s landscaping, it may recognize all of the advance payment as earned revenue in the Service Revenue account. If the landscaping company provides part of the landscaping services within the operating period, it may recognize the value of the work completed at that time.

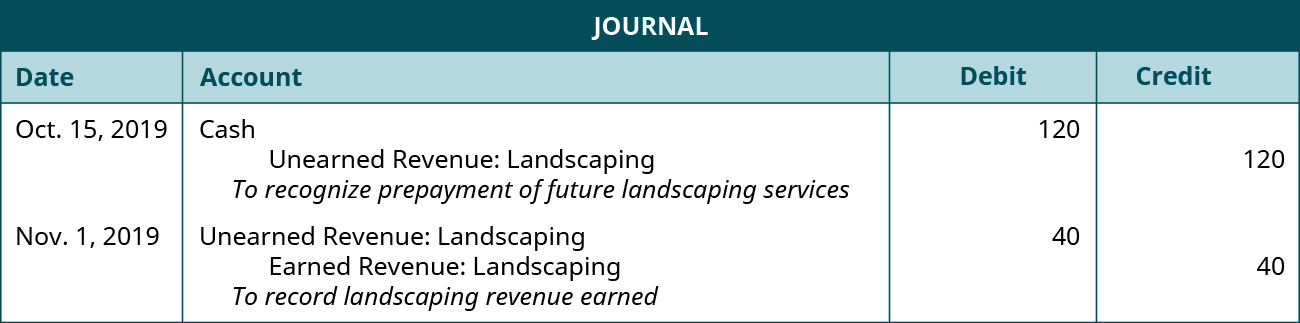

Perhaps at this point a simple example might help clarify the treatment of unearned revenue. Assume that the previous landscaping company has a three-part plan to prepare lawns of new clients for next year. The plan includes a treatment in November 2019, February 2020, and April 2020. The company has a special rate of $120 if the client prepays the entire $120 before the November treatment. In real life, the company would hope to have dozens or more customers. However, to simplify this example, we analyze the journal entries from one customer. Assume that the customer prepaid the service on October 15, 2019, and all three treatments occur on the first day of the month of service. We also assume that $40 in revenue is allocated to each of the three treatments.

Before examining the journal entries, we need some key information. Because part of the service will be provided in 2019 and the rest in 2020, we need to be careful to keep the recognition of revenue in its proper period. If all of the treatments occur, $40 in revenue will be recognized in 2019, with the remaining $80 recognized in 2020. Also, since the customer could request a refund before any of the services have been provided, we need to ensure that we do not recognize revenue until it has been earned. While it is nice to receive funding before you have performed the services, in essence, all you have received when you get the money is a liability (unearned service revenue), with the hope of it eventually becoming revenue. The following journal entries are built upon the client receiving all three treatments. First, for the prepayment of future services and for the revenue earned in 2019, the journal entries are shown.

For the revenue earned in 2020, the journal entries would be.

CONCEPTS IN PRACTICE

Thinking about Unearned Revenue

When thinking about unearned revenue, consider the example of Amazon.com, Inc. Amazon has a large business portfolio that includes a widening presence in the online product and service space. Amazon has two services in particular that contribute to their unearned revenue account: Amazon Web Services and Prime membership.

According to Business Insider, Amazon had $4.8 billion in unearned revenue recognized in their fourth quarter report (December 2016), with most of that contribution coming from Amazon Web Services.1 This is an increase from prior quarters. The growth is due to larger and longer contracts for web services. The advance payment for web services is transferred to revenue over the term of the contract. The same is true for Prime membership. Amazon receives $99 in advance pay from customers, which is amortized over the twelve-month period of the service agreement. This means that each month, Amazon only recognizes $8.25 per Prime membership payment as earned revenue.

Sierra Sports has contracted with a local youth football league to provide all uniforms for participating teams. The league pays for the uniforms in advance, and Sierra Sports provides the customized uniforms shortly after purchase. The following situation shows the journal entry for the initial purchase with cash. Assume the league pays Sierra Sports for twenty uniforms (cost per uniform is $30, for a total of $600) on April 3.

Sierra Sports would see an increase to Cash (debit) for the payment made from the football league. The revenue from the sale of the uniforms is $600 (20 uniforms × $30 per uniform). Unearned Uniform Revenue accounts reflect the prepayment from the league, which cannot be recognized as earned revenue until the uniforms are provided. Unearned Uniform Revenue is a current liability account that increases (credit) with the increase in outstanding product debt.

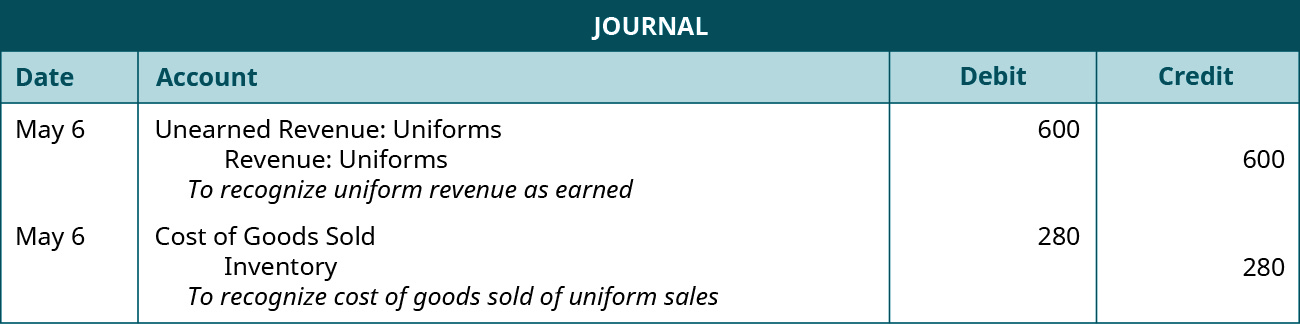

Sierra provides the uniforms on May 6 and records the following entry.

Now that Sierra has provided all of the uniforms, the unearned revenue can be recognized as earned. This satisfies the revenue recognition principle. Therefore, Unearned Uniform Revenue would decrease (debit), and Uniform Revenue would increase (credit) for the total amount.

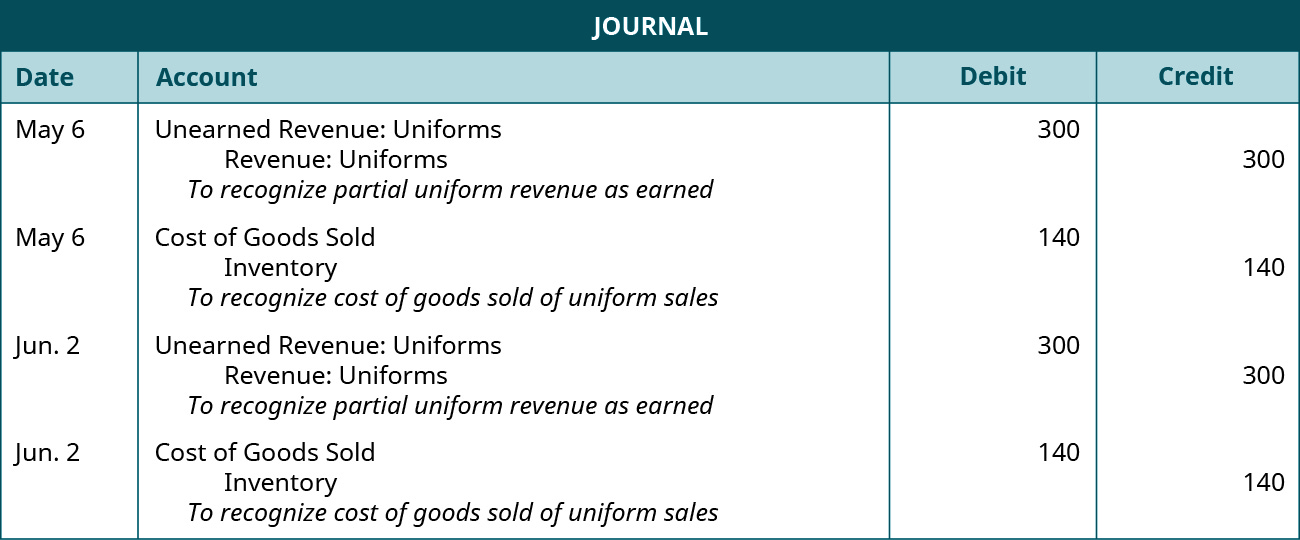

Let’s say that Sierra only provides half the uniforms on May 6 and supplies the rest of the order on June 2. The company may not recognize revenue until a product (or a portion of a product) has been provided. This means only half the revenue can be recognized on May 6 ($300) because only half of the uniforms were provided. The rest of the revenue recognition will have to wait until June 2. Since only half of the uniforms were delivered on May 6, only half of the costs of goods sold would be recognized on May 6. The other half of the costs of goods sold would be recognized on June 2 when the other half of the uniforms were delivered. The following entries show the separate entries for partial revenue recognition.

In another scenario using the same cost information, assume that on April 3, the league contracted for the production of the uniforms on credit with terms 5/10, n/30. They signed a contract for the production of the uniforms, so an account receivable was created for Sierra, as shown.

Sierra and the league have worked out credit terms and a discount agreement. As such, the league can delay cash payment for ten days and receive a discount, or for thirty days with no discount assessed. Instead of cash increasing for Sierra, Accounts Receivable increases (debit) for the amount the football league owes.

The league pays for the uniforms on April 15, and Sierra provides all uniforms on May 6. The following entry shows the payment on credit.

The football league made payment outside of the discount period, since April 15 is more than ten days from the invoice date. Thus, they do not receive the 5% discount. Cash increases (debit) for the $600 paid by the football league, and Accounts Receivable decreases (credit).

In the next example, let’s assume that the league made payment within the discount window, on April 13. The following entry occurs.

In this case, Accounts Receivable decreases (credit) for the original amount owed, Sales Discount increases (debit) for the discount amount of $30 ($600 × 5%), and Cash increases (debit) for the $570 paid by the football league less discount.

When the company provides the uniforms on May 6, Unearned Uniform Revenue decreases (debit) and Uniform Revenue increases (credit) for $600.

Unearned Revenue Interactive Practice

A note payable is a debt to a lender with specific repayment terms, which can include principal and interest. A note payable has written contractual terms that make it available to sell to another party. The principal on a note refers to the initial borrowed amount, not including interest. In addition to repayment of principal, interest may accrue. Interest is a monetary incentive to the lender, which justifies loan risk.

Let’s review the concept of interest. Interest is an expense that you might pay for the use of someone else’s money. For example, if you have a credit card and you owe a balance at the end of the month it will typically charge you a percentage, such as 1.5% a month (which is the same as 18% annually) on the balance that you owe. Assuming that you owe $400, your interest charge for the month would be $400 × 1.5%, or $6.00. To pay your balance due on your monthly statement would require $406 (the $400 balance due plus the $6 interest expense).

We make one more observation about interest: interest rates are typically quoted in annual terms. For example, if you borrowed money to buy a car, your interest expense might be quoted as 9%. Note that this is an annual rate. If you are making monthly payments, the monthly charge for interest would be 9% divided by twelve, or 0.75% a month. For example, if you borrowed $20,000, and made sixty equal monthly payments, your monthly payment would be $415.17, and your interest expense component of the $415.17 payment would be $150.00. The formula to calculate interest on either an annual or partial-year basis is:

In our example this would be

The good news is that for a loan such as our car loan or even a home loan, the loan is typically what is called fully amortizing. At this point, you just need to know that in our case the amount that you owe would go from a balance due of $20,000 down to $0 after the twentieth payment and the part of your $415.17 monthly payment allocated to interest would be less each month. For example, your last (sixtieth) payment would only incur $3.09 in interest, with the remaining payment covering the last of the principle owed. See Figure 5.18 for an exhibit that demonstrates this concept.

A note payable is usually classified as a long-term (noncurrent) liability if the note period is longer than one year or the standard operating period of the company. However, during the company’s current operating period, any portion of the long-term note due that will be paid in the current period is considered a current portion of a note payable. The outstanding balance note payable during the current period remains a noncurrent note payable. Note that this does not include the interest portion of the payments. On the balance sheet, the current portion of the noncurrent liability is separated from the remaining noncurrent liability. No journal entry is required for this distinction, but some companies choose to show the transfer from a noncurrent liability to a current liability.

For example, a bakery company may need to take out a $100,000 loan to continue business operations. The bakery’s outstanding note principal is $100,000. Terms of the loan require equal annual principal repayments of $10,000 for the next ten years. Payments will be made on July 1 of each of the ten years. Even though the overall $100,000 note payable is considered long term, the $10,000 required repayment during the company’s operating cycle is considered current (short term). This means $10,000 would be classified as the current portion of a noncurrent note payable, and the remaining $90,000 would remain a noncurrent note payable.

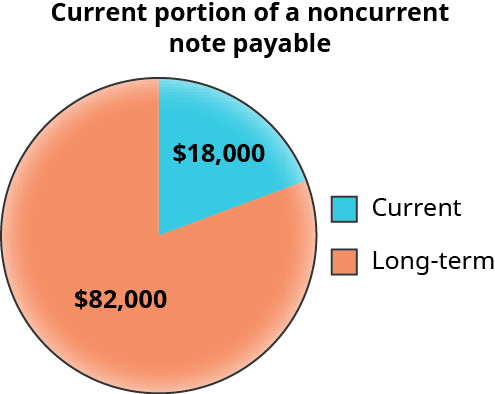

The portion of a note payable due in the current period is recognized as current, while the remaining outstanding balance is a noncurrent note payable. For example, Figure 5.19 shows that $18,000 of a $100,000 note payable is scheduled to be paid within the current period (typically within one year). The remaining $82,000 is considered a long-term liability and will be paid over its remaining life.

In addition to the $18,000 portion of the note payable that will be paid in the current year, any accrued interest on both the current portion and the long-term portion of the note payable that is due will also be paid. Assume, for example, that for the current year $7,000 of interest will be accrued. In the current year the debtor will pay a total of $25,000—that is, $7,000 in interest and $18,000 for the current portion of the note payable. A similar type of payment will be paid each year for as long as any of the note payable remains; however, the annual interest expense would be reduced since the remaining note payable owed will be reduced by the previous payments.

Interest payable can also be a current liability if accrual of interest occurs during the operating period but has yet to be paid. An annual interest rate is established as part of the loan terms. Interest accrued is recorded in Interest Payable (a credit) and Interest Expense (a debit). To calculate interest, the company can use the following equations. This method assumes a twelve-month denominator in the calculation, which means that we are using the calculation method based on a 360-day year. This method was more commonly used prior to the ability to do the calculations using calculators or computers, because the calculation was easier to perform. However, with today’s technology, it is more common to see the interest calculation performed using a 365-day year. We will demonstrate both methods.

For example, we assume the bakery has an annual interest rate on its loan of 7%. The loan interest began accruing on July 1 and it is now December 31. The bakery has accrued six months of interest and would compute the interest liability as

The $3,500 is recognized in Interest Payable (a credit) and Interest Expense (a debit).

Taxes Payable

Taxes payable refers to a liability created when a company collects taxes on behalf of employees and customers or for tax obligations owed by the company, such as sales taxes or income taxes. A future payment to a government agency is required for the amount collected. Some examples of taxes payable include sales tax and income taxes.

Sales taxes result from sales of products or services to customers. A percentage of the sale is charged to the customer to cover the tax obligation (see Figure 5.21). The sales tax rate varies by state and local municipalities but can range anywhere from 1.76% to almost 10% of the gross sales price. Some states do not have sales tax because they want to encourage consumer spending. Those businesses subject to sales taxation hold the sales tax in the Sales Tax Payable account until payment is due to the governing body.

For example, assume that each time a shoe store sells a $50 pair of shoes, it will charge the customer a sales tax of 8% of the sales price. The shoe store collects a total of $54 from the customer. The $4 sales tax is a current liability until distributed within the company’s operating period to the government authority collecting sales tax.

Income taxes are required to be withheld from an employee’s salary for payment to a federal, state, or local authority (hence they are known as withholding taxes). This withholding is a percentage of the employee’s gross pay.

Let’s consider our previous example where Sierra Sports purchased $12,000 of soccer equipment in August. Sierra now sells the soccer equipment to a local soccer league for $18,000 cash on August 20. The sales tax rate is 6%. The following revenue entry would occur.

Cash increases (debit) for the sales amount plus sales tax. Sales Tax Payable increases (credit) for the 6% tax rate ($18,000 × 6%). Sierra’s tax liability is owed to the State Tax Board. Sales increases (credit) for the original amount of the sale, not including sales tax. If Sierra’s customer pays on credit, Accounts Receivable would increase (debit) for $19,080 rather than Cash.

When Sierra remits payment to the State Tax Board on October 1, the following entry occurs.

Sales Tax Payable and Cash decrease for the payment amount of $1,080. Sales tax is not an expense to the business because the company is holding it on account for another entity.

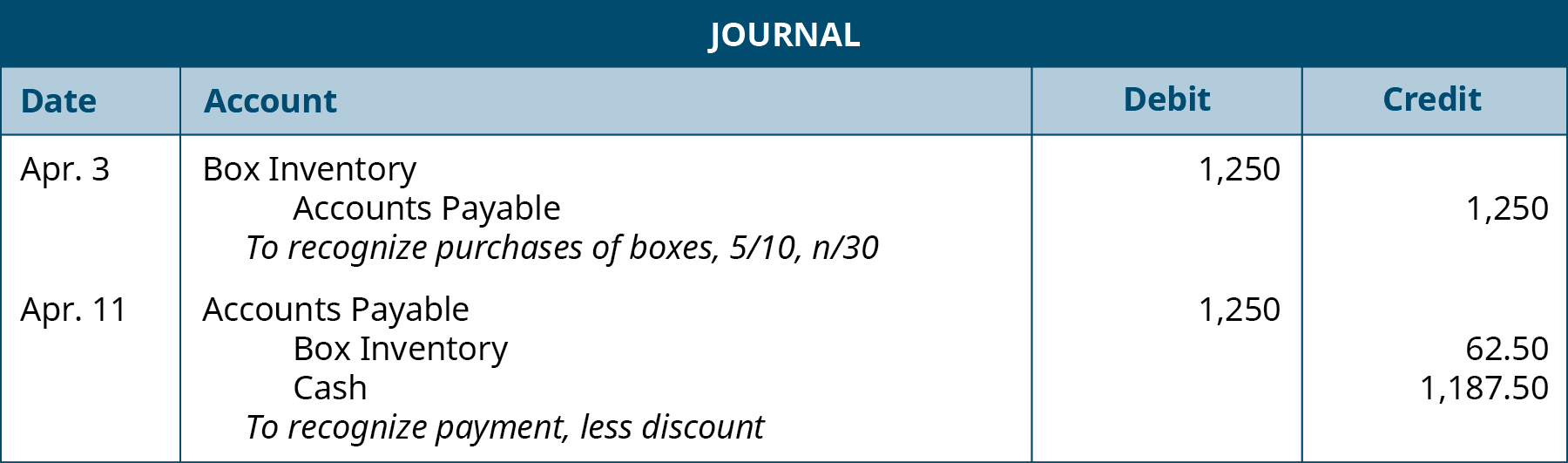

YOUR TURN

Accounting for Purchase Discounts

You own a shipping and packaging facility and provide shipping services to customers. You have worked out a contract with a local supplier to provide your business with packing materials on an ongoing basis. Terms of your agreement allow for delayed payment of up to thirty days from the invoice date, with an incentive to pay within ten days to receive a 5% discount on the packing materials. On April 3, you purchase 1,000 boxes (Box Inventory) from this supplier at a cost per box of $1.25. You pay the amount due to the supplier on April 11. Record the journal entries to recognize the initial purchase on April 3, and payment of the amount due on April 11.

Solution

Long Descriptions

Invoice document from the company Sierra Sports, located on 246 Sierra Road, Anywhere, USA 01234. Invoice no. is 00257; invoice date is August 12, 2016. Joe Johnson is the customer that is billed. SI NO 1; Description of item is Youth Snowboard, Quantity of 10, Unit Price of $45.99, and the Amount is $459.90. Shipping charges are $56. Total is $515.90. Credit term: Net 30.

Return

The first journal entry is made on October 15 in 2019 and shows a Debit to Cash for $120, and a credit to unearned landscape revenue for $120, with the note “to recognize prepayment of future landscaping services.” The second journal entry is made on November 1 in 2019 and shows a debit to unearned landscape revenue for $40, and a credit to Landscaping revenue earned for $40, with the note “to record landscaping revenue earned. Return

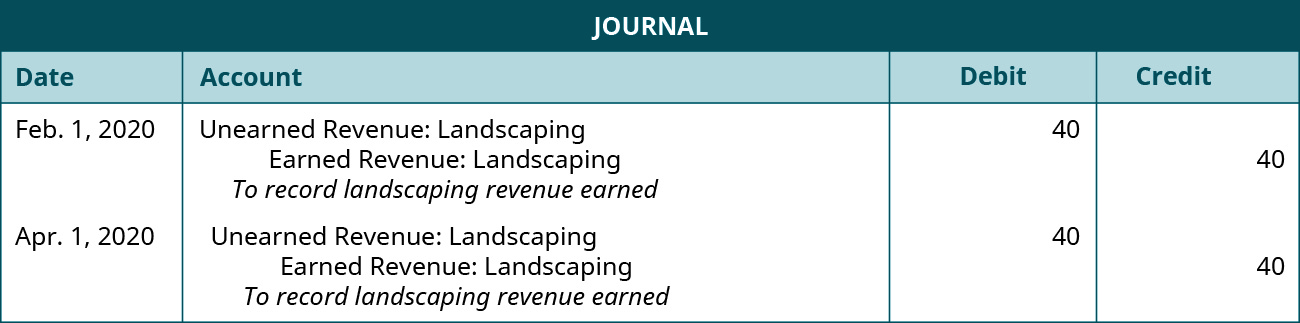

The first journal entry is made on February 1 in 2020 and shows a Debit to Unearned landscape revenue for $40, and a credit to Landscaping revenue earned for $40, with the note “To record landscaping revenue earned.” The second journal entry is made on April 1 in 2020 and shows a debit to unearned landscape revenue for $40, and a credit to Landscaping revenue earned for $40, with the note “To record landscaping revenue earned. Return

A journal entry is made on May 6 and shows a Debit to Unearned uniform revenue for $300, and a credit to Uniform revenue for $300, with the note “To recognize partial uniform revenue as earned.” A second journal entry on May 6 shows a Debit to Cost of goods sold for $140, and a credit to Inventory for $140, with the note “To recognize cost of goods sold of uniform sales.” A second journal entry is made on June 2 and shows a Debit to Unearned uniform revenue for $300, and a credit to Uniform revenue for $300, with the note “To recognize partial uniform revenue as earned.” A second journal entry on May 6 shows a Debit to Cost of goods sold for $140, and a credit to Inventory for $140, with the note “To recognize cost of goods sold of uniform sales.” Return

Footnotes

- 1 Eugene Kim. “An Overlooked Part of Amazon Will Be in the Spotlight When the Company Reports Earnings.” Business Insider. April 28, 2016. https://www.businessinsider.com/amazon-unearned-revenue-growth-shows-why-it-spent-more-on-shipping-last-quarter-2016-4

.jpg){kind=link}